Extend the Duration of Your Bond Portfolio

Over the last one year and a half, the best fixed income play has been to invest in short-term and ultra short-term bonds. With the Federal Reserve hiking its rate target from 0.25% – 0.50% to 5.25% – 5.50% since March 2022, any longer-term play in the bond market has delivered negative returns. This is because bond prices and yields are inversely related and the longer the maturity, the larger the negative price impact. However, with the latest move, the Federal Reserve pushed its rates to a 22-year-high, which increases the odds for it being near the end of the cycle and closer to reversion than to further hikes. If this is right, then this is the best time to increase the duration of a bond portfolio. Longer maturities currently provide great yields by historical means and are those better placed to benefit from monetary policy reversion.

Those who foresee the future based on the present scenario are wrong most of the time. Things change, particularly regarding the economy. I remember that back in 2017, Austria was issuing 70-year bonds yielding 1.65%. By then there was a huge demand for longer term bonds for the wrong reasons. Many institutional investors had to seek for alternative ways of getting higher yields as they couldn’t dare to embark in the risk-on boat sponsored by central banks. By then, a not-so-fool investor had a good reason to invest in a low-to-negative-yielding bond. There were always other fools willing to invest at even lower interest rates. As for institutional investors like pension funds, they hadn’t much of a choice but to extend the duration of their portfolios. Extending duration occurred for the wrong reasons by then.

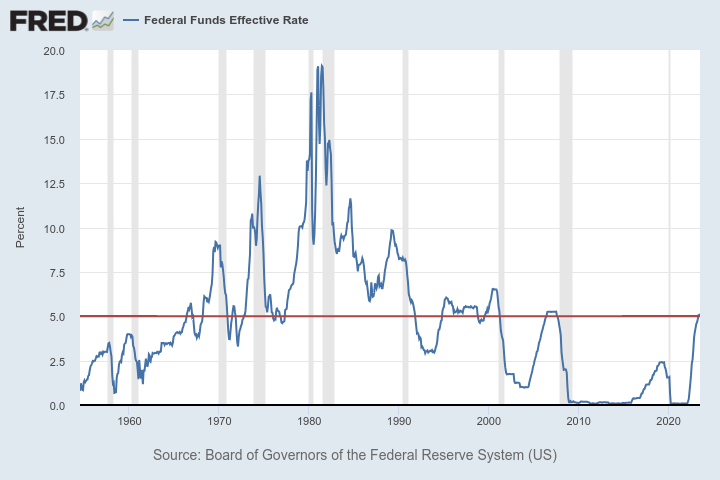

Rate Cycle Is Nearing an End

Today the scenario is much different. The Federal Funds rate is now above 5%, a level last seen in 2007, preceding the Great Financial Crisis (GFC) and in 2000, preceding the tech bubble burst. During most of the 2000s, the Fed Funds rate remained low, particularly between 2008 and 2016, when it was close to zero. However, inflation also remained subdued during most of that period, a scenario that changed significantly over the last two years, forcing central banks to hike their rates.

