Canada is heading for a hard landing

“Back in the old days, a collapse in mining meant that brokers, promoters, and mining entrepreneurs – not to mention the stockholders – had to move fast to raise cash. Their fancy cars went back to the dealers, and real estate agents put up “For Sale” signs in front of their handsome houses! No evidence of that now.”

― Business Insider, July 27, 2015

The world’s economy is walking through a dark tunnel where the light can be seen but never reached. While most economies are not in recession anymore, the near-term prospects are so uncertain that we now omit the words “prosperity”, “boom”, and “expansion” from our conversations, replacing them with the six-year-old “recovery”, which better describes an economy that seems to have improved, but where growth is moderate, financial markets are shaky, and employment creation is slow. After so many years of monetary intervention, central banks around the world are still undecided on the exact policy action they should adopt over the next few months. On the one hand, their economies are growing and creating jobs, but on the other hand, there’s a feeling that the disease is still active, and that major withdrawal symptoms could surface as soon as the treatment is stopped. As a consequence, central banks prefer to keep the status quo, as they fear being blamed for the next crisis. That explains why Carney and Yellen have been postponing the first rate hikes.

Past Action Leads to Future Consequences

For modern Keynesians, it is always easy to deal with recessions. A recession is the consequence of too much saving; monetary and fiscal policy should therefore try to discourage it. The central bank should expand its balance sheet, offering money at ultra low interest rates such that companies increase investment and households can keep consuming. Government should expand spending and cut taxes for companies in order for them to increase investment and hire more workers, and so on.

Lower interest rates encourage consumers to maintain their spending habits when disposable incomes shrink; pushes companies to invest in projects that would show negative NPVs under higher rates; and helps governments finance growing debts. When this is applied for a very limited period to smooth the business cycle, no major distortions are created. There’s nothing wrong with spending more in one month if one expects income to increase over the next month. But what about when spending is above income month after month?

For the last 20 years, the US Federal Reserve has been keeping interest rates below normal levels, which has allowed consumers to spend more than they otherwise would have, leading to higher demand, which in turn led to stronger investment, then to higher commodity prices, and finally higher house and asset prices. Why do you think the shale revolution began? Were interest rates higher there wouldn’t have been a shale revolution. Low rates allowed individuals and companies to invest in long-term projects that would never show a positive NPV under normal conditions. This means that the central bank has been contributing to oversupply, which could never have been absorbed by the country’s real wealth. The magic hand leads to an artificial sense of prosperity that leads to higher demand, higher supply and huge bubbles.

