Does Reckitt Benckiser’s 30% price decline make it good value?

Does a lower share price and higher yield mean Reckitt Benckiser is good value again, or is it just an overpriced seller of disposable goods? John Kingham investigates.

| First seen in Master Investor Magazine

Never miss an issue of Master Investor Magazine – sign-up now for free! |

Reckitt Benckiser (LON:RB.) (which I’ll refer to as RB) is one of the world’s leading fast-moving consumer goods (FMCG) companies. In plain English that means it develops and sells familiar branded health and hygiene products like Dettol, Durex, Nurofen, Vanish and Cillit Bang. In recent years RB and similar companies like Unilever have become very popular with investors, largely because they offered a seemingly low risk way to invest in shares whilst still achieving attractive returns.

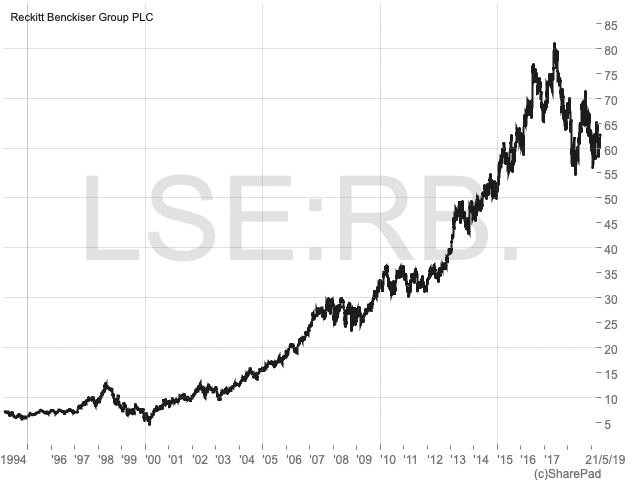

For a long time, RB lived up to that promise, with dividends increasing by more than 70% since the financial crisis and a share price which tripled between 2009 and 2017. More recently though, things have become less certain and RB’s share price has declined by almost a third since its 2017 high.

This share price decline has driven the company’s dividend yield up to 3%, which is below average but still much better than the sub-2% yield RB was offering a couple of years ago. So, does this lower share price and higher yield mean RB is good value again, or is it just an overpriced seller of disposable goods?

Generating consistent growth is not always easy

One of the reasons why investors love consumer goods companies is that they have a long history of steady growth and a plausible case for long-term future growth. As the world’s population has become larger and richer through the 20th and now the 21st century, more and more people want, and can afford to buy, branded consumer goods such as dishwasher tablets (and the dishwashers they go in), headache pills and detergent.

Companies like RB and Unilever have benefited from this tail wind for decades, making them a no-brainer option for many dividend growth investors. But investing and capitalism are not always that easy, and in recent years RB’s steady growth train has come off the rails.

It started in 2012, a few years after RB sailed through the financial crisis as if it wasn’t there. Revenues and earnings began to go sideways rather than upwards, and the dividend growth fell from a consistent 10% per year to low single digits and finally to zero in 2015. RB’s performance picked up again in 2016, but that was mostly due to Brexit and the related decline in the value of the pound (RB generates most of its revenues in other currencies but reports its results in GBP, so when the pound went down, RB’s results went up). If we ignore currency movements then Reckitt Benckiser had pretty much ground to a halt.

Shortly after these disappointing results, RB’s share price peaked in mid-2017 at 8,100p, giving the company a dividend yield of just 1.9%. Clearly there was a dislocation between the growth rate expected by investors (with a sub-2% yield I assume investors were looking for long-term dividend growth of at least 6% to 8% per year) and the almost non-existent growth the company was producing.

At this point there were two possible outcomes (or some combination thereof): Either RB would return to growth, or the share price would collapse when investors demanded a higher dividend yield to offset the lack of growth. What we actually got was a little bit of both.

RB loads up on debt to acquire growth

In the last couple of years RB’s revenues, earnings and dividends have all surged forwards once again. Was this the result of a massive increase in the number of people using Dettol, Durex and Nurofen? No, it was primarily down to one very large acquisition.

