Fund Manager in Focus – Leon Cooperman

“The way to be successful is do what you love and love what you do…I get paid normally a lot of money for basically doing something I enjoy doing. And what I enjoy is to hunt—finding something somebody else doesn’t see, making a bet and having Mr. Market prove me right.”

― Leon Cooperman

Living the American Dream

Leon G. “Lee” Cooperman is a hard-worker who wakes up before sunrise to spend more than 12 hours of his day analysing investments and seeking out new opportunities. With a strong passion for what he does and a desire to see those who work with him succeed, he wakes up before everybody and knows as much about his investments as the CFOs of the companies he invests in. “I don’t think he puts in long hours, I think he works around the clock. I don’t care whether he’s on a plane or car or in Florida presumably on vacation – he’s working”, explains Robert Salomon Jr., former head of Salomon Brothers Asset Management and friend with Cooperman for more than 50 years.

At 72, Cooperman’s career stretches nearly 50 years and he exhibits the same dedication to his wife, Toby, whom he met while at college. Rather than living on 432 Park Avenue and being chauffeured through the streets of New York City, he is more likely to be found on the ferry commuting from his house in the Short Hills, New Jersey, where he lived for 36 years, to his office in New York. The kid who was born in the South Bronx, son of working-class immigrants from Poland, is a self-made man who actually is living the American Dream. With no money in his pocket, a student loan to repay, a wife and a six-month child to feed, Cooperman started working hard in his early twenties. Fifty years later, he made it to the billions and is now ranked #462 on Forbes’ Billionaires list. He feels lucky and grateful for his life and is giving back millions to society. But he feels disgruntled with the treatment the current administration has been giving to the nation’s wealthiest – indeed, he once wrote an open letter to President Obama expressing his feelings on this matter. Unlike many of the wealthiest 1%, he very well knows how rough life can be at times and how hard it is to start underwater and build a life with one’s bare hands. It’s kind of unfair to be punished for succeeding…

A Dental Mistake

Son of a low-income plumber, living in a one-bedroom apartment in the South Bronx, Cooperman grew up poor. He went to the Hunter College where he graduated in economics and met his wife, being the first in his family to earn a college degree. But, oddly as it may sound, he could now be known for his ability to treat teeth – not investments – as he started out at dental school. Only later did he redirect his studies to economics and business.

After graduating, Cooperman went to work at Xerox as a quality control engineer but soon decided to enrol at the Columbia Business School for an MBA, which he completed in January 1967. Without any money, he got a student loan from the National Defense Education Act that allowed him to apply for the MBA. While at Columbia he learned the rules of value investing that would be always present in is his approach to investment. He learned value investing with Benjamin Graham and David Dodd, both of whom are considered fathers of the art. This explains why Cooperman adopts a bottom-up analysis, based on intense and deep company research, which is aimed at unlocking fundamental value from companies. A notable investor who went through the same Columbia MBA is Warren Buffet. The buy-and-hold strategy, which looks at a market downturn as another opportunity to buy more shares on the cheap, is the old-fashioned way the guys from Columbia make money. Cooperman is no exception, which explains why his Omega Advisors has been able to systematically outpace the S&P 500 with lower volatility.

Life at Goldman Sachs

Cooperman is not the kind of man who is willing to wait for anything. The day after he earned his MBA, he headed to Goldman Sachs to start working, where he spent 25 years of his life doing several tasks involving investment. He quickly rose through the ranks and was made partner in charge of research in 1976. Twenty-two years after being hired by Goldman, he assumed an even more important role that would change the company’s future: he helped set up its investment unit – Goldman Sachs Asset Management – for which he served as chairman and chief executive. But, three years later, when the investment bank didn’t acquiesce to his wish to set up a hedge fund, he decided to leave the company to set up his own shop. Omega Advisors was about to be born in 1991, and of course, that happened the day after Cooperman left Goldman.

Founding Omega Advisors

Having learned the fundamental precepts of value investing from the brilliant minds at Columbia and having accumulated 25 years of invaluable experience from Goldman, Cooperman had everything he needed to set up his own hedge fund business – Omega Advisors. Its approach to investment was simple: deeply research through the depths of financial statements and find valuable businesses that are able to deliver more than the market thinks they are. As Cooperman patiently explains to any potential new investor in the fund, he likes to beat the S&P 500 with less volatility than the index offers while trying to mitigate any downturn suffered by the index. Leverage? Not much, if any at all. Short selling? Eventually some on overvalued shares, but just a fraction of what long/short hedge funds engage in.

