Opportunities in small cap healthcare – MAGAZINE EXCLUSIVEMAGAZINE EXCLUSIVE

MAGAZINE ARTICLE

This article first appeared in Issue 40 of Master Investor Magazine.

Click here to download the article as a printer-friendly PDF

Get this article and many more – for free! |

As discussed elsewhere in this issue of Master Investor Magazine, the healthcare and biotech sectors provide significant opportunities for investors. It is my job to provide analysis of small cap opportunities, so before heading into my three small cap picks, here are three pointers to look out for when investing in the medical minnows.

Firstly, small cap investors should avoid having too much portfolio exposure to companies whose fortunes rely heavily upon the success of just one drug candidate. Some readers may remember London listed scar reduction company Renovo, whose shares collapsed by 75% in just one day in 2011 after announcing that trials of its flagship product Juvista were unsuccessful. More recently, shares in Faron Pharmaceuticals (LON:FARN) collapsed by 86% in one day after data from a Phase III study of itsvascular leakage and organ failure candidate Traumakine showed it did not meet its primary endpoint.Remember that while management may be “optimistic” about the prospects of a drug candidate, and that earlier stage trials may have been positive,the key for success is in the Phase III data.

In a related issue, attention should be paid to value. A company might have a potentially world beating product but investors should always ask if it’s worth paying the current price given the risks involved. To give one example, Circassia Pharmaceuticals (LON:CIR) was valued at a whopping £581 million at IPO in March 2014. The shares subsequently collapsed after a Phase III study in 2016 reported that its cat allergy drug candidate performed no better than a placebo.

Another top tip is to consider a “picks and shovels” strategy by investing in areas such as diagnostics and biotech/healthcare service providers. These companies will earn money regardless of whether their customers’ research is ultimately successful. One particular business doing well in this area is antibody developer Bioventix (LON:BVXP), shares in which have risen from 520p to 2,978p since listing on AIM in April 2014.

Noting the points above, here are three interesting small cap healthcare/biotech businesses which I believe are worthy of further investigation.

POLAREAN IMAGING

Polarean Imaging (LON:POLX) is a drug-device combination company operating in the high resolution medical imaging market.Its focus is on developing equipment that enables existing MRI (magnetic resonance imaging)systems to achieve an improved level of imaging when analysing the pulmonary function (respiratory system). It does this by specialising in the use of so called “hyperpolarised Xenon gas” (129Xe), or HPX, as an imaging agent to visualise ventilation and gas exchange. Polarean’s technology has been in development for almost 20 years, with the company having built up an IP portfolio based on 29 patents which cover four broad areas and extend into 2034.

To give a basic description of how the technology works, prior to an MRI scan a patient breathes in a small amount of inert HPX. This provides an extremely strong signal, c.100,000 times stronger than a conventional MRI signal, which can be picked up by the scanner. This transforms the MRI from a technology that is not applicable to the lungs into one that is able to provide multiple images of the lung structure and function in one 10-20 second breath-hold. This is important as MRI technology can help diagnose lung disease earlier, identify the type of intervention likely to benefit a patient and to monitor the efficacy of treatment.

Pulmonary disease is an area of significant unmet medical need at present, with Polarean’s technology providing a novel diagnostic approach, offering a non-invasive and radiation-free functional imaging platform which is more accurate and less harmful to the patient than current methods. Providing significant long-term opportunities for the company, it is estimated that more than 30 million people suffer from a chronic lung disease in the US alone,with it having an economic burden of over $150 billion.

Revenues already flowing

Unlike many life sciences companies Polarean is a revenue generating business, with current products used as “add-ons” which are compatible with existing MRI systems. Polarean made revenues of $1.24 million in its last financial year, although $0.65 million of this was from grant funding.

Current products include: the polariser, with the latest model being the Polarean 9820 Xenon Hyperpolariser; HPX gas, which is polarised within the polariser; the dose delivery inhalation bag,made of HPX-compatible impermeable plastic materials and a mouthpiece for ease of inhalation; and the Polarean 2881 Polarisation Measurement Station, which provides a calibrated measurement of the polarisation of hyperpolarised gas within the dose delivery inhalation bag. The company also develops and manufactures high performance MRI radiofrequency (RF) coils which are a required component for imaging 129Xe in the MRI system

Trial acts as potential milestone

To date, Polarean has generated revenues from selling its gas, polarisers and disposables for research use only to academic medical centres. However, to allow its products to be sold into a wider market, a Phase III clinical trial of the company’s technology is expected to begin imminently (as I write) at US research hospitals Duke University Medical Center and the University of Virginia. The trial, which has been agreed with US regulator the FDA (Food & Drug Administration) will include 80 patients and compare Polarean’s 129Xe MRI contrast agent with an older nuclear medicine agent, 133Xe, to characterise lung ventilation. It is expected to last for approximately 18 months, including the time required to prepare a New Drug Application (NDA) with the FDA.

