Value to be found in the latest IPOs? Hostelworld and Ibstock

Following a quiet summer period for initial public offerings (IPOs) the London new issue market has now come back to life. October saw seven new companies join the main market of the London Stock Exchange, raising a total of just under £1.65 billion. So far this year £6.1 billion of new money has been raised. While this is down from £9.3 billion at the same point last year, listing numbers are up from 49 to 54 companies.

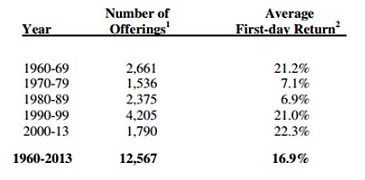

Many investors are attracted to IPOs, enticed by the many “hot” companies which often see large share price increases on their first day of dealings. A study released last year by Jay R. Ritter of the University of Florida looked at first day returns from certain US IPOs since 1960 (removing more volatile small caps) and found an average first day gain of almost 17% – not bad for just a few hours trading.

Source: http://site.warrington.ufl.edu/ritter/

To give some recent examples, this summer saw shares in US tech firm Fitbit open for trading 52% above its IPO price. Back in 2013 Twitter shares opened up by 73%. And just last week shares in Japan Post Holding (the largest global IPO of 2015) closed their first day of dealings up by 26% as retail investors drove secondary market demand.

Unfortunately, the average punter rarely has the opportunity to enjoy the first day gain effect as new issues are more often than not limited to institutional investors.

So how can the retail investor make money from IPOs?

Investment sage Benjamin Graham reminds us, “Most new issues are sold under favourable market conditions, which means favourable for the seller and less favourable for the buyer.”

While some IPOs outperform, it’s clear that many are over-priced. As such, classic fundamental analysis should always be applied before investing in any newly listed business.

On that note, here is a brief review of two interesting small/mid cap companies which have recently admitted their shares to trading in London.

HOSTELWORLD

Founded in 1999, just before the dotcom bubble burst, Hostelworld (HSW) provides an online booking platform for hostels and other types of budget accommodation. The Dublin based group is essentially a middle-man, taking commissions from accommodation providers for facilitating booking transactions with guests – typically 12-20% of booking values.

Key brands include Hostelworld, Hostelbookers and Hostels.com. Together these target an online travel agent market estimated to be worth $150 billion in 2013 and growing strongly on the back of the rise in mobile channels. At the end of August this year the company had 12,600 hostels and 21,000 other forms of budget accommodation on its sites, located across 170 countries around the world.

Cleaning the balance sheet

While the Hostelworld business model is easy to understand, the historic accounts are a bit more complicated.

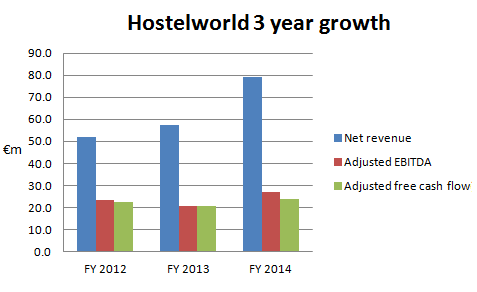

The P&L account shows growth in revenues of 39% in 2014 to €79.3 million, boosted by the prior year acquisition of Hostelbookers. More recently, sales growth in the six months to June was a more modest 8% to €43.9 million. However, operating profits slumped by 43% to €3.7 million as the firm ramped up its marketing efforts, launching the “Meet the World” brand awareness campaign.

The accounts then start to get slightly muddled. Prior to IPO at the start of this month Hostelworld was private equity owned, having the traditional highly geared balance sheet associated with the industry. As at 30th June this year total borrowings stood at over €324 million, with the associated interest charges causing the company to post consistent annual losses.

However, the situation has been significantly improved. At IPO the company raised a net €173.7 million. Combined with a debt for equity swap agreement the firm has now eliminated all of its borrowings and even has a modest net cash position. Future sets of accounts should be a lot simpler to interpret, although it will be some time before we get a clean set of figures.

Data source: Company prospectus

Worth a booking?

Given the change in the capital structure, increase in marketing spend and lack of forward guidance, Hostelworld is a difficult business to value. But I think we can get an approximation of worth from the firm’s historic adjusted free cash flow. This measure strips out the effect of the historic finance charges and shows what, in theory, could be distributed to shareholders.

Free cash conversion averaged 95% over the 2012-2014 financial years but dropped to 75% in the six months to June following increases in working capital and capex expenses. If we modestly assume that the first half performance is repeated then we are looking at free cash flow of at least around €15 million (£10.7 million) for the full 2015 financial year. At the current share price of 213p (up by 15% since IPO) the firm is capitalised at £203.5 million. That equates to a free cash flow yield of 5.26%.

In terms of income, the company is looking to pay a dividend of 70-80% of adjusted profit after tax. Taking free cash flow as a proxy for this and we are looking at a potential dividend yield of around 4%.

While this valuation looks reasonable, remember that the figures are all very “back of the envelope” due to the various issues discussed above. What’s more, competition in online travel is high and, as we have seen, marketing costs are eating into profits – the firm’s direct cost per booking rose by 68% to €4.7 in the past three years due to greater demand for paid internet search rankings.

