BoE Concerned with China

The last time the BoE moved its key interest rate was in March 2009, when the financial crisis was at its peak and the British economy was thirsty for liquidity. Six and a half years later, the financial crisis is over but the BoE is still afraid of touching its near-zero rate. The last MPC minutes show an 8-1 vote in favour of a no change in the BoE main rate and expressed concerns about the latest developments in China, in particular regarding equity market volatility. Ian McCafferty was the only dissident voting in favour of an immediate rate hike, as he already did in August. The hot potato is now back in the hands of Janet Yellen and the US Federal Reserve.

Ian McCafferty believes that private domestic demand is and will remain strong, with consumer and business confidence at high levels. By raising rates a little now the central bank runs less risk of having to do it in a more aggressive manner in the future. The main idea is to start normalising policy as soon as possible to gain some cushion for future intervention if needed. At the same time, the sooner it starts, the flatter the rate increase would be, allowing for an easier accommodation of businesses and individuals. This is a line of thinking also advanced by some inside the Federal Reserve System but has been clearly outpaced by the fear of derailing economic growth. But in a world where the ZIRP (zero interest rate policy) dominates, it pays to be wrong with the crowd instead of being right alone, and no one wants to take the first-mover (dis)advantage.

The MPC minutes show the committee is concerned about China, fearing that any slowdown in the country may quickly spread to other economies. This has already happened in the equity markets, where the recent upturn in volatility experienced in China quickly spread all over the world, dragging global indices down significantly. As stated by the central bank:

“First, on 11 August the People’s Bank of China had lowered the central parity of the Renminbi exchange rate against the dollar by 1.9% compared with the previous day. It also announced a change to the mechanism for determining the central parity of the Renminbi, which led to a further depreciation.

Second, against the backdrop of the policy measures to support the stock market announced by the Chinese authorities in June and July, the Shanghai Stock Exchange Composite Index had dropped by 8% on 24 August, leading to substantial falls in both advanced economy and emerging market equity indices.

In total over the period since the MPC’s previous meeting, equity prices had fallen by 5-10% in the United Kingdom, United States and euro area.”

But while the international picture is considered, the BoE does not see China currently being a threat for the British economy, mainly because there is “domestic momentum underpinned by robust real income growth, supportive credit conditions, and elevated business and consumer confidence”. Mark Carney believes interest rates will start rising around “the turn of the year” and reassures that the path taken will be flatter than in previous cycles. The recognition that China currently doesn’t matter much was seen as a hawkish stance, helping the pound. But, the 11 times one can find the word “China” in the statement does not corroborate that view. Neither does the timing for the first rate hike.

The lack of action was not a surprise for markets, as investors have been backing the “no change” outcome and will continue to do so until 2016. With the job market losing some momentum, productivity increasing, and leading emerging markets cooling; there are a few additional reasons to believe that around “the turn of the year” may be no sooner than March. Energy prices are also important, as investors expect them to decline further. Just a few days ago Goldman Sachs projected oil prices to go as low as $20, a level unheard of in the current century. All these developments reduce price pressures and thus the urge to raise rates.

At the same time, the BoE may also be concerned with the action taken by neighbouring countries. At a time the ECB is planning to increase its asset purchase programme, it may be more difficult for the BoE to tighten monetary policy, as any attempt to reduce the money supply through interest rate hikes will be opposed by capital inflows from the Eurozone, exchanging the euro by the pound. The pound may appreciate quickly and produce negative effects in terms of output and inflation. These are the main concerns at the table right now.

What Does Theory Say

The central bank uses its key benchmark rate to help lead the economy towards full employment and inflation towards its long-term level of 2%. The central bank is mandated to deliver price stability. Whenever inflation is above its target, the central bank should increase its key rate. At the same time, the output gap is also an indicator of inflation pressures. When the gap narrows, the economy heads towards full employment and wages grow more rapidly, which presses inflation higher. Thus, the lower the gap, the higher the interest rate should be.

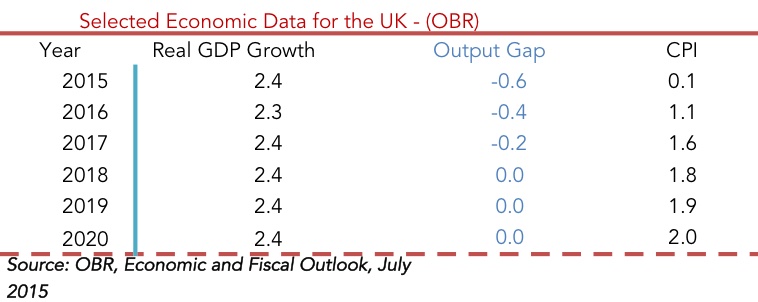

The current projections regarding real GDP growth and CPI from the Office for Budget responsibility (OBR) are as follows:

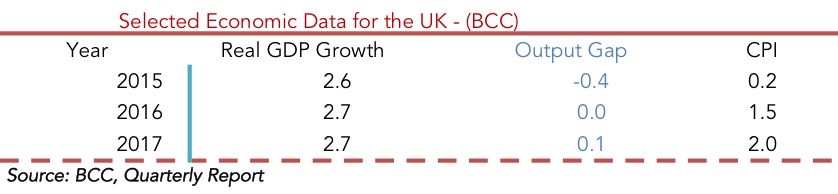

The same projections from the British Chambers of Commerce (BCC) are as follows:

In both cases the economy seems to be approaching full employment while inflation seems to be lagging, even though it is still expected to recover in 2016. These numbers remind us that while inflation is currently not a threat, economic growth will create price pressures as the output gap is quickly being eliminated. When this happens, interest rates should be adjusted higher. At the same time, both projections point to a rise in prices starting next year, which adds to the need for a rate hike.

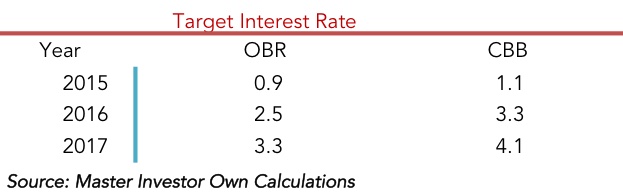

If we follow the Taylor Rule, considering equal weights for the output and inflation gaps and a long-term real interest rate of 2%, we find the following results for the advised interest rate:

By now, the BoE should be normalising its key rate and approaching the 1% level. Such a step would be particularly important because the growth and inflation projections for 2016 point to a much higher rate, between 2.5% and 3.3%. If the projections do materialise, the BoE may need to steepen its action in 2016, which will be much more risky in terms of economic growth. In delaying rate hikes, the BoE is contributing to bubbles in the economy, leading to bad investment decisions, and increasing the volatility of the boom-bust cycle. Delaying the first hike is creating uncertainty in the economy, as everybody is expecting it but yet it seems unlikely to ever happen. It would be much better to do what needs to be done sooner, even if that means having to deal with market declines. Keeping rates low at this point no longer contributes to higher investment levels, as everybody is in waiting mode. The sooner it happens the less uncertain the conditions will be for businesses.

Comments (0)