AKC compares the market for insurers

I was at the Royal College of Surgeons last night for the Sir Thomas Gresham Finance Lecture. It was titled ‘Public Interest versus Private Profit – New Models of Risk Sharing’ and was focussed on insurance. Particularly the role government plays in underwriting risk that the public need but which insurers are reticent to provide at an affordable price – notably flood insurance.

It’s not unprecedented for government to be involved in the insurance domain. National Insurance is just such an example, and making third-party car insurance compulsory another. Living near the river myself, it’s good to know that insurance companies who use the government reinsurance organisation, Flood Re, must limit the excess on claims to £250. Apparently the £180m that supports this body (although flood risk is a bit of an open-ended cheque I would have thought) doesn’t come from the public purse, but from a levy on insurers. I can’t really see how that comes from anywhere other than insurance customers then, but it’s forcing insurers to spread risk instead of identify individual risk and set five figure excesses for affected policies.

An interesting concept that came up was the definition of a pension. Bismarck introduced the world’s first state pension in the 1880s, principally to stop people over-providing for it – the idea was to encourage less saving and more spending! The risk here, for what we all know as a pension, is in fact insuring against longevity! That’s the perspective for pension providers, who are of course insurance companies.

Former MP and government minister Mark Hoban is the CEO of Flood Re and he did a little talk followed by an interview with the very erudite Michael Mainelli. Hoban sidestepped some of the hard to answer nuances of Mainelli’s questions (based on questions that attendees had sent in over the preceding weeks). There was a reception after and Hoban still has the gormless smiling face of a politician when engaging with people, like if he stopped trying to look like some sort of Jesus he wouldn’t get elected. Maybe I’m being harsh there, but politicians are professional liars so I find it hard to take them at all seriously. He was also Financial Secretary and oversaw a lot of the new regulation that I’m not that impressed with. My golden rule is: never leave people or pets alone in a room with a politician. He did make a funny quip though about buying motor insurance (as it’s compulsory) really being a poll for your favourite stuffed toy (Meer cat, dog etc). He ruled out a cuddly water vole for Flood Re customers.

I hear that perhaps as many as 10% of drivers out there are uninsured. Perhaps the insurers should stump up a pool of cash to fund police censuses to remedy the problem.

There’s a lot of consolidation going on in the insurance industry. It’s quite annoying really because, cross-border, it means they are less susceptible to local market conditions, and thus harder to predict in terms of share price. TA to the rescue.

