Zak’s Daily Round-Up

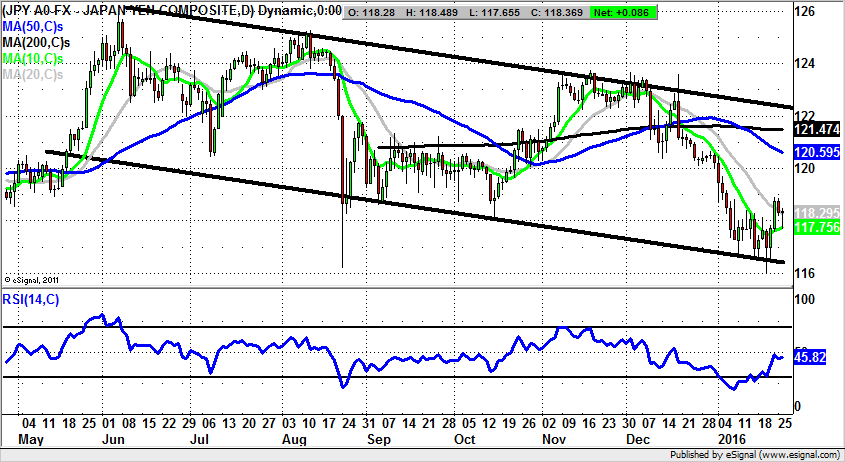

Market Direction: Above 116.50 Targets 122 on Dollar / Yen

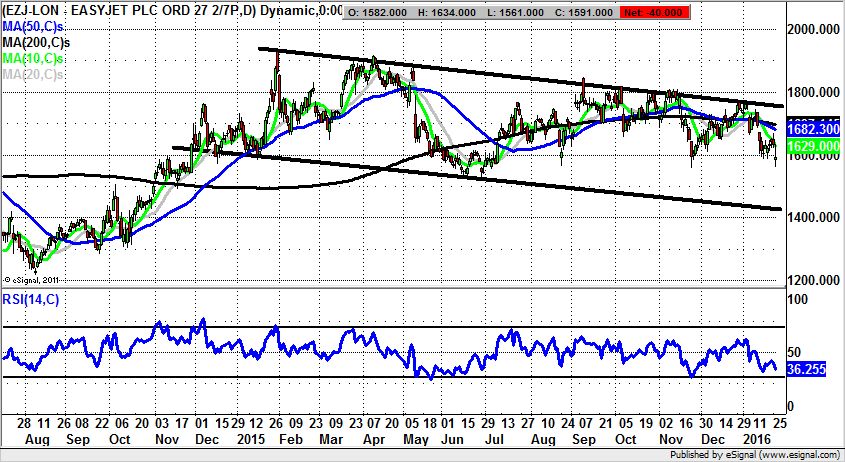

EasyJet (EZJ): Death Cross

It used to be the case in the days of the old flag carriers that the business model was not a good one. However, with the advent of the discount carriers, and their “treat ‘em mean, keep ‘em keen” approach to customer services, the deal for shareholders was very often rather better than for passengers – obsessing over hand baggage weight / size limits. In fact, given that we are in the aftermath of a highly publicised 20th Birthday for EasyJet, and its dreaded orange livery, one might have thought that it is all sweetness and light on the fundamental front. This is particularly the case given the way that the shares are trading in the wake of two gaps to the downside for January to date, the second as yet unfilled. This is not exactly a very healthy state of affairs, especially when combined with the dead cross sell signal for the shares, which came in the form of a negative configuration between the 50 and 200 day moving averages. The position now is that one would expect to see further downside towards the floor of a descending trend channel in place on the daily chart from as long ago as December 2014. All of this goes to suggest that provided there is no end of day close back above the 10 day moving average at 1,626p, the downside here could be towards the 2014 price channel floor at 1,425p over the next 1-2 months.