As a general rule, I prefer companies to generate most of their growth organically rather than by acquisition. There are lots of reasons why, but one of them is that acquisitions are the growth mechanism of choice for desperate companies whose core business has stalled or started to decline. Desperate buyers tend to overpay, and they often buy companies whose main business has only a fleeting resemblance to their existing core business. In the worst case, the acquirer borrows vast sums to buy a mediocre company operating in an unrelated sector, and investors are sold on the deal with promises of vast synergies, cost savings and cross-selling opportunities.

| First seen in Master Investor Magazine

Never miss an issue of Master Investor Magazine – sign-up now for free! |

Some of that applies to RB and some of it doesn’t. I think RB’s management were getting desperate as the company’s lack of growth in 2015 and 2016 threatened to undermine the CEO’s position. Unable to generate much organic growth, RB’s management decided to go out and buy growth instead. They did this by spending a whopping £12.3 billion buying Mead Johnson Nutrition, maker of the Enfamil infant formula and owner of world-leading child nutrition brands.

This acquisition was funded by debt rather than equity, and at first glance the economics make an awful lot of sense. If you can borrow say £100 million at 4% interest (costing you £4 million per year) to by a company generating profits of £10 million per year, you get an extra £6 million in profit per year essentially for free.

But there’s a snag, which is that corporate profits and cash flows are variable, while debt interest payments are fixed. If the acquired company has a bad year or two then its profits may fail to cover the debt interest payments. If that goes on for too long then you could be in serious trouble with the banks, and that’s never a good idea. So, while debt-funded acquisitions should lead to increased profits, they also lead to increased risk.

In RB’s case, it primarily funded the acquisition of Mead Johnson with approximately £16 billion of debt. That’s ten-times RB’s pre-acquisition net profits of around £1.6 billion, which is a bit like taking out a loan for ten-times your annual net income. It’s a big financial obligation and a big risk if your income falters.

What really matters though is the ratio of debt to post-acquisition profits. Mead Johnson was generating net profits of about £0.5 billion before the acquisition, so add that to RB’s £1.6 billion profits and we get a post-acquisition expected net profit figure of £2.1 billion and that’s exactly what the combined businesses generated in 2018.

However, £16 billion of debt is still almost eight-times £2.1 billion, and a debt to profit ratio of eight is, in my experience, a recipe for disaster. Thankfully RB’s management seemed to agree. Soon after the completion of the Mead Johnson acquisition, RB sold off its food business for £3.2 billion and the proceeds were quite sensibly used to reduce the company’s enormous debt pile.

In addition, the removal of the food business (including famous brands like French’s Mustard), continued a long process of restructuring which has significantly reshaped RB in recent years.

RB has changed significantly over the last decade

One of the nice things about consumer goods companies is that the best of them don’t really change much over the years. That’s why investors like the companies that sell Coca Cola, Gillette razors, Johnnie Walker whisky or Dettol. These products don’t change much, so they don’t require expensive R&D to improve them every year, and yet their sales continue to grow as more and more ‘middle class’ consumers around the world aspire to consume these branded products.

This slow pace of change does apply to many of RB’s core health and hygiene Powerbrands. However, the list of brands that make up that core, as well as the list of brands outside that core, has been through a significant amount of change in the last decade or so.

For example, RB spent around £16.5 billion acquiring the companies behind leading brands over the last ten years. During that time, it generated net profits of £18.7 billion, so the amount spent on acquisitions was almost equal to the amount earned in profit.

That’s a problem for several reasons: 1) Large acquisitions can be disruptive and distracting while systems, processes and cultures are integrated and aligned; 2) They are often misjudged, with hoped for synergies, cost savings and expansion opportunities failing to appear; 3) Large acquisitions make it difficult for investors to understand a company’s performance. That’s because the acquirer can end up as a confusing collection of recently acquired businesses, rather than a single entity with a long and coherent history.

On a more positive note, RB’s recent acquisitions seem to be closely related to its core health and hygiene business. For example, RB purchased Boots Healthcare International (maker of Strepsils, Clearasil and Sweetex) for £1.9 billion in 2006, and SSL (the company behind Durex) for £2.5 billion in 2010, and of course Mead Johnson (maker of Enfamil infant formula) for £12.3 billion in 2017.

| First seen in Master Investor Magazine

Never miss an issue of Master Investor Magazine – sign-up now for free! |

In addition to spending over £16.5 billion in the last ten years acquiring other brands, RB has been busy offloading ‘non-core’ brands, partly to fund acquisitions and partly to increase the company’s focus on its Health and Hygiene Home Powerbrands. Notable among the disposals were RB’s pharmaceutical business (reorganised as Indivior PLC and listed on the stock exchange in 2014 at around £2 billion) and its food business (sold for £3.2 billion in 2017).