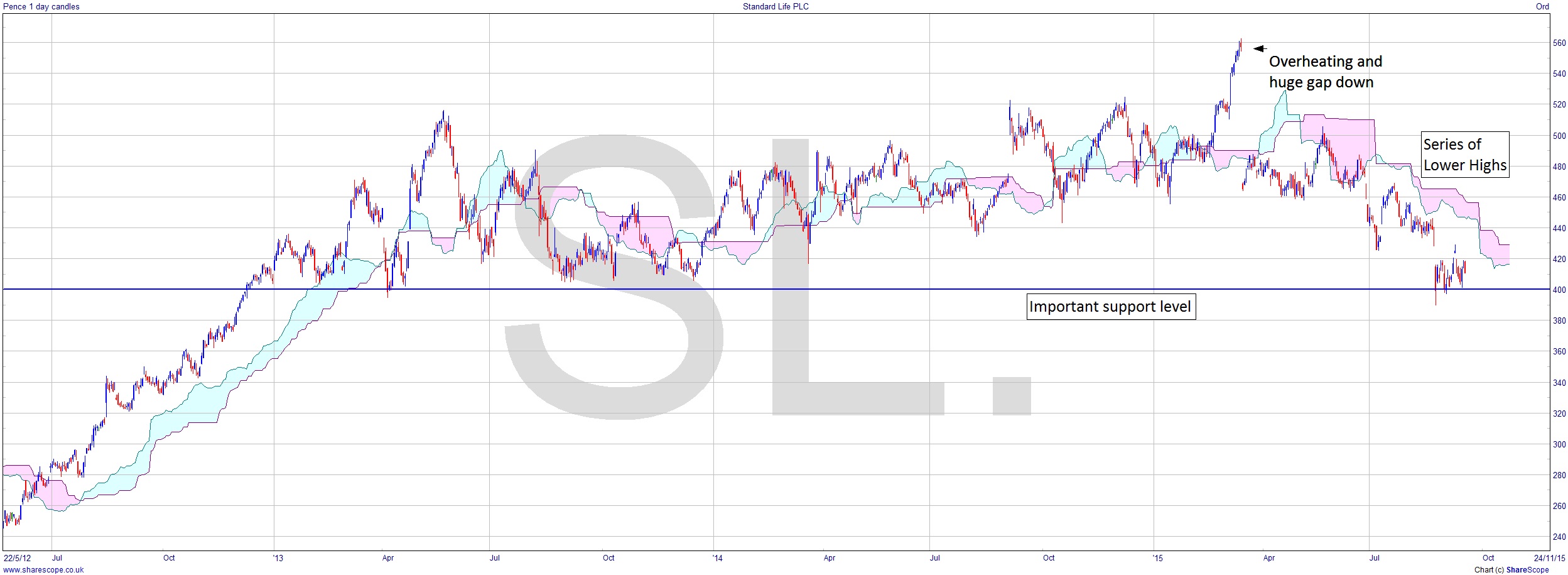

Standard Life (SL.) is looking pretty bad. If it fails at the support level around 400, and especially if that then becomes resistance, it’s in for a rough ride. That massive drop down from the overheated top, staunchly below the Ichimoku cloud, series of LHs, it’s a classic reversal set up over 2+ years.

And also note the fake-out to that overheating from the 520 level. Ok there was a profit there but only if it was taken before the gap. Know anyone who did that?

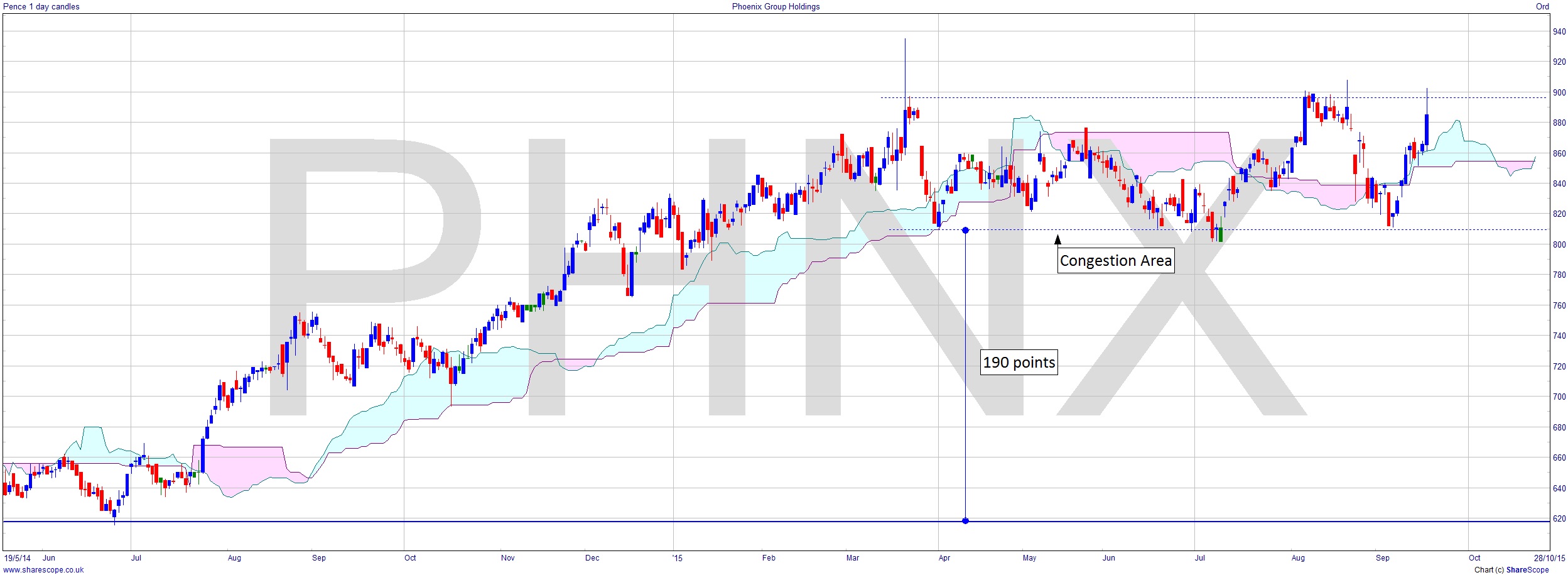

Phoenix (PHNX) looks a bit different and they are very much in M&A mode. I’ve marked the move into the congestion area that it’s been in since the spring. There’s 190 points of measured move upside potential if it does break. And really it’s not a huge percentage.

We still have to be careful of M&A though. It’s a short term trader’s nightmare as it can move a price suddenly and lead to share suspension leaving you holding the baby.

Comments (0)