There’s more to come from the miners in 2017

The recovery in mining stocks took many by surprise in 2016. However, despite the renaissance, there is still a heavy weight of opinion against the mining sector. With this in mind, the contrarian in me is optimistic for continued outperformance in 2017.

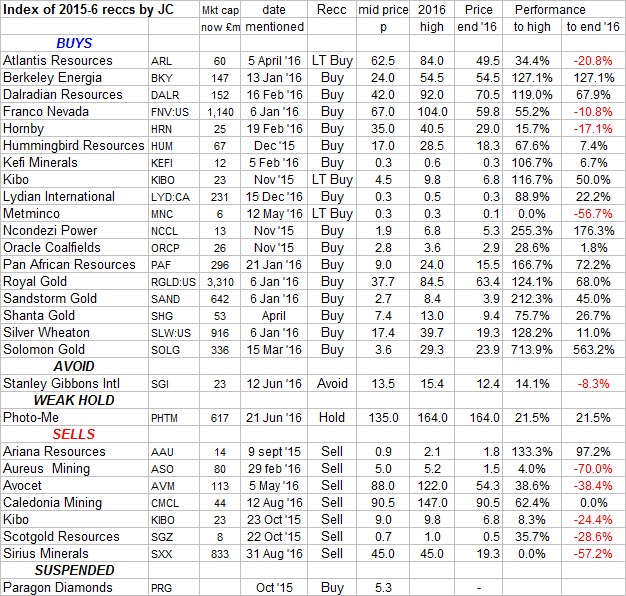

I know my writing here is too intermittent to update readers on investment timing (I warned as much in one of my blogs) so I missed suggesting taking profits when my various recommendations reached their peaks throughout 2016. Not that I’m claiming to call the tops. Except for the highest conviction stocks I hold, I usually take at least partial profits when I see a spike.

24 out of my 29 recommendations went the way I forecast; but one, Ariana Resources (LON:AAU) (on which I provide an update below) went spectacularly the other way; one, Metminco (LON:MNC) hasn’t delivered yet; and one, Caledonia Mining (LON:CMCL), initially went far beyond the price I thought irrational momentum would take it to – before crashing back down a bit later than I thought it would.

My worst bet, Paragon Diamonds (LON:PRG) was suspended – with last news in July when it was still hoping to secure finance for its Botswana diamond project. Since then: nothing.

But the table shows the successes well outweighing the few failures, with most picks, even if down from their peaks, still showing a healthy profit.

The Trump factor

Most of the fallers, of course have followed gold down from its mid 2016 peak, as the prospect of Trumpery loomed. But will Trumpery itself, and the excess US borrowing it might engender, spur gold back up again? Many expect that it will, in which case my goldies will offer another chance to reach and surpass their 2016 peaks.

Just as I started out in 2015 saying I would concentrate on mining as a sector to outperform other equities, I do so again in 2017, despite that some think the mining recovery has stalled for good. I believe, however, that most other equities have been propelled by QE, and temporarily by Brexit, too high for comfort, and that once Trumpery has run its course, gold in particular will recover.

…once Trumpery has run its course, gold in particular will recover.

But meanwhile, Trumpery has dented gold by 15% from its $1,350/oz mid-summer peaks. For gold producers the effect has been worse than 15%. With average cash production costs in the $750/oz region, their margin has reduced from $600/oz to $400/oz – a 33% hit. So it is not surprising that the New York gold bugs index has fallen by the same amount.

However, the 2016 flash of gold has put a more permanent glister on many goldies. It enabled the would-be producers, who a year ago were stalled by investor reluctance to fund their progress, to get at least some of their cash and over the hurdle to production – which will still be profitable, even if at present prices the investors won’t get their pay-back as quickly as they thought.

Signs of life

So we have more gold miners alive than we did a year ago – albeit with the likes of Kefi Minerals (LON:KEFI) still putting the last funding pieces together, and others, like Hummingbird (LON:HUM), getting their funds at worse rates than hoped.

Meanwhile, the funding hurdle (along with seemingly bad management) tripped up the likes of Avesoro Resources (LON:ASO) (previously known as Aureus Mining) which we recommended avoiding, and has seen its original shareholders diluted almost out of existence.

It is not just goldies who have benefited from the 2016 mining restart however. Copper and nickel projects have also sparked partially back into life, while zinc is a rare example of analysts’ price forecasts going their way on the back of a changed demand-supply imbalance that was relatively easy to foresee. With similar forecasts for copper by the end of the decade from those majors who should know, there is every reason for me to start looking at that sector – as I will in the near future.

But before I do, let me say that my analysis never relies on charts. In forty years I have only used them to judge how investors will react to a change in fundamentals – a method which can deliver the best results. So I go by whether I think the market has a correct opinion, which I do by checking as thoroughly as I can the ‘forecasts’ that analysts put up on behalf of their client companies.

