A Generational Opportunity In Bonds?

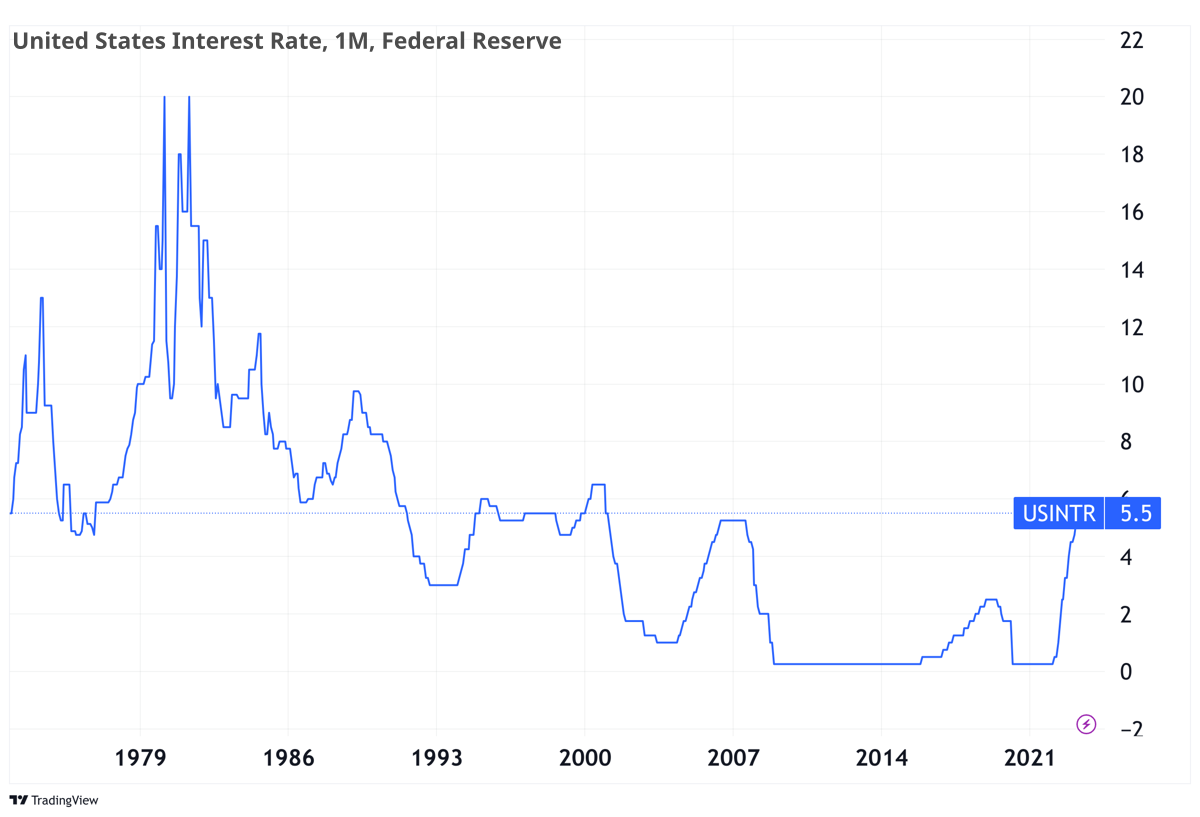

Over the course of the current interest rate cycle, the Federal Reserve has raised its benchmark interest rate 11 times. This has taken it from a target range of 0.00% – 0.25% to 5.25% – 5.50%. These rates have been close to zero for most of the last decade and have been falling since the 1980s. Some institutional investors, such as BlackRock, have seen the current hike as a generational opportunity to buy bonds. The current yield of 4.7% on a 10-year US Treasury is too good to be true. But not all think alike. The rise in yields is evidence that most investors are still on the sidelines. They fear that the Federal Reserve is not finished with interest rates. Whether the interest rate cycle is done or not remains to be seen. But does it matter that much?

BlackRock is forecasting a threefold increase in the value of its bond ETFs by 2030 on the back of a flood of money into fixed income. Its optimism is based on current yields, which are at a two-decade high, and the expected end of the interest rate cycle. However, not all investors agree. Many fear that the central bank is not done raising rates, which could lead to further losses. Many long-term bond ETFs have more than halved in less than two years. This is the result of the Fed’s 525 basis point rate hike. Long-term institutional investors, such as pension funds, have been particularly hard hit. They are reluctant add more money into the long-term bond market. Those in search of fixed income are turning to the money market where interest rate risk is low.