Cooperman wakes up at 05:15 every weekday and arrives in the office around 06:30. He has a working lunch at the office and usually dines with a few chief executives and fellow investors at around 18:30. He finally comes home but doesn’t go to bed before taking a final glimpse at a Bloomberg terminal (usually around 23h00). He has a frugal life, guided by ethics and hard work. No matter how much his social condition improves, he always sticks to the same key principles in life.

Omega currently manages $9.5 billion (£6.1 billion) and is one of the most respected hedge funds. Unlike many of its peers, where management keeps tight redemption rules to keep investors gated during difficult times (as in the Lehman collapse, for example), Omega allows investors to convert their investments into cash whenever they want to. Unlike what happens with other hedge funds, Omega’s investors are less nervous about any losses, as they very well know that Cooperman is particularly good at recovering from them. Any down year is usually easily reversed over the next year. Any anxious investor withdrawing money after a down year would certainly curse himself over the next year for having done that.

A Stellar Performance in the Long Run

Value investing is good at unlocking profit potential from financial statements and delivering long-term profits but isn’t a good strategy at protecting against short-term downside risks. During recessions and market crashes, Omega reduces its exposure to the market, in an attempt to mitigate any potential losses. But Omega is not exactly a long/short fund prepared to profit from the downside, so it is exposed to the market cycle. And there are, in fact, down years for Omega.