Polarean is currently targeting FDA approval during 2020, following which it will be able to begin marketing and sales in the US. A direct sales force is planned to be hired, as opposed to distributors, giving the opportunity for higher margins to be achieved. Providing additional opportunities in the long term, the FDA has also indicated its willingness to accept a very broad indication for use for the company’s technology – for the evaluation of pulmonary function – as opposed to its use being limited to any particular pulmonary disease or condition.

One for the long term

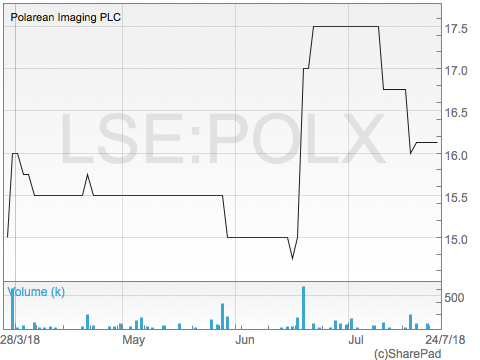

Polareanis a recent addition to the markets, having listed on AIM in March this year raising £3 million (£2 million net) to fund the Phase III trial and working capital. Trading in the shares has been light since the IPO, with a range of 14.5p to the current high of 17.5p being seen, a recent boost coming on the back of an investor symposium on 19thJune. At the current price the business is capitalised at just £12.85 million.

The key upcoming driver of the shares will clearly be the results of the Phase III trial. While the trial itself is expected to take around a year, there could be interim data releases to act as a share price catalyst. While current funds look sufficient to complete and report the trial, the company does look like it will need further funds to commence early marketing exercises in the US.

In any case, I believe investors should take a long-term view here. As discussed above, pulmonary disease is an area of significant unmet medical need. The company’s products provide an attractive complement to current MRI units, with a large installed base of scanners being in place that can be used to implement Polarean’s technology. The US seems a good initial market to go for, with a 2013 study from Kaiser Family Foundation finding that the US has the second highest number of MRI units per million of population, at 35.5, behind Japan, at 46.9.

CARETECH

AIM listed social care services provider CareTech (LON:CTH) is a company I have covered a couple of times before in Master Investor Magazine. The first time was in March 2016 at 235p a share and then in June last year at 442p. Following a recent slip back to 387p, I now see another attractive entry point for both new and existing investors.

Founded in 1993 and listing on AIM in 2005, CareTech supports adults and children with more than 292 specialist social care services via the five divisions of adult learning disabilities, specialist services, young people residential services, foster care and learning services. These are provided to end customers via a portfolio of over 215 homes throughout the country, with CareTech being paid for its work by local authorities and health service commissioners.

Growth over the years has been driven by a number of factors including increased outsourcing by local authorities, shortfalls of specialist beds and higher regulatory burdens. But despite annual revenues having grown from £22.5 million to £166 million from 2005 to 2017 CareTech still only has a small share of what is a fragmented market for social carein the UK, estimated by the company to be worth c.£12.6 billion per annum.

Care to grow

In 2017 (the 12 months to September) CareTech had a strong financial year, with the corporate highlight being the raising of £39 million in a “very oversubscribed” placing of new shares. The money was spent on acquiring new additions to the care home portfolio. Overall capacity increased by 215 placesto 2,534 by the period end. On the back of that, revenues for the year rose by 11.4% to a record high of £166 million, with underlying EBITDA up by 7.5% at £39.9 million. As a result, the total dividend for 2017 was up by 7% at 9.9p per share.

Decent growth continued in the first half of the current financial year, with revenues growing by 11.2% to £87.6 million in the six months to March 2018 as net capacity edged up to 2,572 places. Underlying EBITDA increased by 6.6% to £19.5 million although earnings fell to 9.2% to 14.86p, largely as a result of the increased number of shares in issue following the placing. Nevertheless, the interim dividend was increased by 6.1% to 3.5p per share, with net assets growing by 6.7% to £208.3 million at the period end.

Time to top up?

