Don’t Bank on It

As regular readers will know, I’ve been avoiding bank stocks for years now – since April 2007 to be precise. As I predicted in ’08, banks have become a cash cow for government as well as a popular scapegoat. The extra corporation tax on banks that was announced in the budget was just the most recent in a long line of government raids, either directly or by stealth using their not very crack force the FCA (which is, particularly in its previous guise of the FSA, almost entirely responsible for the credit crisis thanks to their laissez-faire “worry about it when it happens” attitude to our financial security).

The role of government has replaced that of monarchs in trying to work out where the money is hidden and regularly raid it, or steal it completely, under the banner of tax revenues or the public good. Oddly, it’s taken them a really long time to work out the places it flows through might just be places to go panning for gold.

The FCA has put measures in place which are populist but don’t serve the purpose of making lending any easier, whilst blaming banks for not lending enough, and effectively banning many of the low risk elements of the banks’ lending portfolios. “That sounds a bit far-fetched Adrian!” I hear you say. Let me explain.

The sub-prime crisis was undoubtedly fuelled by the reluctance of regulators to act – no doubt because governments encouraged them not to. A fundamental lack of understanding of basic economics by the financial regulator should ring enough alarm bells to know why you have to take care of your own finances. What they have done since the crisis is to put in place rules that demand that banks have sufficient evidence of income that a loan can be serviced by the borrower. Seems fair enough?

Let’s take the case of a residential mortgage. Imagine you have received a large sum of money quite legitimately, like a golden handshake. Now let’s say you’re retired early but have easily saleable skills which you’ll use to earn when it suits you. Using your windfall to pay for the lion’s share of the purchase price, you only need to borrow 20% as you are providing the rest in cash. You would own 80% of the property. There would have to be a cataclysmic event to wipe 80% off property values. So banks would consider your proposition to be zero risk. Surely then they can lend you the 20% to buy your property. You will easily pay the mortgage with freelance work but you have no track record of that. And in any case you’re taking all the risk. After all, you lose your life savings if you can’t pay and get repossessed. Risk to bank: virtually zero. Risk to you: your life savings. Can they lend to you?

In a word: no. Not even a specialist lender can. No lender can. Not without some proof of income. This means that all that very low risk business (and there is plenty of it; it used to be self-certification, or non-status lending) is kept off the lender’s balance sheet as they can’t lend on it. The high risk stuff, your 95% mortgages, where pay slips are easily obtained, is what can and does get lent on. The risk in lenders’ mortgage portfolios these days is likely to be much worse than it was pre-crash. Nice work FCA. (Not sure what FCA stands for but I can think of three words).

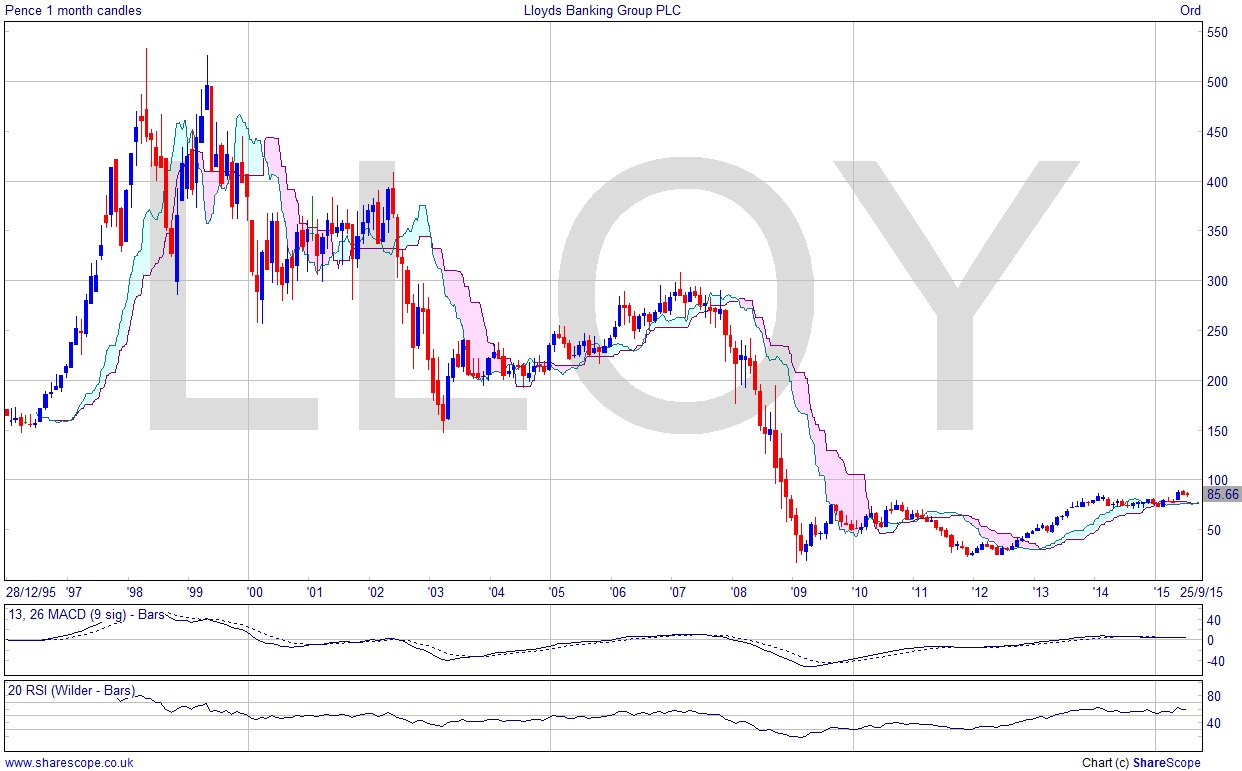

The banking sector is damaged, I don’t think it’s worth the risk. I still don’t have anything to do with it. And the charts support that stance. Barclays and especially Lloyds both utterly unremarkable.

Comments (0)