Energy Investment Trusts – Not To Be Trusted

Investors in other sectors than mining won’t know my views on inappropriate methods of valuing them – in particular a ‘NPV’, which, to put simply, is the total sum of all future profit, with each year discounted by an appropriate factor to allow for inflation, or the cost of capital ,thought to be appropriate into the future. Those non-mining investors would be quick to notice immediate flaws in such an approach.

It is not used for ordinary sectors, where either a dividend yield or a PER is used as a measure of share value. Such sectors are usually fairly predictable, and company profits or dividend paying abilities don’t vary too much year by year, so those measures have stood the test of time.

But miners (and project companies) have extremely variable incomes and outgoings, the latter very large in early stages and (hopefully) switching suddenly to highly profitable incomes later. There is no feasible way to apply any value to them than to use the NPV approach, where the (discounted) value of that future income is set against the costs today of building their mines.

But the flaws remain. What ‘discount’ rate should be used in the calculation? Most investors would use what they think is the ‘cost of capital’ to the miner who is building the mine – ie what is it paying to banks or to investors to secure the funds to build. Its not just the direct interest rate or the price at which it issues shares to investors however. There is also the unknown rate of future inflation.

The problem is that a small change in the discount rate can produce large differences in an NPV – the higher the discount rate the smaller the NPV. Not only that, but one company might already have the cash to build its mine, whereas another with a similar mine might have to borrow it. The first can use a discount rate which only takes account of inflation. The other has to add the often much higher cost of raising it. Their ‘NPV’s will therefore be very different, even though their mine’s profitability and dividend paying ability will be the same.

Another problem comes when a miner starts to include income well into the future. If the ‘NPV’ method is applied to a normal share, you will find that to include forecast income beyond 10 years (or for highly rated shares maybe 15 or 20) produces a NPV higher than the price the shares are commanding in the market, sometimes considerably higher. In other words investors won’t give any credit for income that far into the future.

But miners typically have lives (through build, to end production) of 10 to 30 or 40 years. Why should investors rate them much more highly than they would a normal (usually more reliable) share? Yet brokers analysts very often do when they propose that an NPV based on such future income is the price investors should pay for a miners’ share.

In practice the sensible ones don’t. As in the notorious case of Sirius Minerals back in 2016, when the company itself, and its broker in trying to persuade investors what they should pay to raise the funds needed to build its potash mine, touted an NPV based share price which took in projected income 55 years into the future. Institutional investors didn’t agree, the fund raise failed, and Sirius went bust.

And lastly in any case. Why should an investor pay upfront for income 10-20 years into the future? – which is what he would be doing by paying the NPV. He is after all an equity ‘investor’ who by definition wants to make a profit. If he wants an assured future income he should buy an annuity from a reliable insurance company. That way he knows what fixed rate of interest he will earn and for how long. But if he wants to sell it again he won’t make any profit because, unless interest rates change, it will have a constant value – less whatever has been paid to him meanwhile.

There is no way he can be certain what income he will earn from investing in a miner. Yet he is effectively also buying an annuity, which if in practice the income he receives is exactly what was used to drive the NPV, would give him the discount rate as his return over the life of the mine. But a miner is risky, they hardly ever deliver the numbers used to calculate the NPV in the first place, which is why an investor shouldn’t pay anywhere near it if he wants to make a profit on his investment.

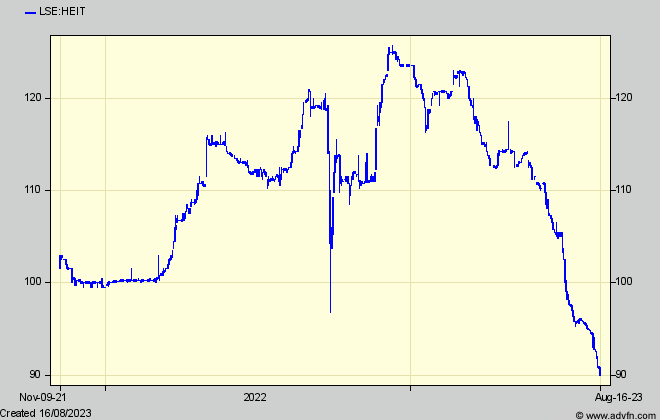

What has this got to do with the Energy Investment Trusts, which were all the rage until – starting last January – three favourites all have crashed? The longest running 10 year old TRIG (The Renewables Energy Group) is now 25% off its peak, Gresham House (GRID) by 30%, and Harmony (HEIT) by 26%.