Canada Is a Victim

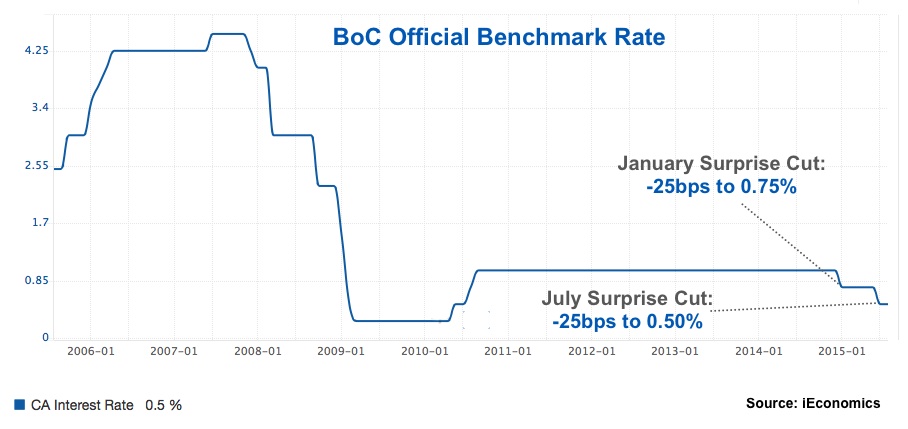

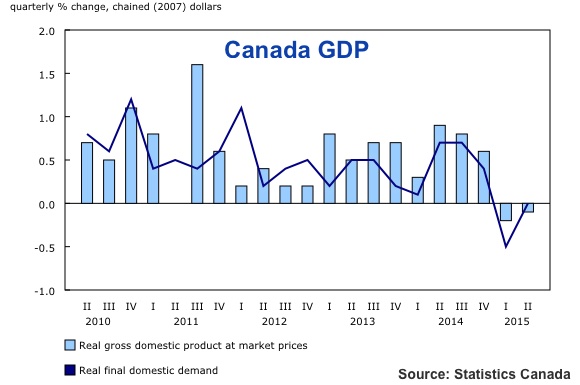

But the Keynesian formula doesn’t seem to work everywhere and at all times. Look at Canada. The country had a stunning performance during the financial crisis, escaping the harsh effects felt in the US and Europe. The main reason for this was the fact that banks were much better regulated in Canada and didn’t engage in the same kind of risky behaviour as others did. This spared Canada from a financial crisis and allowed the economy to absorb the negative international impact. In the opposite corner is Europe, which was severely damaged by the contagion from the US MBS crisis. But if Canada resisted in the 2007-2009 period, it seems it won’t do as well now. The economy shrank 0.5% in the 2nd quarter on top of a 0.8% loss in the 1st quarter, which means that Canada is in technical recession. Investment is shrinking very rapidly and the central bank has had to cut its output projections from a 1.9% rise this year to just 1.1%, and to surprise the market twice with interest rate cuts in a desperate attempt to spur growth.

Back in 2012 when Carney was still the governor of the BoC, both the central bank and the government blamed the Canadian corporations for lack of investment. The central bank had by then pushed interest rates down to nearly 1% from more than 4% and the government had been cutting corporate taxes. However corporations preferred to sit on “dead money” rather than invest. The Keynesian formula to spur investment and demand was not working, as companies didn’t react to the incentives given. A few years later, at a time when the US Federal Reserve is expected to reverse its monetary policy, commodity markets have crashed and the Canadian economy is dealing with a recession that could turn nasty. Canada is a great example of the collateral damage excessive monetary easing conducted by a leading economy can create around the world, something largely ignored by central bankers. It also counts as evidence that the main Keynesian assumptions may be wrong.

The Challenges

The Canadian economy is at a very important junction where it faces three main challenges: (1) business investment is declining and pressing GDP down; (2) a number of key economic sectors are facing declines in output; (3) household debt is increasing while disposable income is declining.

Lack of Business Investment

Low interest rates and corporate tax cuts didn’t prevent investment from declining. As Carney said in the past, companies are sitting on piles of “dead money” as they aren’t willing to invest more despite the incentives given. This situation has now persisted for years and is contributing to one of the most dangerous rotations ever felt in the Canadian economy. A few years ago the norm was for the Canadian household sector to run surpluses, which were then lent to corporations for them to invest in new projects, leading to gains in productivity and GDP growth. But the policy adopted by the government to boost corporate investment allied with decreasing interest rates has just contributed to an inversion of the situation, where companies run surpluses and households run debts. Keynesians were expecting companies to invest or to payout the extra profits to shareholders who would invest them. One way or another demand would be boosted. But that didn’t happen, as companies didn’t invest and the dividends received didn’t lead to an increase in consumption but rather to an increase house and equity prices. Real estate in Toronto and Vancouver is amongst the most expensive in the world. Even the BoC acknowledges that house prices may be showing an overvaluation of up to 30%. The propensity to consume among those receiving dividends from corporations is very low and thus it is not to rational to expect that if the corporate tax cuts fail to deliver investment that it would at least lead to higher consumption. It leads to bubbles and strong wealth redistribution issues instead.

Key Sectors Declining

The Canadian economy is too dependent on oil and mining exports. With the Fed expected to reverse policy, these sectors have turned very negative and are not expected to recover any time soon. A period of ultra loose monetary policy in the US led to the appreciation of the loonie, which damaged the country’s exports for too long and contributed to the lack of investment. Now that the Fed is reversing its policy and the loonie is depreciating, commodity prices are being decimated, erasing any positive effect. One point to notice here is the fact that the ultra-loose monetary policy conducted in the US for the last 20 years is responsible for the supply glut we now have in the oil markets, as the expensive shale oil production relied on artificially low interest rates on the one hand, and artificial high demand on the other. Now, there is excess production that will plague other oil producers for years and damage economies like Canada’s.

