The Japanese bubble reaches new technical extremes…

We suggested a potential short on the Japanese market nearly 1500 points lower just over a week ago (can you believe) and we are now in full blown parabolic mode.

The Japanese government and central bank seem to have finally found the magic ingredient for making money grown on trees…Mmmm… Intervention in financial markets has the potential to distort the economy and create inefficient allocations of resources, as well as asset bubbles and there sure as hell is one in place now.

Combine this with the already excessive liquidity sloshing around in the global financial system, and finally with the fact that Japan has been historically the ‘play-thing’ of global capital markets, then recent market moves begin to take on a precarious appearance to say the least… Forever being seen as a high-beta play, because of the often limited trading volume available in much of the Japanese equity market, individual stocks as well as the broader indices are capable of doing amazing things over short periods of time, as long as enough money is willing to chase the same stocks.

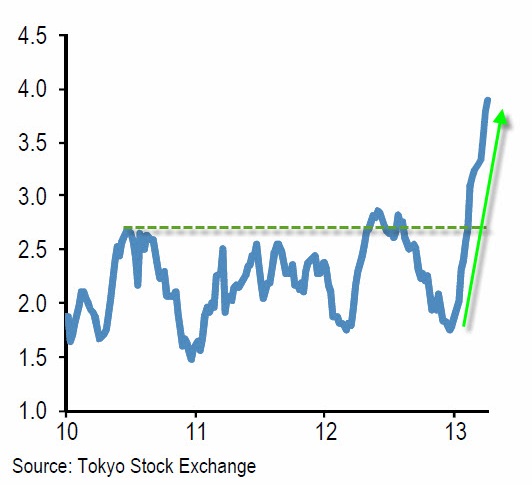

The chart below shows the net position (buys minus sells) of margin trading accounts (millions of shares) on the Tokyo Stock Exchange (TSE).

{kind=link}

This is basically a measure of how many shares have been bought by people who either can’t or won’t own shares outright, but that still want to be involved in the market. Needless to say, these are typically not your average conservative pension funds. Clearly, there is very significant interest in the stock market right now. Speculators are out in force, most likely trying to position themselves for expected higher corporate earnings as a results of the weaker Yen, as well as to try to front-run the BoJ’s prospective open market purchases of ETF’s and certain types of shares on the exchange.

Foreigners have always had a significant impact on the direction of the Japanese market, and this time is no different. The chart below shows foreign investors’ net buying of Japanese equities, along with japanese investors’ net selling.

Historically, the Japanese have been very happy to accommodate foreigners when the former wanted to increase their position in the Japanese equity market substantially. Again, this time is no different – or perhaps it is different. Perhaps they think they know something about the Japanese economy that the average foreign investor does not? Food for thought.

The somewhat speculative nature of this market move is also clear from the U.S. government oversight entity the Commodity Futures Trading Commission (CFTC), which published the following chart showing the net speculative positions in Nikkei 225 futures contracts measured in billions of dollars (NOTE THIS WAS FROM MID APRIL).

Speculative positions in the Nikkei 225 futures market are at their highest in more than 6 years. The eagerness to get involved is clearly huge, but for the investors who are late to the party, the bad news is that this level of speculative positions have historically not boded well for the short term outlook for the market.

Looking at what this type of phenomenon does to markets, we can take the first chart (net position of margin trading accounts) and extend it back to 1989 and Then overlay the broadest Japanese equity market, the Topix.

There is little doubt that these fund flows have historically had a huge impact on the market, but note how relatively small the rise in the Topix has been this time around compared with the current size of the net margin position. If the net margin position tops out here, possibly as a result of investors (particularly foreign investors) becoming disappointed with the impact of the flows, then the market could become very vulnerable to a large correction downwards. Of course, the impact of the inflows has been very significant in term of percentage returns for any investor who bought the market a year ago and which we advocated right at the ground floor level in November, but it is a given that the vast majority of investors did not get involved until fairly recently.

Whether this necessarily means the market is going to drop sharply in the short term is anyone’s guess, but it is worth keeping in mind that historically investors have not felt particularly wedded to owning Japanese equities. In fact, far from it. At the first sign of trouble, they often tend to find the nearest exit very quickly indeed.

As we can see in the chart below, the move in the last month has been unarguably parabolic with 13,14, 15 and now it looks like 16,000 being taken out in just 30 days – this is very reminiscent of the Nasdaq in 1999/2000 – we all recall how that ended…. The deviation from the 7 month moving average that we referrred to in our last piece is in unchartered territory, the weekly RSI the most overbought it’s been since 1988-89 and speculative positioning at extremes. We were early again, but doubt that the party goes much further…

Comments (0)