Overall, Hostelworld is a growing business taking advantage of strong market drivers and is now in a much stronger financial position. I would prefer to see a clean set of accounts before buying at the current price. But if we see a fall back to around the IPO price of 185p then the shares might be worth checking into.

IBSTOCK

High on the current political agenda is the UK’s housing “crisis”. Driven by a rising population and low supply of properties, economist Kate Barker recently estimated that the country needs to build an extra 250,000 houses a year up until 2040 just to keep up with demand. And when we need houses we need bricks. This is where recently listed manufacturer Ibstock (IBST) comes in.

Operating in the UK and US Ibstock is a manufacturer of clay bricks, brick components and a range of concrete based products. In the last financial year just over half of revenues came from clients in the new build housing sector. Subsidiary Ibstock Brick is the UK market leader by volume of clay bricks, having an estimated 40% share. Over in the US the Glen-Gery subsidiary is a leading producer of bricks in the Northeast and Midwest regions, having an approximate 24% market share.

The business model is interesting in that Ibstock is “vertically integrated”. In English this means that the company owns its supply chain – over 150 million tonnes of clay reserves across quarries in the UK and US support the operations of 43 manufacturing sites. In the UK, Ibstock has production capacity of around 780 million bricks per annum, the largest in the country. This is set to expand further, with a new manufacturing plant in Leicestershire set to add approximately 100 million bricks to capacity per annum by the end of the decade.

Ibstock bricks. Source: Company prospectus

Building revenues

Ibstock had a tough time during the 2008/9 financial crisis, being forced to close some of its plants as demand for bricks slumped. But driven by the resurgence of the housing sector over the past few years the company has recently put in a very strong performance.

In the two years to June 2015 revenues grew by a compound annual rate (CAGR) of 15% to £395 million and adjusted EBITDA was up by 55% at £87 million. Adjusted free cash flow growth was also strong, rising by a CAGR of 37% to £72 million. Net proceeds of £83 million from the October IPO, along with a debt for equity swap similar to Hostelworld’s, left borrowings of £188 million on a pro-forma basis at the end of June, along with a pension deficit of £29.4 million. However, the strong cash flow performance means that the debt position looks comfortable to me.

Assessment

Ibstock’s listing perfectly demonstrates how IPOs can generate significant returns for professional advisors and selling shareholders. Private equity owners Bain Capital only bought the company from Irish builder CRH in December 2014 for £414 million before selling (or “flipping”) a stake at the IPO valuation of £770.5 million – not a bad return in little over 10 months – while advisors banked £14 million in fees and expenses.

While Bain retains a 47% stake in Ibstock the IPO sale raises questions as to whether the deal was done at the top of the cycle, something which often happens with large IPOs – Glencore springs immediately to mind. However, with the fundamentals of the brick industry looking strong, I believe that there could be decent returns available for new investors.

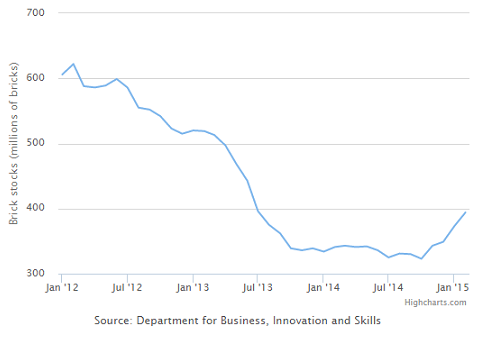

Following the closure of a number of plants as a result of the 2008/9 financial crisis brick supply has fallen at a time when demand is increasing, with the UK currently experiencing a supply shortfall. The Department for Business Innovation & Skills estimates that at the end of 2014 UK brick stock levels were the lowest in the last 25 years, falling to approximately 0.35 billion. This compares to pre-crisis brick levels of 1 billion.

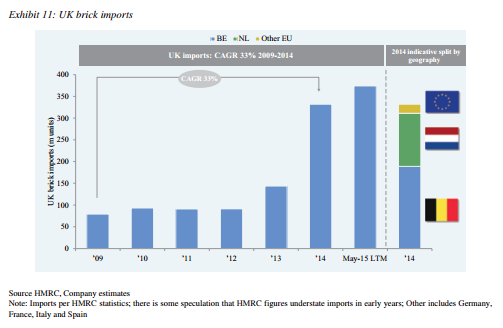

The shortfall has led to UK brick imports rising by a CAGR of 33% from 2009 to 2014 as the building industry tried to keep up with demand – see chart below. With the new Leicestershire facility opening soon, this creates an excellent opportunity for Ibstock to take advantage of the supply deficit.

Valuation

Ibstock shares are currently up by just 3% on the IPO offer price. Capitalised at £798 million the company might just make it into the FTSE 250 in the near term.

On a historic basis the shares trade on an attractive adjusted free cash flow yield of 9%. The dividend policy targets a pay-out ratio of 40-50% of adjusted profit after tax over a business cycle.

In terms of risks, investors need to be aware of the cyclical nature of the industry and that we are certainly not at the bottom of that cycle at the moment. I also note that AIM listed competitor Michelmersh Brick recently reported in a trading statement that, while selling prices have been ahead of budget, its own delivery volumes were below previous expectations due to a softening of the market.

But with strong fundamentals in the wider industry and a market leading business Ibstock looks like one to buy and hold over the coming years.

Comments (0)