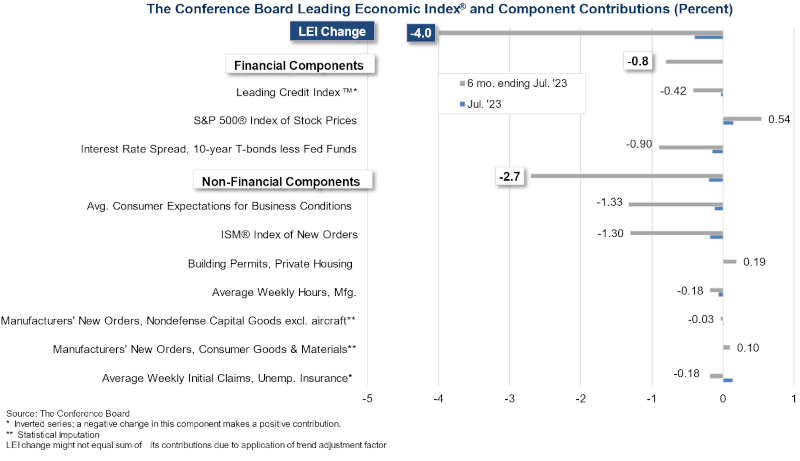

The latest inflation numbers show inflation rising at declining rates, which may prevent the Federal Reserve to keep the pace of rate increases, if not put an end to it. Another point weighting on the current monetary policy stance is the increasing odds of recession. The US economy has been skipping a recession since 2020. However, the numbers aren’t favourable. The Conference Board Leading Economic Index (LEI), a composite indicator aimed at predicting the economy’s trajectory, is predicting a recession. Last month’s reading marked the 16th consecutive decline for the indicator, dropping to a reading of 105.8, it’s lowest since 2020. Such a path of declines was last observed during the period preceding the GFC. The Conference Board is now projecting a recession for the US economy for the end of this year.

The most concerning part comes from the decomposition of the overall reading into its 10 components. It shows that only two of the 10 components rose last month, with those being the S&P 500 index and the average weekly initial claims for unemployment insurance. The job market has been lagging other indicators since the start of the pandemic. As for the stock market, it appears completely out of sync with reality. Investors appear too optimistic about the economy’s trajectory, which increases the odds for a free-fall.

With the points taken above, I believe the Federal Reserve is mostly done with rate hikes and that a recession will occur soon. No matter how mild it could be, I believe this is a good opportunity to increase the duration of a bond portfolio. While shorter maturities offer higher yields, from the perspective of the medium to longer term, I believe this point is great to invest in maturities greater than 10 years. Unlike what happened a few years ago, now we may extend duration for the best reasons.

Extend the Duration

One excellent option to play this trend is to invest in the Vanguard Long-Term Treasury Index Fund ETF (NASDAQ:VGLT). From the perspective of its current performance, investors are certainly not tempted by it, as its year-to-date performance is negative. However, the reasons are the fast interest rate rises occurring since last year. If those are near an end, VGLT’s performance will revert.

VGLT’s bond portfolio duration target is 10 to 25 years. Currently, it sits at 15.8 years. While its average maturity is 22.9 years, the interim coupon payments associated with most bonds shorten duration. VGLT invests only in US Treasuries, providing the best safety. The cost of this ETF is just 0.04%.

Many investors may be thinking about an alternative investment in corporate bonds, as those bonds offer higher returns. Vanguard offers the Long-Term Corporate Bond ETF (NADAQ:VCLT), which invests in investment grade corporate bonds. Unlike VGLT, VCLT is delivering a positive performance this year. Even though this fund seems as a good alternative, its riskier component creates an opposing layer to the play I want to set in. In case of recession, the Federal Reserve may cut rates, which plays favourably to longer-termed bonds. However, a recession is associated with increasing credit risk, which has a negative impact on corporate bond prices (and can have a positive impact on Treasuries due to its perceived safety).

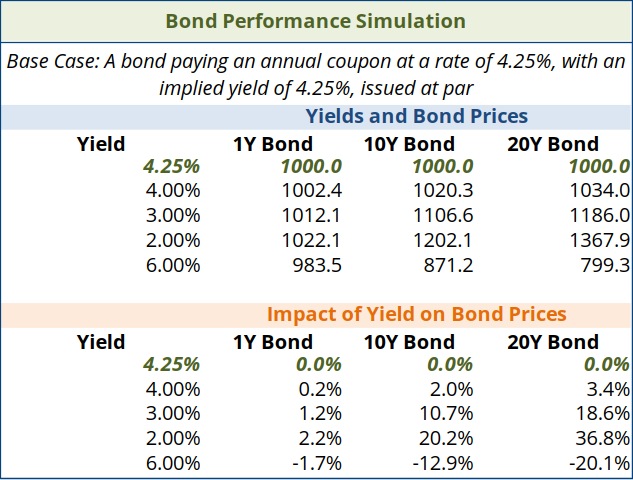

I include below a very simple simulation for the impact of interest rates on bond prices. The base case scenario starts with a bond trading at par value, with a yield of 4.25%. As can be easily spotted, when yields decline, bond prices increase, with the increase being substantially higher on longer maturity bonds. The reverse is also true. But, at this point, I believe the odds for a yield decline are much higher than for the reverse.

Comments (0)