Selling the S&P 500 While Buying Energy

The last edition of Master Investor Magazine was dedicated to Warren Buffet, who is “perhaps the greatest investor who ever lived”. If anything is to be learnt from the “Sage of Omaha”, it is that investors should buy value and use the short-term market fluctuations in their favour to purchase great stocks at low prices. For both Buffet and his mentor Ben Graham (see Master Investor April, p.70), investing is about preserving capital over time while getting a decent return from it. In particular, for Graham, the crux of investment resides in researching companies to find those that are really valuable but have been dumped by investors, while avoiding everything that has been pushed higher by excess optimism.

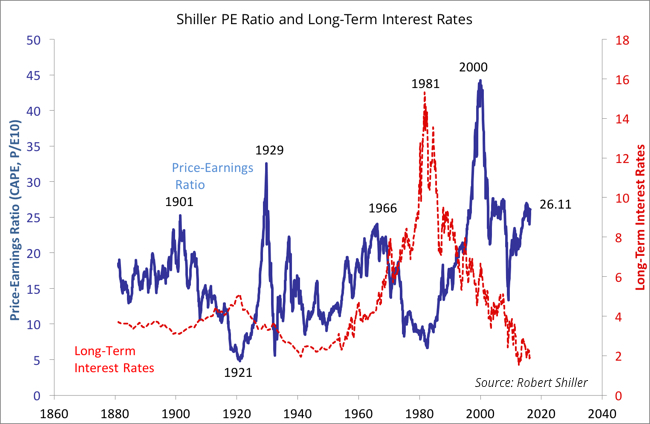

Speaking about optimism, I was shocked today when I looked at the latest value for the S&P 500 Cyclically-Adjusted Price-Earnings (CAPE) ratio, which currently stands at 26.11x. The long series of data kept by Professor Robert Shiller shows a historical average of 16.7x, which puts the current value 55% above that average figure.

Since the market recorded a bottom during the financial crisis of 2008-2009, investors have been enjoying a spectacular uptrend that has lifted the S&P 500 from a low at 666, hit on March 6, 2009, to yesterday’s close at 2,064. The collapse of Lehman Brothers and the subsequent downfall of the financial sector led to panic selling. Those brave enough to pick up stocks during 2009 were able to use Mr. Market’s negativity in their favour, benefiting from a huge undervaluation. But, after such a stunning uptrend, one wonders how much juice is still left. The quick rise in the CAPE ratio is a warning sign telling us that prices are rising more than the average earnings of the last ten years justify. Of course you may believe that such past history is worth nothing and that stocks can earn much more in the future than they earned in the past. If that were true, we could just disregard the CAPE because it would reflect an under-estimated denominator. But disregarding the past, particularly when it comes to companies that are part of the S&P 500, is always a mistake because historically we have witnessed a large degree of mean reversion in earnings. Companies cannot experience rapid growth forever. The current valuations rely on excessive optimism regarding earnings growth. No matter where you look you will see a scenario of low growth, low inflation and low interest rates. Under such a global scenario, how can US stocks reverse two years of stagnation and double their earnings, for valuations to return to earth? I’m not really enjoying the same optimism as the market, as I see a much higher likelihood for the next adjustment in the CAPE ratio to be more through the numerator (price) rather than through the denominator (earnings).

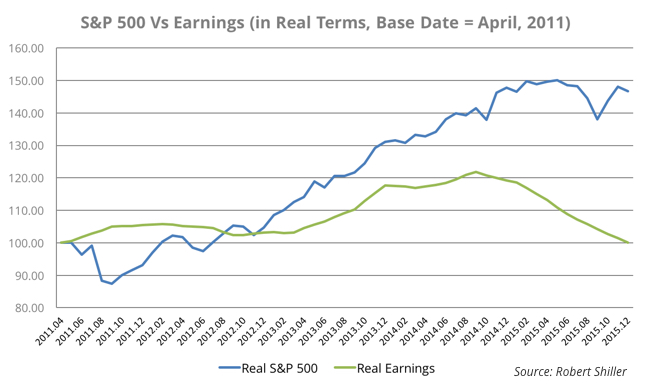

Speaking of earnings, the current earnings season is coming to an end in the US. According to Deutsche Bank’s data, the earnings reported by S&P 500 companies fell by 6.3% year-on-year, in the fourth consecutive quarterly decline and the steepest since the crisis of 2008-2009. In fact, the situation is even worse than that, as although earnings started declining one year ago, they stagnated two years ago. If we take the earnings data in real terms, current earnings are at the same level they were at the beginning of 2014 – and all this while the S&P 500 rose 50%.

Corporate America is making money, but not more than it was two years ago. Earnings have stagnated while share prices have risen, much because of expansionary monetary policy and bold share repurchase programmes. But, as I mentioned in my blog “The US Economy Is Slowing…Again”, the repurchases aren’t sustainable because companies aren’t generating enough cash flows to finance them. Net debt is rising like it did before the 2008-2009 crisis and may become a problem in the near future. As a whole, the S&P 500 is overvalued and is near the point where Graham and Buffet would just avoid it. I believe that any upside left for this market is based on sentiment and not in fundamentals. Until the point where I see companies showing some earnings growth, this market is a sell candidate.

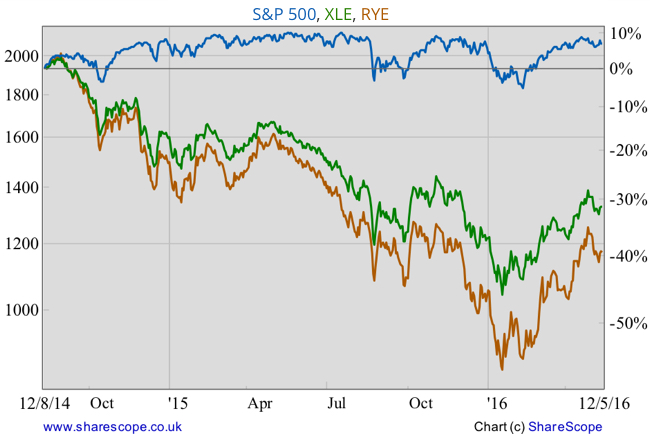

But, it seems that not everything is in an overbought state. A closer look into CAPE ratios inside sectors shows one single area of deep value – energy. Energy companies have been severely punished by a bear market in commodities but may experience some relief now, in particular because the FED is stuck for the rest of the year. I’m really not seeing a way for the FED to hike rates. The country needs a weaker dollar for corporations to be able to get something on their overseas earnings. A rate hike would most likely push the US economy towards recession, which is something Janet Yellen certainly wants to avoid. But a failure to hike rates would also not be enough to propel the market as a whole at this point, because low rates haven’t been enough to push consumption higher in any meaningful way. The economy and the central bank are stuck between a rock and a hard place.

In the meantime, the energy sector will likely continue to offer the best opportunities, at least in fundamental terms. The current CAPE for the sector is around 13.60x, almost half the CAPE for the whole market. After a painful adjustment in the recent past, these companies may well outperform the rest of the market.

One way of getting exposure to the US energy sector is through the Energy Selector Sector SPDR Fund (XLE), which includes many of the world’s largest oil producers. Because of concentration issues, an alternative to this ETF is the Guggenheim S&P 500 Equal Weight Energy ETF (RYE), which gives equal weighting to its holdings.

Comments (0)