How to profit from the latest small-cap IPOs

After two moribund years, the small-cap IPO markets have taken off again. According to data from the London Stock Exchange, 61 companies joined AIM in the nine months to the end of September this year, up from the total of 55 that joined in 2019 and 2020 combined, with three months of the year to go. This year’s AIM new issues have raised a total of £1.19bn between them to advance their business plans and grow their operations. Here are three recent new issues which I believe could make investors some decent money over the next few years.

Northcoders Group

Technology jobs are in high demand around the world. According to the U.S. Bureau of Labor Statistics, employment of software developers, quality-assurance analysts and testers is expected to grow by 22% from 2020 to 2030, much faster than the average for all occupations. What’s more, the UK Commission for Employment and Skills estimates that 1.2m more technically skilled people are needed by 2022 to satisfy future skills needs in the UK. Taking advantage of these trends is Manchester-based training provider Northcoders Group (CODE), which joined AIM in July this year.

Northcoders provides a range of software-coding training programmes, to both individual and corporate customers, online and in the classroom. Courses, which typically attract more applicants than there are places available, cover a comprehensive range of commonly used coding languages including Node.js, SQL and DOM. The business model sees courses typically paid for in advance by private individuals or over the duration of the course via government-funded apprenticeships or on agreed terms with student-finance providers and corporate customers. Apprenticeships are a core area of growth for the company. It became a direct apprenticeship provider in December 2020, enrolling its first students shortly after. The training works too − a survey by the company found that around 95% of students gained employment within 44 days of completing a training course.

This summer’s IPO brought with it £3.5m of new funding at 180p per share, the net proceeds of which will be spent on rolling out the model geographically. An additional hub in Birmingham is planned, adding to the existing hubs in Manchester and Leeds, with two more expected in 2022. The ultimate goal is to create a substantial network of Northcoders hubs across the country. The director’s interests are well in line with investors here; they still own 38% of the company after going public.

C# numbers

Having a classroom-based operation, Northcoders was affected during the pandemic after it was forced to close its physical sites. Before that, growth was strong, with revenue more than doubling from £0.6m in 2017 to over £2m in 2019, on the back of student numbers growing by 80%. While 2020 was a difficult year, with revenues slipping to £1.3m and a loss posted, it could be a blessing in disguise in the long term, with the pandemic accelerating the digital transformation of businesses and highlighting the need for coding skills.

The six months to June 2021 saw Northcoders return to profitability despite teaching limited to online only for most of the period. Revenues surged by 55% to £1.09m, with profits at the pre-tax level a modest £18,000. This is a high-margin business, with gross margins in the low 70% range and, combined with relatively fixed costs, providing a strong operational gearing. On the balance sheet, Northcoders was well-funded, with cash rising to £2.46m at the end of August following the IPO fundraise. Borrowings are low at just £0.84m.

The outlook for the full year was positive, with trading in Q3 set to continue at record levels. Contracted bookings stood at £2.87m, around 96% of the target revenue for FY2021 and providing excellent near-term earnings visibility. The performance was helped by a 162% increase in applications for the company’s “bootcamp” programmes − intensive, 13-week courses designed to turn learners into work-ready software developers. There was also the award of a £1.65m government-funded scholarship programme. Reflecting the high demand for places, this was oversubscribed within five days of launch, despite the expectation of being offered over nine months.

Value hack

Northcoders is a true micro-cap company, capitalised at just £12.5m. But there is a lot to like here, in terms of growth and positive industry trends, so it might not stay that small for long. Broker WH Ireland has some pretty ‘racy’ forecasts over the coming years, expecting modest pre-tax profits of £0.1m for 2021 to grow to £0.8m next year and £3.2m in 2023 as the operational gearing kicks in. It reckons the shares are worth 210p on a fair-value basis, which would put them on a very cheap-looking multiple of just 4.9 times the broker’s 2023 earnings forecasts. In my view, if Northcoders meets those forecasts the valuation could be much higher. There is also a maiden dividend of 4.3p being pencilled in for 2023, in line with the company’s stated policy at IPO, equating to a yield of 2.4% at the current price of 180.5p.