For a company with a market cap of around £40 billion, adding businesses worth £16.5 billion and removing other businesses worth more than £5 billion is a significant amount of change.My point is that while consumer goods businesses are supposed to be stable and low risk in theory, in practice they can be just as full of change and uncertainty as any other company.

And the change and uncertainty aren’t over yet. The next phase of RB’s reorganisation is called RB 2.0 and it involves splitting the company into two largely separate and independent businesses; RB Health and RB Hygiene Home, in order to “reignite growth”. As with the acquisitions and disposals, splitting RB in two may be a good idea, but it does add yet more uncertainty and risk.Speaking of uncertainty and risk, that leads me onto the most important point, which is:

Is RB good value today?

So far, I’ve been somewhat negative about Reckitt Benckiser, partly to counter some of the relentless enthusiasm many investors have for fast moving consumer goods companies like RB and Unilever.

Yes, these companies have benefited from a growing global ‘middle class’ who want to buy their high margin and relatively defensive products such as headache pills and detergent. But no, they don’t have a Golden Ticket which allows them to be perpetual growth machines, churning out 10% growth year in year out from here to infinity.

They are real companies operating in the real world, with real competitors who can do them serious damage and real customers who can change their minds about which brands they like.

Capitalism is tough, and that is precisely why RB has had to work so hard over the last decade to reposition itself away from just home cleaning products and towards emerging markets, health and hygiene. And despite all that work, its growth rate still ground to a halt in 2015 and 2016.

In summary then, RB is a defensive business with a reasonable track record of success, but it’s undergoing a significant amount of restructuring to stay competitive. Over the last ten years its revenue and dividend growth rates have averaged close to 5% per year, although by 2016 growth has virtually stopped. The company has grown again in the last couple of years, but mostly because it’s leveraged up its balance sheet and acquired growth. How sustainable this new growth spurt will turn out to be is unknown.

As for the future, I don’t have a crystal ball, but RB’s own estimates for long-term annual revenue growth are in the 3% to 5% ballpark. Some profit margin expansion is always possible, so perhaps earnings and dividends could grow a little faster than 5% over the medium-term. However, I’d rather err on the side of caution and set my expected long-term dividend growth rate for RB at 5% per year.

With an expected dividend growth rate of 5% and a current dividend yield of 3% (at a share price of 5850p), RB has an expected total return (i.e. dividend yield plus dividend growth) of 8% per year.

That’s not bad, but it isn’t especially interesting either. The UK stock market has historically returned something in the region of 7% to 9% over the long-term, so an expected 8% return from RB is no better than the market average (the FTSE 100’s dividend yield is currently just north of 4%). To put it another way, at 5,850p RB is probably trading at something close to fair value, and as a value investor I’m only looking to invest in companies when they appear to be trading significantly below fair value.

My ‘good value’ price for Reckitt Benckiser

| First seen in Master Investor Magazine

Never miss an issue of Master Investor Magazine – sign-up now for free! |

I wouldn’t buy RB at 5,850p because I don’t find the combination of dividend yield and expected dividend growth is attractive enough. I also don’t like its £12 billion debt mountain and I would want to see that debt pile cut to £8 billion or less before I’d invest. But let’s ignore those debts for now and focus on price.

With an expected dividend growth rate of 5%, I would want to see that combined with a dividend yield of around 4% at the very least. With a 4% yield the stock would offer an expected annualised return close to my 10% target, and the shares could be set for a rebound if RB manages to exceed that 5% dividend growth rate.

For RB to have a 4% dividend yield, its share price would have to fall to about 4,200p at some point in the next year. That would be a drop of about 28% from today’s price, which some investors might think is impossible. I would disagree, and I’m sure that investors who bought RB at 8,000p in 2017 didn’t expect the shares to fall 30% over the following two years. But they did.

Comments (0)