Deflation? What deflation?

Central banks have a long track record of failure when it comes to stabilising the price of money. Many decades after their creation and they still know very little about the full consequences of their actions. But one can’t blame them, because there are so many variables in the process that aren’t under their control that keeping the value of money stable may only be achieved by chance or by magic. By “chance”, I mean by a mix of economic conditions that, without requiring any action from the central bank, contribute towards the achievement of the imposed goals. By “magic”, I am referring to the use of the rare ability some persons have to create an illusion of something that doesn’t really exist. Central banks are a mix of chance and magic!

If we go back to the 1980s and early 1990s in terms of monetary policy, we are faced with an era of complete failure. With the rare exceptions of Germany and Switzerland, central banks in other developed countries were just playing a game they couldn’t win. It was the era of monetary targeting, that is, central banks were directly targeting the monetary aggregates. Some were using narrow targets like M0 while others preferred the broad measures of money like M3. The idea was always to track a proxy for the money stock, gain control over it, and, as a natural consequence, keep prices on a tight leash. The BoE, the Fed, and the BoC are just a few examples of how miserably those plans went.

With the exception of Germany and Switzerland, central banks had to give up on targeting the monetary aggregates they first proposed to, as they were not able to keep the aggregates near their defined levels. At the same time, the volatility of the aggregates was so great that central banks didn’t even know what they were doing. They then decided that monetary aggregates shouldn’t be used as targets for monetary policy and should be abandoned or, eventually, kept just for recreational purposes. The words spoken in 1982 by Gerald Bouey, governor of the BoC, illustrate the sentiment at that time: “we didn’t abandon monetary aggregates, they abandoned us”. Even in cases where the money stock was more successfully managed, it seemed uncorrelated with the price level for the economy. Without a material connection between the two and with central banks mostly unable to control the money stock, there was no reason for them to maintain monetary targeting. It was time to start inflation targeting, which in the end has been claimed as a huge success.

There are two main reasons why monetary targeting was a failure. Firstly, most central banks have not seriously pursued monetary targeting. Secondly and foremost, there was a growing instability in the relation between the money stock and prices. Two question arise then:

– Could the central banks really control the money stock in the first place?

– When speaking about correlation between money and prices, which prices exactly were central banks referring to?

Most central banks in the developed world operate under a fractional reserve system; one that allows for commercial banks to create money. These banks concede credit up to the point it becomes unprofitable for them to concede more, and only later do they seek the required reserves – which the central bank is always willing to provide them with, to avoid a collapse of the financial system and any resulting systemic risks. The central bank expands base money at high-street banks’ will, not its own’s. The role of the central bank is passive in this process. It exists to serve high-street banks in their pursuit to maximise profits. Under such a system, only by chance would a central bank would be successful in achieving any monetary target. In general, the monetary targeting was deemed to fail miserably.

But now let’s pretend the central bank controls the money supply. Then many would argue that it still isn’t a good way of conducting monetary policy because there is no good correlation between the money stock and prices. But then one must additionally ask: Which correlation are they referring to? Are they using the consumer price index to track price changes?

The concept of inflation was tweaked so many times that no one knows for sure what it really is. Many say that inflation is a sustained increase in the general price level of goods and services in an economy over a period of time. But then one must think: Which goods and services? Should we consider the goods produced or all goods exchanged? Central bankers love to exclude energy and food to get the lowest possible inflation numbers. But, we shouldn’t forget that the central bank has good reasons to underestimate inflation. One of them is the fact the lower that number the greater the achievement of the central bank.

If we take the Austrian school view, inflation is an increase in the money supply, which may or may not lead to a rise in the prices of goods and services. Inflation and price increases are two different animals. When the money supply increases, the money available to make purchases increases. But the final increase in prices will depend on whether there is an increase in output or not. If not, more money is chasing the same volume of goods, and prices would tend to rise.