Lords Group Trading

Some firms join the market in order to raise money and use their shares to pay for earnings-enhancing acquisitions. This next company did just that, with an ambitious plan to almost double revenues over the next three years.

Founded over 35 years ago, Lords Group Trading (LORD) is a specialist distributor of building, plumbing, heating and DIY goods. It mainly sells its wares to local tradesmen; small-to-medium-sized plumbing and heating merchants; and construction companies. It also retails directly to the general public from over 20 sites around the country.

The larger of the company’s two divisions by revenue is heating and plumbing where Lords acts as a specialist distributor of heating and plumbing products to a UK network of independent merchants, installers and the public. The division offers its customers an attractive proposition through a multi-channel offering, with nine locations enabling nationwide, next-day delivery service. Secondly, the merchanting business supplies building materials and DIY goods through its network of merchant businesses and online-platform capabilities. It operates both on the ‘light side’ (building materials and timber) and on the ‘heavy side’ (civils and landscaping), through 25 locations in the UK.

The IPO on AIM in July this year saw £30m raised for the company at 95p a share, with £24m of this being used to pay down debt. Some of the remainder will be used to fund the growth by acquisition strategy, with Lords having a strong track record of deal making. The company has acquired more than 13 businesses in the last 10 years and with an estimated 2,300 builders’ merchants in the UK, and 40% of these independent, there are plenty of further opportunities. As it grows its national presence, Lords is looking to grow revenues to £500m by 2024, almost double the £288m posted in 2020.

Building business

Boosted by contributions from a number of acquisitions, Lords had an excellent year in 2020, with revenues almost trebling. Growth continued in the first half of the current year too, with sales surging by 44% to £179m and pre-tax profits coming in at £4.5m from a loss of £0.3m. Operational highlights included digital sales growth of 42% and the integration of two acquired businesses − MAP Building & Engineering Supplies and Condell, with the deal pipeline said to remain robust.

While this is a business with relatively low gross margins (16.4%), cash flow is strong. There was an £8.2m inflow from operations during the half year, well-ahead of pre-tax profits, mainly due to the adding back of certain non-cash charges. While net debt was £25.6m at the period end, the net proceeds of the IPO received in July will have practically eliminated this.

During its brief time on the market, Lords has made one acquisition, that of a west-London branch of Nu-line Builders Merchants. Nu-Line is an independent builders’ merchant specialising in the supply of general building materials including timber, paint, electrical, ironmongery and plumbing. At £0.6m, this was a small deal, but priced at just three times the branch’s historic EBITDA, it looks to have been done at a good price. Furthermore, Lords expects its EBITDA to grow to £0.8m in the first full year of ownership in 2022, demonstrating the benefits that bolt-on deals like this should deliver.

Owzat?

Shares in Lords have had a good start to trading on the markets, rising by 42% on the IPO price to the current 135p. That is only just short of broker Cenkos’ fair-value price of 144.5p but I see significant potential for long-term growth here, given the fragmented nature of the industry, the company’s experience in acquisitions and a strong balance sheet to fund growth. The paying down of the debt following the IPO fundraise is expected to significantly reduce interest charges and create a more stable platform from which to pursue growth.

With a 0.63p dividend announced in the interims, assuming a traditional one-third/two-thirds split, we are looking at a total payment for the year of 1.89p. That yields a modest 1.4% at the current price. There should be scope for significant increases however, with Cenkos expecting the company to deliver free cash flow of around £14m per annum in the medium term.

