The ECB Does It

There it is, European-QE, extended version, Part Two! Mario Draghi delighted investors yesterday with an extension of the current ECB asset purchase programme. Well…delighted them with the announcement, but as soon as he started speaking… It sometimes pays to keep your mouth shut.

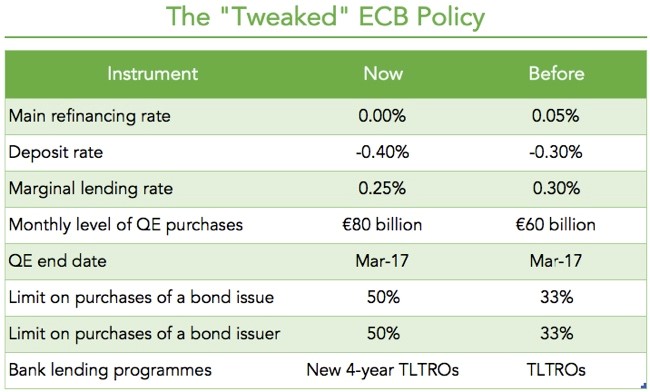

When the global economy is no longer able to provide enough magma to keep the equity market hot, investors place all bets on central planners, expecting them to come in support of markets and provide the magic that keeps the money flowing. While Janet Yellen is certainly placed at the top of investors’ preferences due to the global influence of her actions, Mario Draghi is eventually just behind, as he at least has been providing something lately. Yesterday was no exception, and Mario Draghi provided the market with much more than was really expected. On one side, the ECB ended cutting its key rates: the main refinancing rate was pushed to 0.00%, the lending rate tweaked to 0.25% and the deposit rate cut further into negative territory, this time to -0.40%. On the other side, the ECB enlarged its purchasing programme, which will now be targeting €80 billion in assets each month and will include corporate bonds. Starting on April 1, the ECB will purchase investment-grade euro-denominated bonds issued by non-bank corporations established in the euro area, which is a huge extension to the previous version of the programme.

The central bank also announced new four year TLTRO (Targeted Long-Term Refinancing Operations), aimed at providing long-term liquidity to banks at rates that can be as negative as the deposit rate. Limits on bond purchases were also tweaked to allow the ECB to purchase up to 50% of an individual bond issue and up to 50% of the total bonds of a single issuer. At a time the issuance of bonds by European governments is limited, the success of the central bank programme is heavily dependent on relaxing its self-imposed limits. For that goal the ECB raised the issue/issuer limits, cut rates (to allow the purchase of more negative yielding bonds) and expanded the range of assets to include corporate bonds. The announced extension of European QE was huge and drove a large upside movement in equities and pressed the euro down, as soon as it was announced yesterday at noon. The German DAX 30, for example, rose near 250 points to hit the 10,000 level in the one hour that followed the ECB press release. By then, the euro hit the ground, losing 170 pips from 1.0990 to as low as 1.0820. Everything seemed to be running perfectly and investors found a new support for their positive sentiment.

Well, everything was going well, but then the press conference started and Draghi elaborated on his plans for the future. Eventually he decided to put an end on an otherwise open-ended asset purchase programme, by saying that he doesn’t anticipate further rate cuts. That was one of the worst errors ever committed by Draghi at a press conference; the moment he told investors there’s nothing beyond.

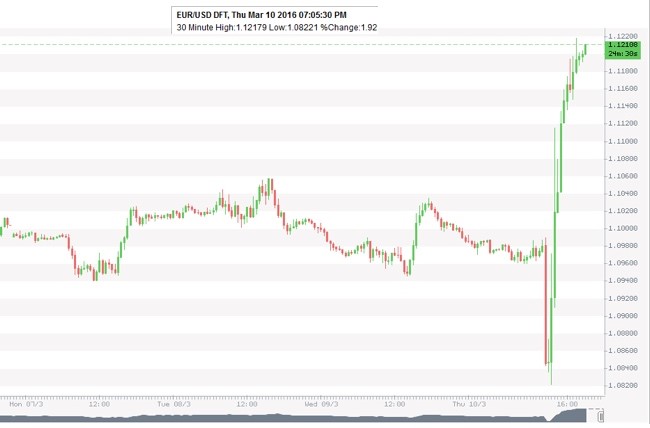

Financial markets are forward-looking. Give them asset purchases and they will rise as if those purchases would never end; tell them there is an end to the purchases and they will sink as if there is a crisis in the horizon. That single terrifying moment is very well depicted in the following picture:

Draghi’s unfortunate mix of words boosted the euro from 1.0820 to 1.1210, a near 400-pips rise, running in exactly the opposite direction as aimed by the ECB, which would expect its asset purchase programme to boost GDP and inflation through the exchange rate channel. It became clear from Draghi’s speech that the policy committee may not reach an agreement in the future for further QE-extensions if needed and that the bank is concerned with the effect new interest rate cuts may have in high street banks’ profitability. There is a feeling this is the closer we can get to the lower bound. While there’s nothing wrong with believing this, it sometimes pays to keep it to yourself, in particular if you’re the governor of a central bank. The ECB announced the “right” thing in the “wrong” way.

Regarding the programme itself, I believe it will do almost nothing for the European economy. Like I said many times in the past, asset purchases may help restore the pass-through of monetary policy at times there are huge distortions, but they should be used with parsimony. Europe shot itself with austerity policies at a time of recession and now will enjoy years of just mild growth (at most). The ECB is contributing to redistribute wealth and I really doubt it can build some. Faced with an extra demand from the ECB, investment-grade companies in Europe will have an incentive to issue bonds. But I ask myself whether they would use the proceeds to invest in real assets, expanding their businesses, or just repurchase shares and this way pay huge dividends to their shareholders. While demand keeps sluggish in the continent, companies will likely avoid investing, even if they can get the money for free. Regarding banks, while investors seem happy with the effect all this may have in the European banking sector, as major banks rose yesterday, I’m really a little more concerned. Over the period QE has been running in Europe, the Euro STOXX 50 ex-Banks declined 12% while the STOXX Europe 600 Banks declined 26%. QE seems harmful for all equities, and, in particular, worst for banks.

It’s time to wait and see. Most likely, the fresh QE stimulus will play nicely for equities for the next few days. After a huge negative reaction to Draghi’s words, markets will eventually correct and the euro come down from its record 1.1220 seen yesterday. But after that, it is business as usual, and that may not play as nicely. After all, while extending QE, the ECB revised all its projections down. GDP is expected to grow at a pace of 1.4% this year, 1.7% in 2017 and 1.8% in 2018. Just three months after the last projections and the ECB already cut 0.3% into this year’s expected growth. In terms of inflation, which would be expected to be impacted the most by QE, things are even worst. The ECB cut this year’s projection from 1.0% to 0.1% and next year’s projections from 1.6% to 1.3%. Not even in 2018 the central bank expects inflation to hit its 2% target (expected at 1.6%). With so much stimulus and so little results, investors will start scratching their heads sometime in the very near future and asking themselves whether QE is really good for equities or not. In the very short-term just enjoy the upside.

Comments (0)