As regards analysts’ forecasts I speak with many years of experience making them myself and from monitoring as far as I can those of my peers. So I know that very little truly ‘independent’ analysis, for AIM shares in particular (and even for many mid caps!), actually exists. All analyst reports from brokers are ‘paid-for’ in some form or another, so they have to be biased, even if ever so slightly, in the direction of economy with asking the awkward questions that should strike a good analyst.

…very little truly ‘independent’ analysis, for AIM shares in particular (and even for many mid caps!), actually exists.

And especially for mining stocks, where little consensus exists regarding correct valuation methods, I find that many analysts use whatever method will hype up the share price ‘targets’ that their clients want. These can range from ‘peer group’ comparisons with selective statistics, to spurious ‘NPV’ targets, and to the never-in-practice achieved ‘sums of parts’.

The spectacular but untypical example was, of course, Sirius Minerals (LON:SXX), where both the ‘house’ and a wannabe broker wanting part of the fund-raising used the extraordinary method of taking in forecast earnings 50 years ahead as a ‘valuation’ to justify their ‘target’ prices here and now. On the same basis Sainsbury’s would be valued in the market at well above prices that have never, ever, been seen in relation to earnings.

Fool’s gold?

The jewel in the crown is, of course, Solomon Gold (LON:SOLG), which is still my very strongest pick even after the massive gains to date. It remains in a class of its own, with exploration now almost fully funded for what looks likely to prove to be, after 2-3 years more drilling, a copper-gold resource many times larger than that discovered so far.

At present it is the growing size of an eventual tier-one mine that investors concentrate on, rather than the prices of either commodity, whose fluctuations meanwhile will only have a limited effect on the shares. For the record, at current prices, the ‘value’ of SOLG’s gold in the ground is about the same as its copper.

So how about Ariana Resources (LON:AAU)? As the only one of my opinions to have been seriously wrong it behoves me to take another look – at the company itself and at the latest research published note four months ago by its new broker, Panmure Gordon.

Ariana Resources 2015 and 2016

Just now, Ariana is in the news and its shares have spiked after taking over from the much larger (£1.7bn) Eldorado Gold (who retains a 2% production royalty) the remaining 50.5% of their joint Salinbas exploration venture in N East Turkey, 10 miles from where Mariana Resource’s joint venture with Lidya is finding the best copper-gold drill intersections in the world.

Only recently did its new broker put a $4m value on Ariana’s Salinbas stake, and before that other analysts were justifying the shares on expectations that Eldorado would pay £1m to buy it out. Now, however, Eldorado has elected not to add to the $8m it has spent since 2009 and obviously doesn’t think a stated $100m NPV8 for the 560,000 oz gold resource justifies spending the upfront $53.3m capex estimated for a mine.

Instead, it is Ariana who will have to spend to further prove up Salinbas. We haven’t been told how much, but it could be a lot (apart from the capex), which only adds to my original reservations about Ariana’s share price – that it has never taken account of the substantial amount by which the anticipated earnings from its first mine, Kiziltepe (now being built), will be diluted by the shares needing to be issued to pay for the further drilling necessary to keep it going after the present reserves run out in nine years from start in 2018.

Adding the commitment for Salinbas will only make things worse, and tip Ariana back towards the lower rating accorded to explorers, instead of the rating investors expected as a producer who might pay them a dividend now, instead of promising them jam later.

The bull point for Ariana has been that its first mine will subsidise its exploration and might still leave something over for dividends. But here Panmure’s latest note doesn’t reassure. Not because it doesn’t forecast a sharp increase in earnings from Kiziltepe – to a small cash inflow in 2017-18, and a $6m operating profit in 2018-19 (compared with a present $19m market cap) – but because it doesn’t assume any spending on Salinbas or to expand Kiziltepe, and therefore makes no allowance for dilution to come from extra share issues.

All of this puts the broker’s 2.7p share price ‘target’ (versus 1.8p now and based on that bane of my life – a NPV – which even then doesn’t allow for the ‘negative’ NPV of spending on exploration) into my ‘questionable’ basket.

Of course, the balance between spending and Kiziltepe cash earnings might be such that Ariana can still pay dividends from 2020 onwards. It would take too much work here for me to work it out but I think it unlikely.

But the fact that the new broker’s note hasn’t mentioned it illustrates my reservation about questions that are not asked. The company, of course, doesn’t want investors to ask them either. The management only have 4.6% of the shares, so would rather ride along for a bigger company that taking over Salinbas has given them, and the accompanying bigger perks, than for the profit on their shares that its outside investors would prefer.

That’s why I don’t think major institutions will be investing.

Comments (0)