House Prices – Sale Soon

The residential property market is one of the key drivers of the US and UK economies, although not so much in many parts of Europe where they still have a large proportion of renters. Our affair with property in this country started in the ’70s. Rampant inflation caused people to want a store of wealth accessible to the growing middle class, and property was the obvious choice.

I was thinking for a long time about how to create an index of the middle class. The stability of any society, and its general prosperity, is a function of the size of the middle class and whether it’s growing or contracting. Actually, property ownership is a good proxy for that. Not prices per se, as there are all sorts of other factors at play there – foreign investment, buy-to-let etc. – but the actual proportion of owner occupiers.

Official statistics from various sources are painting the same picture. In spite of low interest rates, and the government’s attempts to encourage first-time buyers and council tenants onto the housing ladder, the high rates of stamp duty, high prices, and general economic and demographic problems are taking their toll. By 2013 home ownership in England had fallen to the lowest level since 1987. Lack of new builds, and lack of wage inflation to keep pace with house prices, have kept would-be owner occupiers out. And the age of first time buyers is much higher than it was 10 or 20 years ago.

We can see that a stable society is being undermined by high property prices and low interest rates. I’m always looking for a signal. I sold out of the last property boom in 2005 myself, and went to live in Brazil for a while, which I can highly recommend! I was ahead of the curve, and if I’d held on another year or so I’d have made more money. But in 2005 there was a flattening out of prices and given you can’t put a stop loss on a house, I have no regrets.

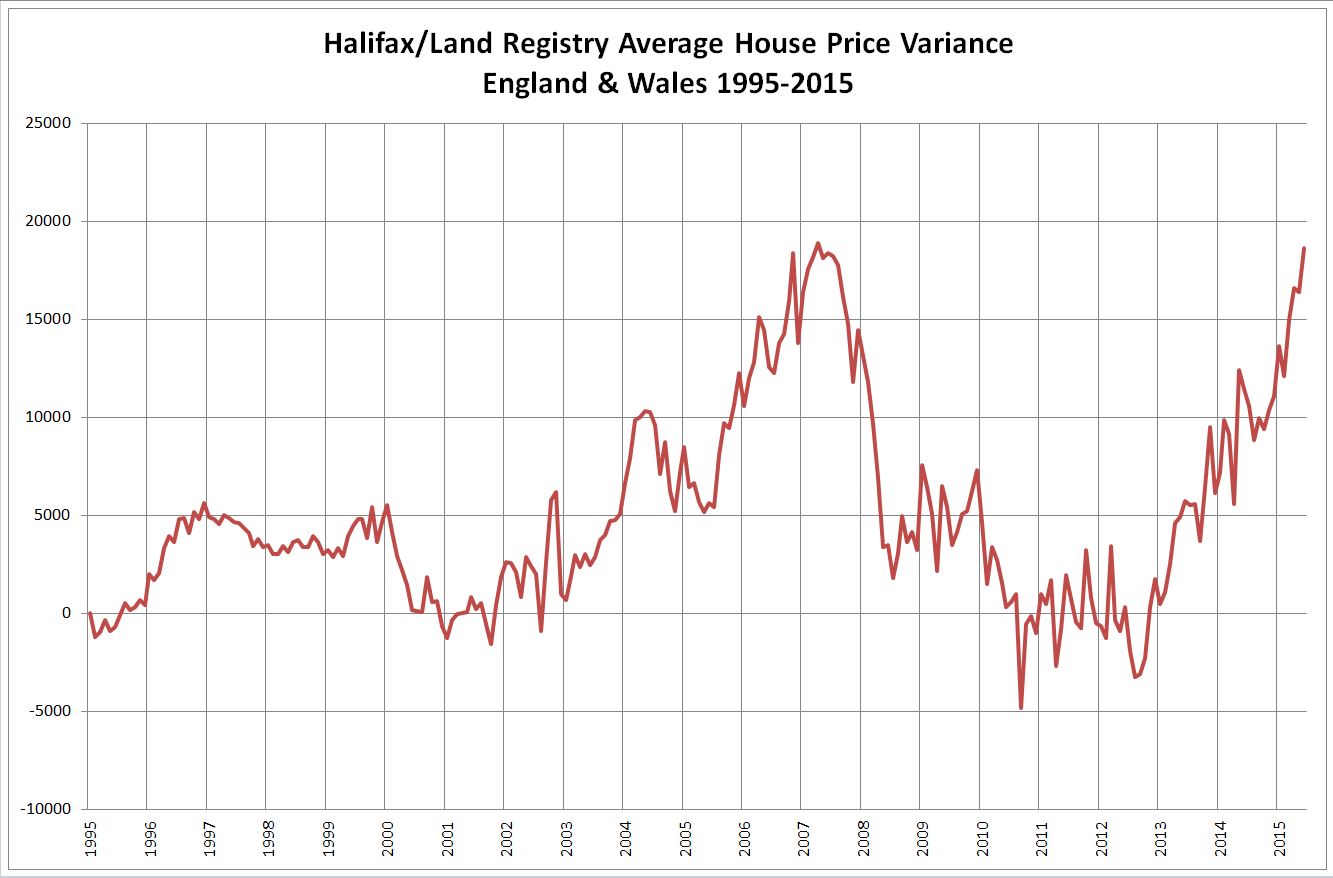

I’ve tended to use Land Registry figures when analysing the property market because it includes all property transactions – i.e. cash purchases, auctions, etc. The Halifax and Nationwide figures are just those requiring mortgages, albeit using large data samples, and just as valid statistically. So I thought I’d compare the average house prices that Halifax calculates with those the Land Registry publishes. This is the closest we can get to the difference between the cash and, to some extent, a de facto futures market in house prices, subsidised by mortgages based on risk assessments by lenders.

The chart I’ve created shows that the only time since 1995 we’ve seen such a disparity between the Halifax and the Land Registry figures was in 2007. This is just the sort of variance we’re looking for to signal a housing correction, if not a crash. With interest rate rises seeming inevitable, it’s hard to see how we won’t see a correction at least, as repossessions kick in and housing stock comes on the market at a discount. Of course house builders could step in before then and take the heat off a bit, but that won’t happen overnight. In any case they want to maximise profits – they’re not a public service industry, so they won’t be keen to bring house prices any lower than they have to.

Alongside the mounting evidence of a failing FTSE, the house price data supports the view that serious economic problems lie ahead. Of course it is possible to short the housing market using spread bets. But that is using a mechanism best suited for short term positions trading a longer term trend, so timing will be critical if the destructive costs of being in a trade for months on end are to be avoided. On the bright side, if you’ve been really hacked off that your savings are being eroded and had almost given up hope of getting on the property ladder, some of the lower rungs might be back in place for a while in the near future. For those who own property, a hedge might be a good idea – and not in your garden! For those with a cheap mortgage, another hedge for the interest payments! A significant fall could also seriously damage the buy-to-let market. When I say significant fall, I mean circa 20%.

Comments (0)