Re-evaluate my Yen bias? Perhaps, but then again…

As seen in this month’s issue of Master Investor Magazine.

Back in June, the USD/JPY reached 125 flat for the first time since December 2002, and posted its highest rate since February of the same year. The systemic weakening of the yen has come about as a result of Japanese efforts to combine monetary and fiscal policy towards a unified target of weakness, with the goal of making Japanese exports cheaper, and in turn boosting international trade. For a couple of years now, we have seen so-called Abenomics dictate the state of the Japanese economy, but based on a number of recent factors, many are arguing that we could see the Japanese government and central bank loosen its grip on the yen, and allow it to – in the near-term at least – regain some strength.

However, these factors aside, there are also a number of macroeconomic fundamental concerns that point towards further yen weakening, going as far as to suggest even, that irrespective of the actions of the Japanese government and the bank of Japan (BoJ), further yen weakness is inevitable. In my own personal trading, I have held a short bias in the yen for a long time, and have published material reinforcing this bias on numerous occasions. However, as we head into the latter half of 2015, the situation is not so clear-cut. So with that said, let’s address both sides of the argument, and try to come down on one side of a definitive bias.

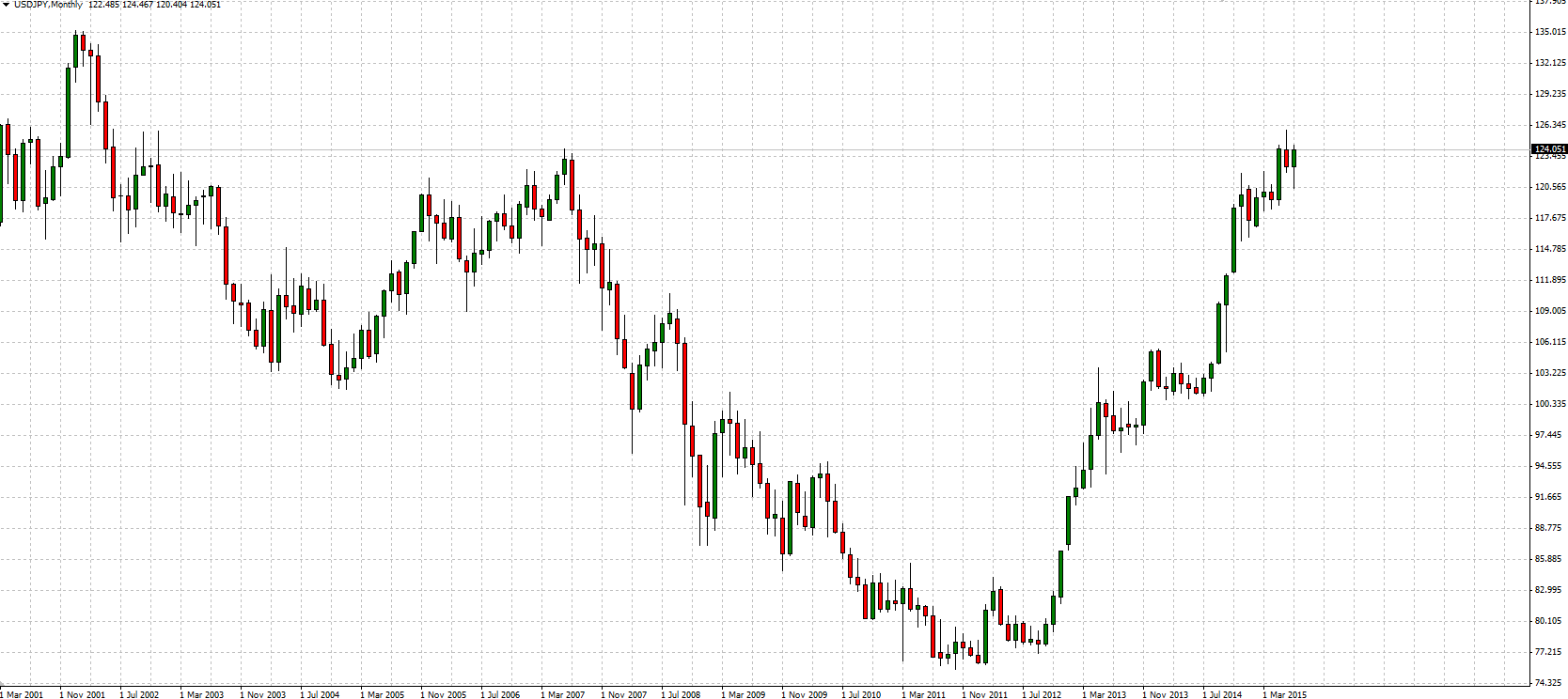

First, let’s look at the argument for near-term yen strength. From a technical perspective, 125 flat presents strong resistance on the higher timeframes (see chart). Having broken this level back in June, the USD/JPY quickly reversed to trade lower and corrected all the way back down to 120 flat before bouncing to current levels of around 123. As we approach 125, we could very easily see medium-term long entry profit taking, to the extent that it initiates another downside correction. Looking at things from a fundamental perspective, Bank of Japan Governor Haruhiko Kuroda said mid-June (around the time of the aforementioned correction, as it happens) that he felt that “it is hard to see the [Yen’s] real effective rate falling further”. In the interest of balance, it is worth noting that he has since commented on this statement as being misinterpreted, but whether there is any validity in this redaction is debatable.

There are also the ongoing Transpacific Partnership (“TPP”) trade talks to take into consideration. For a while now we have heard arguments from a number of the nations involved in these trade talks, which call for provisions against currency market manipulation to be implemented in any potential trade agreements. At close to $125, the current yen valuation puts Japan in a particularly precarious position from a political perspective, especially when we consider that the TPP is very much an integral part of Japanese Prime Minister Shinzo Abe’s three arrows policy. The avoiding of political cross-nation friction within TPP negotiations could viably be enough in itself to make Japanese policymakers think twice about the current yen situation.

However, with all this said, and as we have mentioned, the situation may already be out of Japanese hands. It is now looking increasingly likely that we will get an interest rate hike in the US this September. Fed chair Janet Yellen has hinted at an interest rate rise before the end of the year, and she has two potential dates at which to make good on this intent – September and December. As far as I’m concerned, December is out of the question. An interest rate hike just before New Year would make it very difficult for certain aspects of the US financial framework – and in particular, repo desks – to refinance according to the altered rate. With what has the potential to be a pretty disruptive hike anyway (coming at a time when inflation is zero or negative, as is quarterly GDP in the US), Yellen will want to avoid further complicating the matter. Therefore, this puts September as pretty much a shoo-in for an interest rate hike in the US. In the run-up to this, and post hike, there will inevitably be some dollar strengthening and, in turn, further weakness in the yen. If we break 125, 135 flat (last seen in January, February 2002) will be the level to watch to the upside, and all bets will be off for Abe and Kuroda.

So on which side of this debate does my bias fall? Well, I’d like to think that the yen has weakened about as far as it can, and that the upcoming trade negotiations will spur Japanese policymakers into initiating a reversal. However, with a potential US rate hike looking more and more likely for September, it is very difficult to see how Shinzo Abe can effectively regain control of the Yen – at least in the near to medium term. It is the latter of these two arguments that sways my bias, therefore, so I remain, bearish yen.

Comments (0)