Since reaching an all time high of over 450p last June shares in CareTech have drifted down to the current 387p despite the company’s operations ticking on nicely. At the current price the company trades on a historic price to earnings multiple of just 10.2 times,which looks incredibly cheap in my opinion given the company’s track record of growth and solid business model. What’s more the historic dividend yield is reasonable 2.56%, with the current market cap of £292 million supported by the £208.3 million of net assets on the balance sheet as at the end of March this year. This included £300 million worth of property assets.

Assuming access to finance is not a problem, I believe that the company can continue to grow market share over the coming years, with the current strategy continuing to focus on attractive bolt-on acquisitions, along with potentially larger deals.

MEDICA GROUP

Medica Group (LON:MGP) is the UK market leader by revenue in the provision of teleradiology services.Teleradiology refers to the electronic transmission of radiological patient images, such as x-rays, Computerised Tomography (CT) scans and MRI scans, from one location to another for the purposes of diagnostic interpretation and reporting. Through teleradiology, images can be transmitted from parties that undertake the diagnostic imaging itself, such as a hospital, to a radiologist who can review and report on the images remotely.

In the UK, the NHS is the main player in what is a growing teleradiology market. The Royal College of Radiologists, for example, has forecast for England that CT scans will continue to grow at a CAGR of 10.1% between April 2014 and March 2023and that MRI scans will continue to grow at a CAGR of 12.3% over the same period. This increased number of scans, combined with a shortfall in the supply of radiologists, means that the teleradiology services offered by Medica are increasingly in demand.

Medica currently offers three main services to hospital radiology departments: NightHawk,an out of hours emergency reporting service focused on short turnaround times; routine cross-sectional (Routine CS) reporting on MRI and CT scans, and routine plain film (Routine PF) reporting on x-ray images. Across all three services Medica offers hospital radiology departments the ability to manage their workflow more efficiently and flexibly, providing fast access to specialist consultant radiologists who may not be available to that hospital at the relevant time or not at all.

Recruitment of new radiologists has been a key focus of the company in recent times, with 318 contracting with the company as at the end of February this year. This represents the largest cohort of consultant radiologists in the UK outside the NHS. Medica also has a bespoke IT platform that provides a link between a hospital’s Radiology Information System (RIS) and its consultants.This enables it to provide more than 1.5 million examinations annually across its customer base of more than 100 NHS Trusts, private hospital groups and diagnostic imaging companies that provide it with high quality repeat revenues.

Double-digit growth

Medica listed on the main market of the LSE in March last year, with the IPO seeing £121 million raised at 135p per share, although £106 million was for selling shareholders. The business has performed well in recent years, delivering consistent double-digit growth, with the company reporting in its IPO admission document that revenues grew by a CAGR of 27% between 2013 and 2015, with EBITDA up by a CAGR of 20% over the same period.

However, Medica had a bit of a wobble at the start of 2018, announcing in January that results for 2017 would be slightly behind market expectations due to certain capacity constraints and a softening of demand in the final quarter. The shares subsequently lost around 22% of their value over the two days following the announcement and have gone on to reach an all time low. This looks harsh in my opinion given that the results themselves showed a continuation of the double digit expansion.

For the year to December 2017 overall revenues grew by 18.2% to £33.7 million, driven by sales from Nighthawk growing by 24.1% and Routine CS growing by 19.4%. Pre-tax profits grew by a more pronounced 48.6% to £8.85 million, with earnings up by 39% at 6.92p per share. The net £12.4 million raised for the company at IPO was mainly used to pay down borrowings during the period, with net debt falling from £22 million to just £5 million by the year end. As a result of the good performance Medica announced a maiden final dividend of 1.1p per share to give a proposed total dividend for the year of 1.65p

More recently, a brief statement at the company’s AGM in May suggested that 2018 has started well, with performance being in line with expectations and recruitment of radiologists continuing to be strong.

Growth and income

While Medica shares have bounced back from recent lows of 117p, at the current 129.8p they remain below the March 2017 IPO price despite the company having seen a full year of decent growth since then. At the current market cap of £144 million, the shares trade on a multiple of 18.8 times historic earnings, which does not look bad value for a company which has consistently grown revenues and profits in the low to high twenties on a percentage basis over the past few years.

Analysts at house broker Investec have a 210p target price for the stock, implying 62% upside from here. There is also a progressive dividend policy, with a 2.1p payment pencilled in for 2018, equating to a yield of 1.62%.

|

Comments (0)