The current situation is a reminder that fixed income is not that safe. David Dreman, the legendary value investor, has mentioned this on a number of occasions, in particular in his books on contrarian investment strategies. Using data from the US stock and bond markets, he shows that bonds are riskier than equities over longer time horizons. Stocks have many ups and downs, but over a decade or more, the market almost always delivers positive inflation-adjusted returns. Bonds don’t. If we look back just a few years, we can see countless examples of long-maturity bonds trading at very low yields that would never cover inflation. This is why I always prefer the stock market.

But this is not about my investment preferences. It is about what to expect from fixed income at this point. If the Fed is done, this will be a golden opportunity to buy long-term bonds and lock in high yields. If inflation stays above 2% for a longer time, the Fed may be tempted to raise rates further and eventually keep them high for longer. This could mean further losses for fixed income.

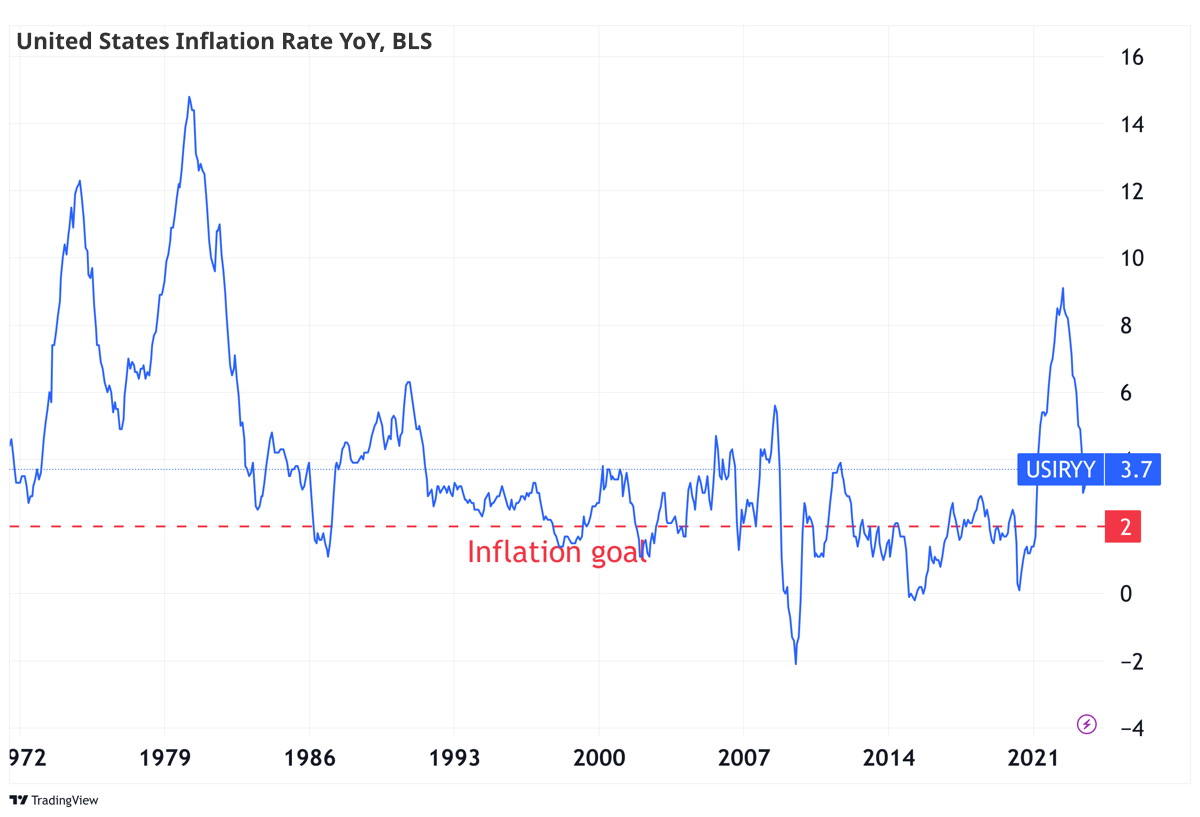

The accumulated losses in the bond market should have been largely expected. We shouldn’t expect interest rates to stay near zero forever. Moreover, at such a level, interest rates are close to their lower bound. The only direction they can go is upwards. Therefore, many years of low interest rates and monetary easing could only end with a bust in fixed income. After all, part of the reason we have inflation at current levels is the zero interest rate environment we have lived in. But both the FED and the ECB are pausing and are unlikely to keep raising rates. Past experience tells us that after such steep rate hikes, we usually enter a recession and a new cycle of rate cuts. This time won’t be any different. The US economy has long been operating close to full capacity, with unemployment rates at four-decade lows. One explanation is that the pandemics are changing inter-temporal choices between present and future consumption, with new generations putting much more emphasis on today rather than tomorrow. The pandemic and global warming, some say, make people lose faith in the future and change their preferences in favour of the present. If that were the case, central banks would have to raise interest rates much more to accommodate the new trend.