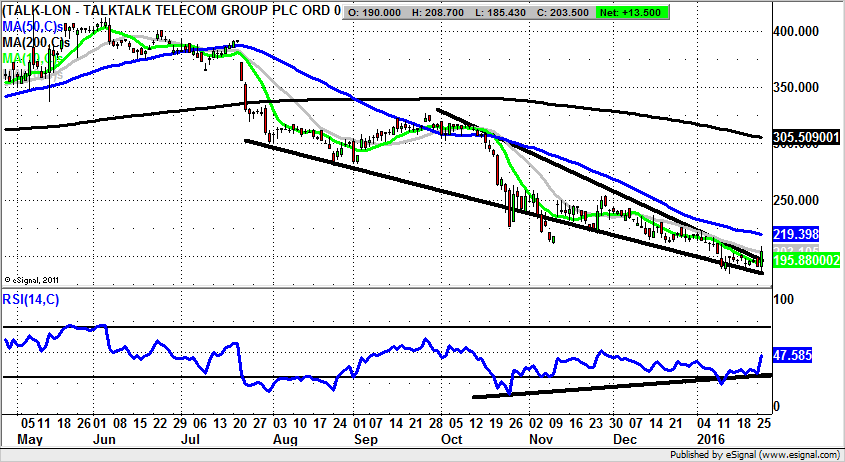

TalkTalk (TALK): Wedge Breakout

It is perhaps an interesting theme to continue for TalkTalk on the “treat ‘em mean, keep ‘em keen” front, with this company arguably being the “no frills” telecoms sector equivalent of EasyJet and Ryanair (RYA). There has been plenty of media anecdotal evidence of the “customer service” this company supplies and the degree of difficulty that some have experienced attempting to escape their contractual obligations to this company. Of even more intrigue was the recent hacking experience the group suffered which lost it 250,000 customers and £35m. Presumably, it will not take too long to make up the ground lost, but as can be seen from the daily chart here, the stock has suffered quite painfully since the summer. Indeed, the halving of the share price over the past six months is all the more surprising given the way that until the middle of 2015 there was apparently a very well entrenched bull run in place. The view now is that for January we have been treated to a double bottom in the 184p zone, with a slightly higher second low within a bullish falling wedge pattern in place on the daily chart since July. All of this goes to suggest that, provided there is no end of day close back below the 184p January support, we should see a “minimum” journey towards the 50 day moving average at 219p over the next 2-3 weeks.

Bull Call:

Patisserie Holdings (CAKE): Above 50 Day Line Targets 500p

Although for many of the Great British public the chance to enjoy themselves at up-market pastry / cakes and the general French sugar produce outlet Patisserie Valerie owner is a joyous experience, for myself the risk of acquiring Type 2 Diabetes is simply way too high for me to join in all the fun. However, putting my fund manager hat on, the opportunity to invest in a high margin, strong brand, High Street chain is a golden opportunity that is simply too good to miss out on. This point is underlined by the trajectory on the daily chart of the shares since they came to market. This has been almost exclusively bullish since the big breakout of November 2014 through the 50 day moving average and the 210p zone. The situation since then has been that we have seen progress within a rising trend channel, one which can be drawn from as long ago as May last year. The main interest in the recent past is the double bounce off the 200 day moving average, now at 327p. The fact that the 200 day line has come in so robustly for the stock, even after the rather sharp decline since the beginning of this month, suggests that we are looking at the opportunity to go long in the midst of a mature bull run, rather than needing to be concerned regarding the end of the line for any rally. The view now is that, provided there is no end of day close back below the 10 day moving average at 360p, the top of last year’s price channel at 500p is possible over the next 1-2 months.

Bear Call:

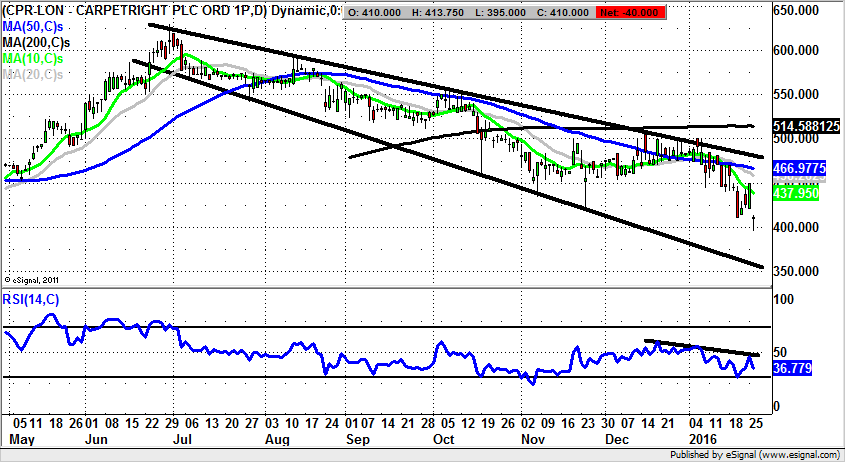

Carpetright (CPR): Risk of 350p

I suppose it is fair to say that Carpetright is one of the many companies on the stock market which is effectively a play on the housing market. The higher the price of real estate goes, the greater the prospects of those who benefit when buyers buy or refurbish their homes. In the case of Carpetright and its daily chart over the post summer period, it can be seen how the climate here has grown rather cooler for the price action. This is said on the basis that there was a brief peak to 629p at the end of June, after which it has been a case of an acceleration to the downside. All of this has occurred within a falling broadening triangle, which has been in place from as long ago as June. The support line formation of the channel currently runs as low as 350p, with this being regarded as the downside for the shares over the next couple of months. The fact that the stock has just delivered a gap to the downside suggests that there is fresh momentum in favour of the bears, and that at least while there is no end of day close back above the 10 day moving average at 436p one should favour further weakness. Indeed, it is probably the case that one should be looking to sell the stock into any strength up to the 10 day line over the next few weeks in order to improve the risk / reward of going short.

Comments (0)