These trusts seemed attractive because investing in ‘renewable energy’ was flavour of the moment and the business offered attractive dividends (at least initially). Then it was solar or wind generation, but now, belatedly, the companies are rushing into battery storage, so there have been bottlenecks in building them which is adding to other operational problems (erratic electricity demand) and causing some of the price declines. But another reason has been interest rates and the fact that the trusts and those promoting them all persuaded investors that an NPV was the price to pay for their shares. Maybe that irrationality is now coming to roost as higher discount rates cause those NPV’s to fall.

So why, in the face of the arguments I’ve used against miners, would the EITs, or the brokers floating them on the market, have done that? Traditional Investment Trusts have assets that are tradeable – ie normally shares which have a day-to-day value on a stock market and can be sold there and then, so backing the price the Trust commands

But EITs invest in ‘projects, held in the form of Special Purpose Vehicles – separate legal entities whose structure (assets, liabilities borrowings, profitability) might or might not be shown even in the accounts of their top holder – ie the Trust itself that shareholders have bought. As a result, the latter can’t necessarily know the value of each such investment, and neither can those investments be sold there and then. So the whole point of investing in a Trust is lost.

Instead of an investment which can be valued there and then, shareholders have to rely on what their Trust tells them it is worth. And what the Trust tells them it is worth is not any saleable value there and then of its projects – but their NPV’s – except that it doesn’t term them that (only in the very small print) and instead calls them ‘asset values’, which of course are the basis on which investors would value a normal investment trust.

That is despite that they are very different valuation concepts. So we have to ask again, why were they floated as if to be valued the same as a normal Trust.? Could the answer – Heaven Forbid – be that the founders and promoters made more money from the float than if valued conventionally.

For the answer we have to follow the life of a typical renewable energy project as it becomes part of an Energy Investment Trust.

Some small-time individual with land submits application for permission to build a solar or wind plant. He then sells the unlisted, unplanned but permitted ‘project’ to someone a bit bigger for a nice profit. The bigger one does a bit more planning and sells on again at another nice profit to someone like Harmony Energy (still small and unlisted with no real assets to speak of) who gets together a ‘seed’ portfolio or pipeline of projects and everything needed to be ‘shovel ready’, but not yet built.

Then along comes an ‘institution’ with the bright idea of turning the whole thing into a nicely profitable enterprise (for itself) – who acquires Harmony and turns it into a public company, which it then renames and floats off (projects not yet built) as a listed ‘investment trust’ or whatever (like EIS trusts before their tax benefits were withdrawn) whose investors put up the cash to build.

These new investors are told that the ‘asset value’ of their company will benefit from an enormous ‘uplift’ once the projects are built (just like the property companies 20 years ago before the whole sector crashed) and are also promised a very juicy dividend.

But that asset value is the NPV, which investors have to take on trust, because even in the listing prospectus there is no information about the profit forecasts and their lifespan that lay behind the calculation, nor of the discount rate used. Not only that, but the calculation is made by a subsidiary of Harmony itself.

Why is that important? Because on floating the shares Harmony takes itself a nice 15% of what it has calculated to be the ‘uplift’. Some of that of course is remuneration for getting the shovels ready but not anywhere near 15%. So it was that unlisted Harmony (and all others similar) came from nowhere only a year before with peanuts in its balance sheet and spending very little, to suddenly being rather rich.

So this has been a rather profitable game of ‘passing the parcel’ without very much real being achieved until the new investors were persuaded (by that ‘asset value – in reality an elastic NPV) to put up all the build cost. Admittedly in the early days and with a certain amount of assured contracts in place once built, investors could expect an attractive dividend (around 8% today). But they were used to Investment Trust shares being valued on the stock market on an ‘asset’ basis. And that continued on an assumption that ‘asset’ was the same as a NPV until very recently, when that assumption has been shown to be wrong.

On top of that, investors now have no guide to real, saleable, value. None of the companies/entities involved in this passing the parcel or floating off their ‘pipelines’ process shows its finances on Companies House (by changing names/groups etc) and even the listed Trusts are hard to follow because they shuffle their ‘projects’ around among themselves (at what price or profit we don’t know). And from now on, with erratic interest rates, and NPV discount rates whose choice is at the discretion of the companies, investors won’t be able to forecast how even the Truss ‘asset’ values will change

Perhaps a question investors should have asked themselves in each Trusts’ early days was why, if the ‘uplifts’ were going to be so massive, the ‘facilitators’ like Harmony Energy didn’t hold on to the projects themselves instead of floating off to retail investors.

So now perhaps we can understand why those ‘facilitators’ and their promoters used NPV’s as the price they persuaded investors to pay!

At the now lower share prices we are seeing I’m not saying these EITs aren’t worth buying for their dividends. Only that investors won’t have as much insight into their real, saleable, asset values as they are able to do with conventional investment trusts. Its why I think EITs aren’t to be trusted.

Comments (0)