Passive strategies for downside protection

With a ‘second wave’ of Covid-19 seemingly upon us, Filipe R. Costa looks at passive strategies to protect against the downside.

Last month, I wrote about rotating from growth to value. In my view, although there’s still upside potential in the market, the odds of a bear market are rising. This is the longest bull market we have ever witnessed. The S&P 500 has risen at a pace of 11.4% over the last 10 years and the Nasdaq 100 at a stratospheric of 19.1%. If you had invested $50,000 in the Nasdaq 10 years ago, you would currently be sitting on more than $287,000. And all this while the global economy grew at a very mild pace. The developed world has experienced sluggish growth since the beginning of the century. However, the stock market has been rising fast. Some would say that the elevated returns are a consequence of the recovery from the 2007-2009 crash. But we could also say that the crash was the consequence of the previous returns being disconnected from reality. Will this happen again?

Corporate profits aren’t rising as fast as stock prices and price multiples are very high at the moment, in particular for tech stocks. Additionally, the US election next month is a material uncertainty. Election disputes are very likely, as hinted at by Trump. This would contribute to heightened volatility. Moreover, we shouldn’t forget that the current uncertainty is not only about politics and skyrocketing valuations. We’re in the midst of a pandemic. There are 34 million reported cases of SARS-Cov-2, of which more than one million resulted in death. While the virus seems to be less deadly at this point, the number of new cases is rising quickly. As we approach the cold season in the northern hemisphere, the number of cases is expected to rise even faster. When SARS and influenza mix together, we just don’t know what might happen. And, we shouldn’t rely on a vaccine, at least not for this coming winter, as none is fully developed yet and it will take time for a vaccine to reach the population in a way to provide herd immunity.

With all of the above in mind, I believe it makes sense to look into ways of protecting against downside risks. It’s not about jumping out of the market but just getting some insurance against potential negative developments.

Thus, the question is: what can an investor do to protect against the downside? Let’s look into it.

Alternatives to the conventional stock/bond holding

Today, the real problem faced by an individual investor willing to commit funds to the right places is deciding on the exact layers to add to a portfolio. The simplest strategy is to purchase a portfolio with just two ETFs: a broad equity market ETF and a broad bond market ETF. A very good choice for this aim in terms of its broadness and cheapness would be the Vanguard Total Stock Market ETF (NYSEARCA:VTI) and the Vanguard Total Bond Market (NASDAQ:BND). The only decision to make thereafter would be on the exact proportion of each to hold, often departing from a common 60-40 stock/bond holding.

Under such a conventional investment setting, it’s easy to protect against the downside. Just decrease the stock holding while increasing the bond holding. Possibly to 30-70 or even 20-80. But at the current interest rate levels, no bond offers a satisfying income. Not even corporate debt, unless you jump into junk territory. But that wouldn’t exactly protect against the downside, would it? If central banks cut interest rates further, there’s some potential price appreciation for fixed income but the room for it is disappearing. The fixed income option is uncertain and may do pretty badly if the stock market rises and presses bond prices down. Thus, let’s move on and look for non-standard fixed income products.

A few years ago, banks loved to sell structured notes. These were complex products that offered returns linked to certain outcomes related to the stock market, bonds, currencies, or commodities, but that were tweaked to offer downside protection in exchange for limits on the upside potential. Through the use of financial options, the bank could tweak the payoff of any asset. While appealing, these products usually carry counterparty risk; they’re opaque and difficult to understand; they’re not traded in an exchange; and they’re often tweaked to the banks’ needs and not to investor demand. These products were recently relaunched in a new, cleaner, simpler, and more liquid body. That of an ETF – a defined-outcome ETF.