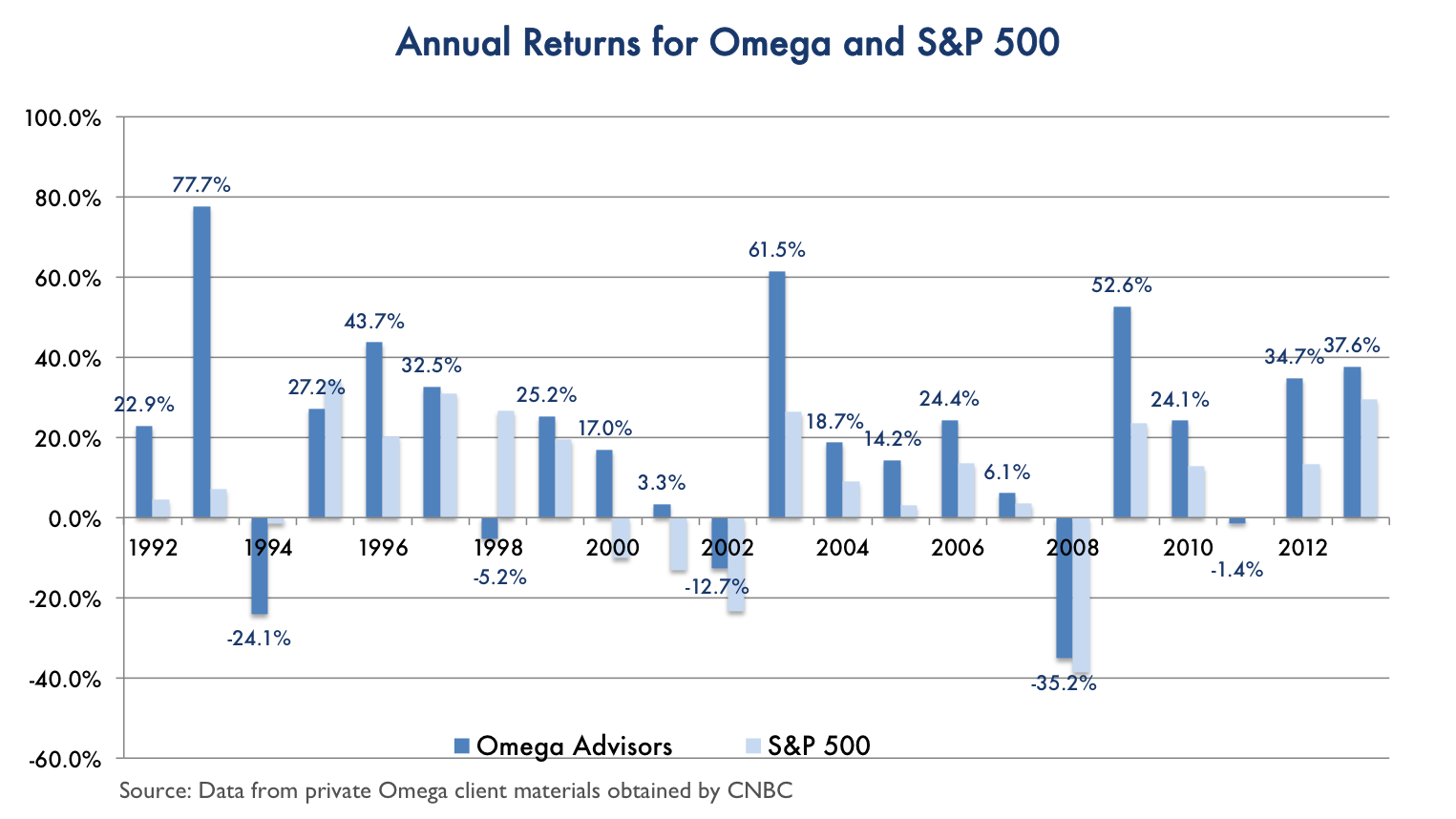

But, what Omega does very well is position itself to profit the most from any recovery. It is common for the fund to more than double the performance recorded by the market during the first years of a recovery. That happened in 1992, 1993, 2003 and 2009.

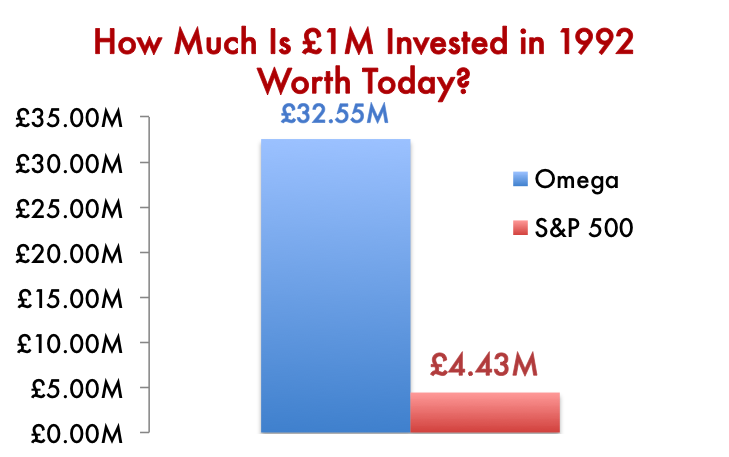

Omega shows just five down years in the period between 1992 and 2013 (22 years) and recorded a CAGR of 17.15%. During the same period, the S&P 500 returned a CAGR of 7.00%. Someone who invested £1 million at inception (at the end of 1991/beginning of 1992) would by now have accumulated £32.55 million, which certainly covers any inflation during the period. The same £1 million invested in the S&P 500 would now be worth £4.43 million.

Nevertheless, Omega has a bullish bias due to the adopted value investing strategy. This makes the fund prone to the downturns observed by the U.S. economy. But Omega has been able to either reduce the loss of the fund relative to the market during such downturns and/or to recover quicker than the market does. That said, Omega wasn’t able to avoid a few bad bets in 1994, the 2002 downturn, the 1998 emerging markets crisis precipitated by the Russia default, and the 2008 financial crisis led by the Lehman collapse. In 2008, the fund lost 35.2% when the market declined 38.5%. But over the next year, in 2009, the fund gained 52.6% when the market rose 23.5% and gained another 24.1% in the following year, when the market recorded a gain of 12.8%. Omega is good at betting big on recoveries, after sell-offs.

Five annual losses in 22 years, with an annual return around 17% is quite an excellent performance, particularly when considering that Omega has achieved this with a low degree of leverage and a high degree of ethics. When asked about his worst moment at Omega, Cooperman doesn’t mention the 2008 loss but rather he seems more perturbed with a fraud episode involving one of Omega’s employees that ended with the company paying a $500,000 fine to the U.S. Justice Department to settle the case. At that time, Omega was in a position to profit from the selling of a state-owned oil company in Azerbaijan, which involved alleged bribery of officials in the country. Clayton Lewis, an Omega executive at that time, was aware of it and hadn’t reported the case. Cooperman was really upset by the episode.

An Example to Follow?

Cooperman always remembers how tough life can be at times and how hard it is for someone coming from a low-income family to set up and make a living. Rather than aligning his habits with the amount of money he earns, he likes to contribute to help improve society. He has created a number of scholarships to help students with financial difficulties; he has donated a few million to Columbia, for the school to expand the campus; and he is involved in several other philanthropic activities. He and his wife Toby, who recently retired from a 25-year career as a teacher for special-needs children, founded the Leon and Toby Foundation, which has been contributing for several causes and currently owns $200 million (£128.6 million) in assets. He also signed the Giving Pledge in 2010 to give a majority of his wealth to charity, “to ensure that [his] money, properly stewarded, continues to do some good after [he’s] gone”.

“I have nothing to apologise for. I’ve made a lot of money. I’m giving it all back to society”, he observes.

Comments (0)