European Central Bank Fails on its Verbal Commitments

One of the most important monetary-policy tools is communication. Managing expectations is a skill that was once widely (and wisely) used by the European Central Bank (ECB) but it seems to be lacking now.

With inflation nearing two digits, the ECB’s only option is to hike its key interest rates. However, due to the asymmetry in fiscal conditions between countries, what it needs more than ever is strong communication skills.

Back in 2012, when Mario Draghi pledged to do “whatever it takes” to save the euro, he didn’t know he could. However, he went all-in because it was the only option he had. After that point, Draghi managed to get the approval needed for the ECB to step in and keep yield spreads tight across the eurozone. The low interest-rate environment that followed, helped the ECB keep these spreads below the radar.

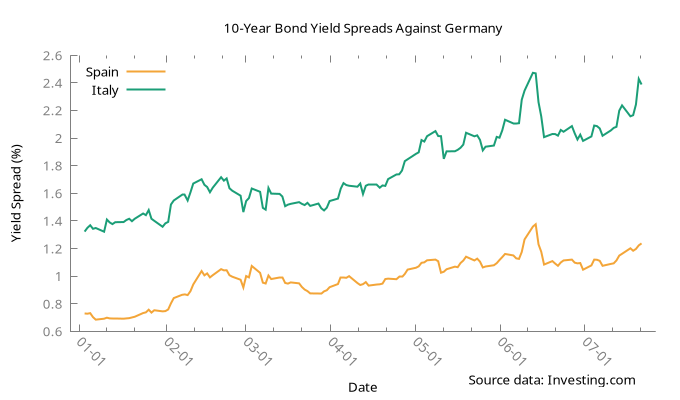

However, at a time when the central bank is hiking its interest rates, initiating a new rate cycle, the issue has been brought into the spotlight once again. ECB president, Christine Lagarde is caught between a rock and a hard place. On the one hand, she needs to hike interest rates very aggressively to fight the 8.6% inflation that threatens to disrupt the pursuit of the ECB’s goal of keeping inflation below 2%. On the other hand, after just one rate increase, bond spreads are already reflecting the past. Since the beginning of the year, the yield spreads on a 10-year Spanish bond and a 10-year Italian bond have risen from 0.73 and 1.32 to 1.24 and 2.39, respectively.

Unlike in the US, where there’s a single Treasury market with virtually no default risk, in the euro area there are 19 sovereign nations, and some of them carry higher risks than others. Such risk threatens the stability (if not the existence) of the euro and should be minimised through strong policy commitments.

To that end, the ECB has introduced the transmission protection instrument (TPI), under which, the eurosystem (the monetary authority of the eurozone – ie the ECB and central banks of member states) will be able to make secondary-market purchases of securities issued in jurisdictions that are experiencing a deterioration in financing conditions not warranted by country-specific fundamentals.

However, the ECB will take into consideration whether a sovereign nation pursues sound and sustainable fiscal and macroeconomic policies. The language used by the central bank to define and present the TPI is vague, conditional on fiscal matters and subjective. I would say it leaves a very large back door open for speculation, which is exactly what it aims to avoid.

As Draghi demonstrated during his mandate, verbal commitments are a powerful tool for policy makers. If the message is credible enough, you don’t really need to take action. The idea is to keep expectations tightly aligned with the central bank’s goals. However, Lagarde started the new rate cycle on the wrong foot, by raising interest rates well above investors’ expectations. At the same time, the ECB is not giving any clear clues about the expected path for monetary policy, leaving investors guessing. This contributes to a depreciating euro and increasing yield spreads.

For the euro to survive there must be no default risk. The ECB needs to pledge to keep yields narrow, adopting clear, transparent and credible debt-mutualisation policies. By setting a policy instrument conditional on fiscal rules, the ECB is admitting the possibility of default, thus contributing to the rise in yield spreads. At some point, the ECB will face a choice between allowing a default, which would probably mean the end for the euro, and buying sovereign debt, which would be more costly when fiscal deterioration had already occurred.

In my view, the ECB should not wait that long. Why not announce targets for yield spreads? Such a simple, rules-based policy would be much more credible than the TPI. Moreover, such a choice would require much less intervention and keep spreads tighter. But unfortunately, the EU continues to expect the ECB to use monetary-policy instruments that comply with the EU’s fiscal rules. For that reason, I believe the decline of the euro has further to go.

Comments (0)