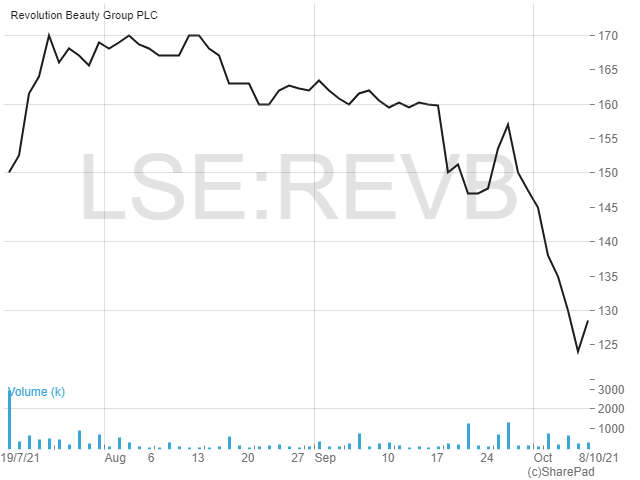

Revolution Beauty

According to analysts at Common Thread Collective, the global beauty industry brought in revenues of $483bn in 2020 and is expected to rise to $716bn by 2025. Looking to expand its presence in this growing market is Revolution Beauty (REVB), a company which creates and sells ranges of beauty products such as makeup, haircare and skincare in a number of countries around the world, via an online and in-store model.

The company was founded in 2014 to ensure that high-quality, cruelty-free cosmetics and skincare are affordable for everyone. Today it sells its range of around 4,000 products in around 11,000 stores via partnerships with key retailers in 45 countries. These include Superdrug and Boots in the UK, Ulta and Target in the US, Priceline in Australia and Watsons in Turkey. Online, products are sold via digital partners including ASOS, Boohoo and Amazon. Revolution launched its own direct to customer online portal in August 2019 and saw one million customers in just over a year. Product development has been key to the company’s success, as new items can go from concept to launch in just 16 weeks. The company analyses the latest trends and social media to come up with ideas.

Revolution’s significantly oversubscribed IPO placing in July, priced at the top of the valuation range, raised £110.7m gross for the company at 160p per share. With significant opportunities to grow the brand around the world, the company will be spending the money on growing its direct online operation, looking for new digital and in-store partners, expanding into new countries and launching new products.

Good foundation

From a standing start, Revolution Beauty has grown rapidly in a short period of time. Up until FY 2019 revenues almost doubled on average every year, growing at a compound rate of 99%. In its last full financial period, the 14 months to 28 February 2021, revenues hit £157.6m, with adjusted EBITDA of £13.1m.

No results have been released during the company’s time on the market, but a recent trading update confirmed that sales grew by 35% to £78m in the six months to August 2021. Some operating highlights included adding over 200,000 customers to the online platform and doubling international online sales in the US, Australia and New Zealand. In the US, sales grew by over 90% overall, helped by launching in 1,800 Target stores, with the country set to become the largest by revenue shortly.

A number of initiatives are expected to continue to drive growth in the second half of the year. New digital and retail distribution and country expansions are planned for H2, with the Makeup Revolution brand expanding into over 350 of the largest Boots stores across the UK in early 2022. New product lines are also expected to continue growing, with the Revolution Skin category growing revenues by over 34% in H1 and the Revolution PLEX Haircare range now stocked in over 250 Boots and 300 Superdrug stores.

Overall, management are confident of achieving full-year expectations, with strong sales as the beauty industry enters its seasonal peak-trading period of September to November. Calming investors’ fears, the company also flagged that, having reacted to current, global, supply-chain disruptions, it does not expect its ability to offer products to its customers to be affected.

Looking cute

While shares in Revolution Beauty have seen highs of 170p since IPO, they currently sit at 127.5p following a surprisingly negative reaction after the half-year trading update. Analysts at Zeus Capital are looking for strong growth here, with pre-tax profits expected to almost double, from £10.2m to £20.3m, from 2022 to 2024. While the forward earnings multiple for 2024 is a rather ‘chunky-looking’ 26.5 times, the growth-focused price-to-earnings growth (PEG) ratio for the year is a much more reasonable 0.9 times.

So, Revolution is a company for growth-seeking investors, given itse ambitious plans. Chief executive and co-founder Adam Minto said in a recent interview that he believes the business is capable of becoming one of the top-20 beauty brands in the world over the next few years, with revenues in the billions. At that stage, if it comes, I can image it being bought by one of the bigger industry players for a much higher price than today’s. To give some idea of the upside here, Zeus’s blue-sky scenario analysis sees scope for £69m in EBITDA over the medium term, which on an EV/EBITDA multiple of 15 times would imply an enterprise value of over £1bn.

Comments (0)