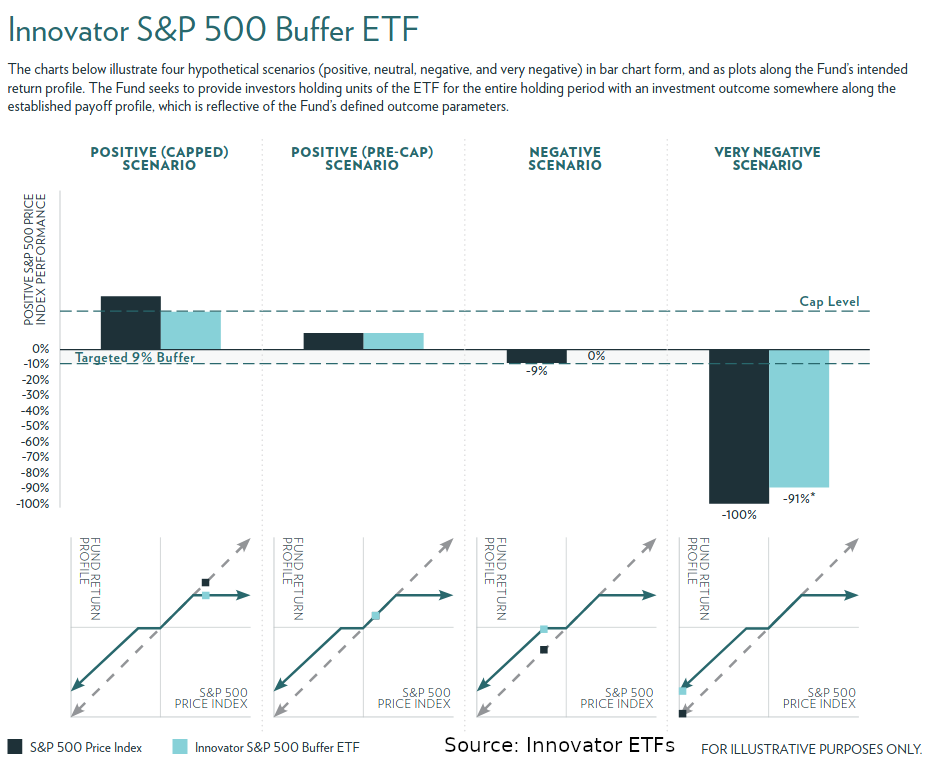

A defined outcome ETF offers protection against the downside in the form of a buffer. However, this comes at the cost of limiting the upside potential, in the form of a cap.

When investing in a defined outcome ETF, investors forego any gains an index may achieve above some pre-defined cap. If the fund is capped at 8% and the underlying index rises 12%, an investor loses the difference in the form of an opportunity cost. It’s not an accounting loss but just a foregoing of extra profits. Another loss is dividends. As these funds don’t track total return, an investor misses the dividends part. Thus, roughly speaking, if the dividend yield for the index is 2.5%, that comes also in the form of an opportunity cost. The higher management fees (when compared with broad market ETFs) comes also as another cost. So, when investing in defined income ETFs we need to live with limited upside, foregone dividend yield and higher fees.

A question that arises at this point is: why would an investor be willing to engage in the above? The answer is straightforward: because these funds offer downside protection in return. Let’s say a fund has a 9% buffer. It means that if the underlying index declines by up to 9%, an investor doesn’t lose any money. If the index declines more than 9%, an investor loses 9% less than the loss suffered in the index. Suppose the underlying index declines 20%. Your loss would be just 11%.

Innovator ETFs is a leading issuer in the defined outcome world. The company launches a defined outcome product every month with a new cap and buffer expiring in 12 months. The fund then resets, according to the new market levels at that point. First Trust also offers these kinds of fund, which are created in a similar fashion but are launched quarterly. The expense ratio for these funds varies between 0.79% and 0.85%, which is a bit high when compared with the cheap broad market ETFs, but relatively fair for the kind of fund built from more complex products.

The defined outcome ETFs provided by Innovator are typically made up of three main layers of options[i]. The first layer involves buying and selling four options, two calls and two puts. This strategy establishes a synthetic 1:1 position in the underlying index. The second layer involves buying one put option while selling another to establish what is called a put spread and that serves as the downside buffer layer. It could end here but the strategy would be expensive. To finance it a little bit, the third layer involves selling a call option. In the end an investor foregoes some upside potential above a certain level while gaining some protection for the downside.

Innovator offers three levels of buffers for most of its products: Buffer, Power Buffer and Ultra Buffer. Investors that are more risk-averse can opt for the Ultra Buffer while others may opt for the plain Buffer. The extra downside protection always comes with a lower cap level on potential gains.