But it is not only about mining and oil. The decline is also felt in sectors like manufacturing, construction and wholesale trade. All these have been retreating over the last few quarters. At the other end of the scale lies the real estate sector, which has been pushing GDP higher. The high-flying real estate sector has been preventing the Canadian economy from entering a full-blown crisis, but it is also a sign that a bubble may be forming, as construction is retreating while the real estate sector is booming. Robert Shiller has already warned of a US-like housing bust taking place in Canada.

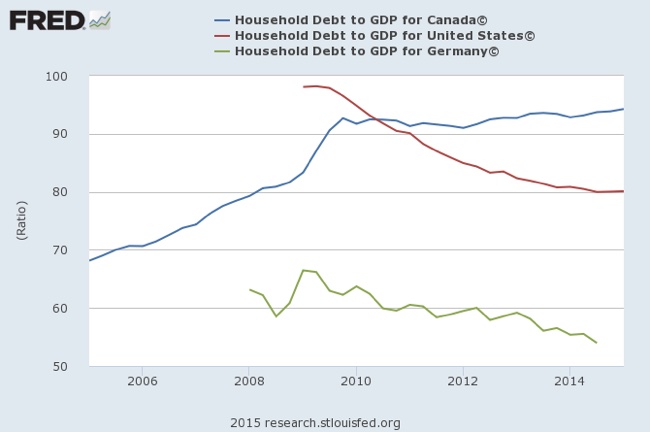

Household Debt

While household debt has been declining in the US and Europe as a result of a burst bubble, it has been increasing in Canada. This is because households have kept spending at a time when disposable income is decreasing.

When disposable income declines, the natural reaction from households is to cut spending. Of course, when all households cut spending we may end with a recession. But in a certain way, we should view such a reaction as not only natural but also efficient. Supply will then shrink and adapt to lower demand. But now think of a central bank cutting interest rates. Lower rates give the wrong incentive to households – to keep their consumption levels despite their disposable income being lower. As lower interest rates don’t help to increase real disposable income in any sustainable fashion, household debt will increase to unsustainable levels. The central bank buys time at the cost of creating a bubble.

When disposable income declines, there are only two efficient routes to take: (1) adopt policies that lead to an increase in disposable income such that households can keep consumption; or (2) do nothing, allowing households to adjust spending to their new lower levels of disposable income. Anything that messes with savings rates will just finance growth through debt and contribute to promote major supply gluts, such as those we now observe in the oil and mining markets. This is one point where Paul Krugman fails. He believes savings are the problem, when in fact the problem is disposable income. If the Canadians want to finance consumer spending, then it would be much better to increase taxes on corporations (which don’t invest as we have seen) and decrease them for households. To drive demand in a sustainable way, the Canadian government needs to forget about cutting corporate taxes and instead opt for decreasing them for households. This measure will allow Candian consumers to increase spending as a result of higher disposable income. The supply would then adjust to higher demand. In an economy battered by declining exports of oil and mining products, it may be worth boosting internal demand, although I don’t see that happening anytime soon…

The Future

With a general election scheduled for October 19, the future government will be confronted with a difficult task. The Canadian economy is a victim of ultra-loose Fed action and is heavily exposed to the movements it creates. A heavy exposure to oil and mining prices, rising household debt, and a bubble in real estate are strong reasons to believe the worst is not behind it. Central banks went too far in helping consumers to over-consume and producers to over-produce for too long. An economy grows from saving a little from the present and investing it to achieve higher levels of wealth in the future. No wealth can be achieved from spending more than what is produced. A reduction in disposable income is painful, but maintaining the same spending habits regardless is just insane and inefficient. Canada is preparing for a very harsh landing.

<insert tsx>

Comments (0)