In my view, both the loss of time associated with the pandemic and the loss of faith associated with global warming have their own roles to play in explaining consumer resilience, but interest rates will start to bite into consumers’ wallets. Current expectations are relying too much on the recent past and may take time to adjust. But the effects of higher interest rates will be passed on to consumption through the transmission mechanisms of monetary policy, sooner or later. Consumer’s resilience only increases the odds of a hard landing.

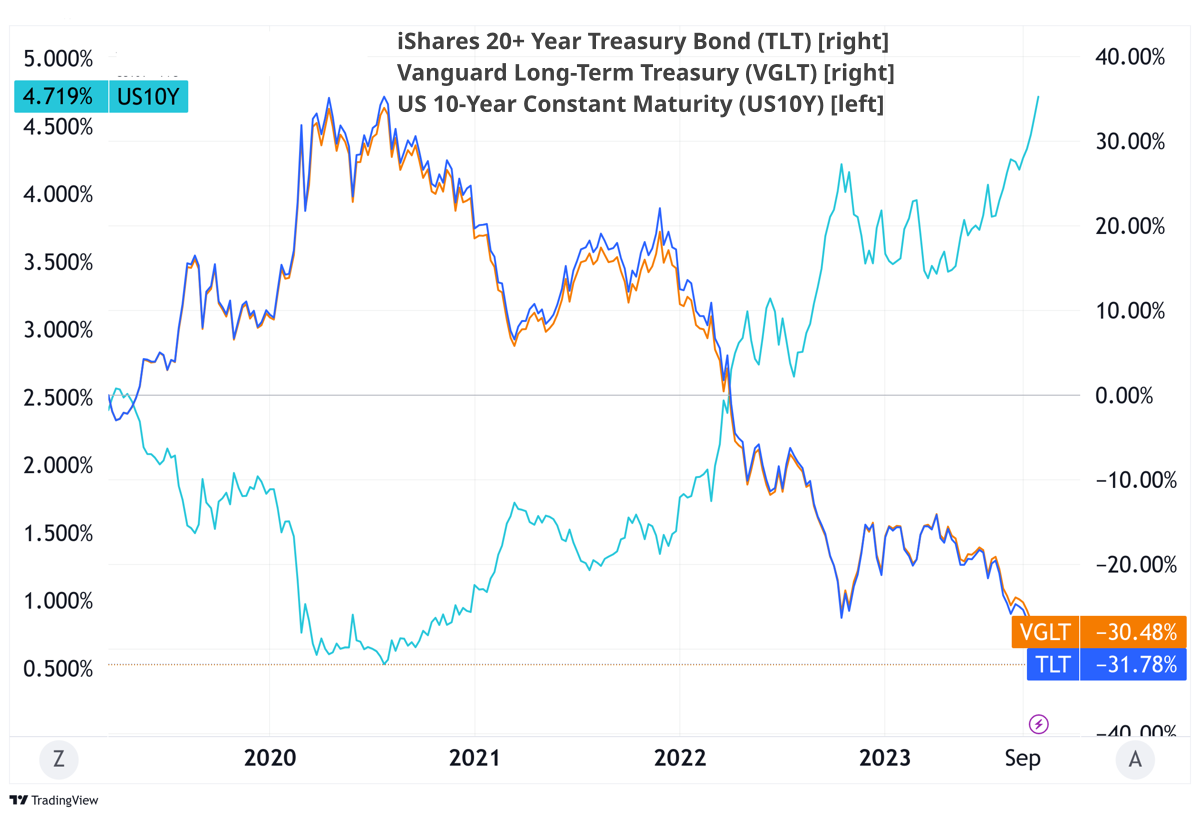

From a long-term bond investor’s perspective, this is ultimately a generational opportunity, as BlackRock sees it. Not only are yields very high, but the risk of recession is also high. Even if yields rise for another year, this is ultimately a loss that a long-term bond investor can bear for the chance of a fat yield thereafter. The wait for the first signs of a recession is too long a wait, and yields would be lower by that time. For these reasons, ETFs like the** iShares 20+ Year Treasury (NASDAQ:TLT)** and the** Vanguard Long-Term Treasury Index (NASDAQ:VGLT)** are, in my view, good options for investors. TLT holds 40 US government securities, trades with an average duration of 16.4 years and charges 0.15%. VGLT holds 78 US government bonds, has an average duration of 15.6 years and charges just 0.04%. In essence, TLT and VGLT are very similar. This is reflected in their performance, which is shown in the chart below. Both are very good options for investors seeking long-term exposure to the US yield curve.

Hi,

And the EM bonds.What do you think you about it?

I’m talking about these 3 tickers VEMT,IS3C and IUS7.

Thanks in advance.

Kind regards,

João Falcão