Other definitions consider inflation as a measure of the purchasing power of money. When we need more money to purchase the same things, then there is inflation. For this definition, CPI measures aren’t appropriate. The purchasing power of money involves measuring money against all other assets, them being goods and services or financial assets, produced in that period or pre-existing. If on average individuals commit 30% of their budgets to house purchases and 20% to stock market purchases, then the CPI measure will lose a large piece of the price action. Thus, when house prices are rising and the equity market is booming, money is being directed towards assets other than those captured by CPI. It may be the case that CPI is under control and the central bank seems to be doing a good job. It may even be the case the CPI is decreasing and the central bank is adopting anti-deflationary measures. But the reality may be in the exact opposite direction. With CPI capturing just part of the action, we should not expect a good correlation between the money stock and such measures of inflation.

Central banks are (or should be) mandated to maintain the value of money over time but all they do is maintain the value of a relatively small basket of goods and services at all costs, even if that means generating a huge increase in all other prices. What they do has more to do with illusion than with reality. They are indeed masters of illusion.

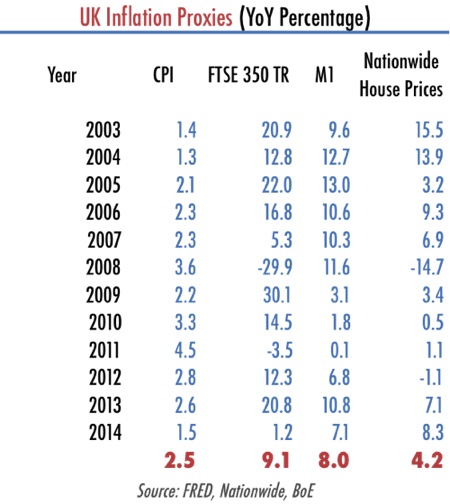

Just look at the above table. It tracks the value of four different measures that could very well be part of a broad inflation measure aimed at capturing the real change in the purchasing power of money. The first column shows CPI values, which have been more or less under control for the last 12 years, showing an annual growth rate of 2.5%. So, job done for the BoE.

But people do purchase houses too. So, why not track house prices on the inflation measure? The Nationwide House Price index has been rising at a 4.2% annual pace, which is 168% greater than the CPI. But then why not extend the measure to the stock market. People purchase shares. If we take the FTSE 350 Total Return as a measure of price increases, then prices have risen at a 9.1% annual pace, which is almost four times the CPI pace. Let’s use the example above in which the average person commits 30% of his budget to house purchases, 20% to share purchases and the rest to the items that are captured by the CPI. Then, the average loss experienced in purchasing power would have been 4.3% and not 2.5%.

If we alternatively measure inflation as being a rise in the money supply and if we track the money supply with M1, then average annual inflation has been 8.0%. Of all the measures the CPI is the one that most overstates the real value of money, as it is full of holes.

Recently the ECB found justification to launch a massive asset purchase plan to revitalise the European economy in the face of near-zero inflation. Stoking fear of a deflationary spiral, it was able to force the adoption of European QE. In Britain everyone is holding their breath after experiencing one month of negative inflation (as measured by CPI). But the Nationwide house price index rose by 8.3% in 2014 and M1 was up 7.1%, so the British should not be concerned with a lack of real inflation. At the end of the month you may spend less at Tesco but will end up losing the savings in other purchases you usually make.

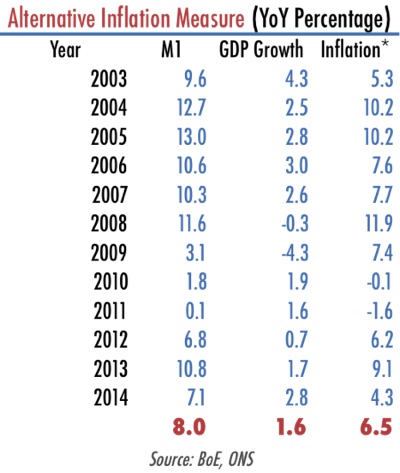

An alternative measure for inflation that I like is composed of M1 growth less GDP growth, as it is summarised in the table below:

While far from perfect, the main idea is that the money that is created without a corresponding increase in output must be spent in bidding pre-existing assets and does generate inflation. That is based on the quantitative theory of money. That being true, average inflation for the last 12 years has been 6.5% and not 2.5%. The difference between the two figures is what goes into the creation of asset bubbles.

Comments (0)