Innovator S&P 500 Offer

Innovator has been creating new defined income ETFs every month, tracking the S&P 500, the Nasdaq 100, the Russell 2000, the 20+ Year Treasury Bond and even the MSCI EM and MSCI EAFE indexes. The general idea is to issue one product every calendar month. These products never expire but are reset every year. This allows investors to buy the product at the reset date and have a clear idea on how the cap and buffer are. Let’s take a look into three S&P 500 products:

S&P 500 Buffer ETF (BATS:BOCT)

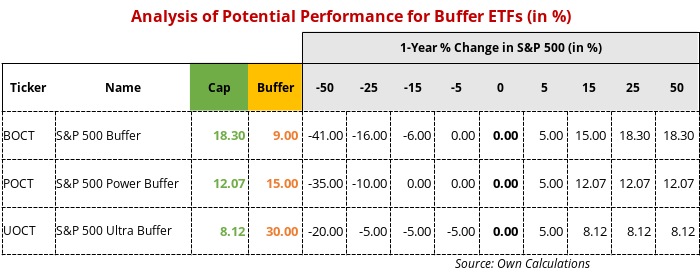

The S&P 500 Buffer ETF seeks to track the return of the S&P 500 Price Return Index, up to a predetermined cap, currently set at 18.30%, while buffering investors against the first 9% of losses over the outcome period, which starts at 1 October 2020 and ends at 30 September 2021. At the end of the period the cap and buffers are reset as Innovator will have to purchase a new lot of index options for another year. However, investors may stay invested in the product. An investor that believes the S&P 500 still has room to rise but who is concerned with potential losses may find this product compelling. If the S&P declines up to 9%, an investor loses nothing and if the S&P 500 declines more than that, an investor loses 9% less than the market. A buffer isn’t the same as a floor, which would put an effective cap on losses, but is cheaper to set. For an expected moderate to high gain in the broad market, this fund offers downside protection without much impact on the upside.

S&P 500 Power Buffer ETF (BATS:POCT)

Some investors are more averse than others or may just believe that the potential upside for the S&P 500 is much less than 18.30%. In this case they may exchange some upside potential for extra downside protection and then get a better buffer deal than offered by BOCT. The S&P 500 Power Buffer is similar to its Buffer version depicted above but caps the gains at 12.07% while increasing the downside buffer to 15%. If the market declines 20%, the loss for an investor in POCT would be 5% while it would amount to 11% in BOCT. The Power Buffer then better fits a more risk-averse investor or someone with a less optimistic view.

S&P 500 Ultra Buffer ETF (BATS:UOCT)

The third version is the Ultra Buffer, which caps gains at 8.12% but offers a buffer of 30%. If the S&P 500 declines between 5% and 35%, this product returns zero. If the S&P 500 moves between -5% and 8.12%, an investor gets the performance of the index. If the S&P 500 rises more than 8.12%, profit is capped to 8.12% and if it declines more than 35%, losses accumulate to 30% less than those suffered by the S&P 500.

The following table shows the outcome for an investor assuming different scenarios for each of these ETFs.

Some additional remarks

The defined outcome with which the above products are marketed usually refer to what happens if you buy the ETF at its launch or reset date and keep it until the next reset date. If you buy later, you could get a different return and different protection levels, based on how the market has moved. If the market has gone up, the fund will lose some of its return potential, while the buffer will appear greater. If the market has gone down, the fund will gain some return potential, but the buffer will appear lower.

The defined outcome products are more complex for an individual investor than other ETFs because of the mix of options these funds invest in. However, for someone wishing to preserve capital over a volatile period or someone with high risk-aversion, these products offer a very well-defined payoff. While there are many other options in the market, I believe this is a hybrid instrument that uses the real power of stock/index options. In a world of low-to-negative interest rates and a market that still retains upside potential but that’s marked with growing geopolitical and health risks, the defined outcome is a product to consider.

[i] An option is an agreement between a buyer and seller that gives its purchaser the right, but not the obligation, to buy or sell an underlying asset at a specified future date at an agreed upon price. A call option gives its purchaser the right to buy the underlying asset and its seller the obligation to sell it. Similarly, a put option gives its purchaser the right to sell the underlying asset and its seller the obligation to buy it. Innovator buys six options in total to build the defined outcome strategy.

Comments (0)