The Dividend King: lunching with Job Curtis of City of London Investment Trust

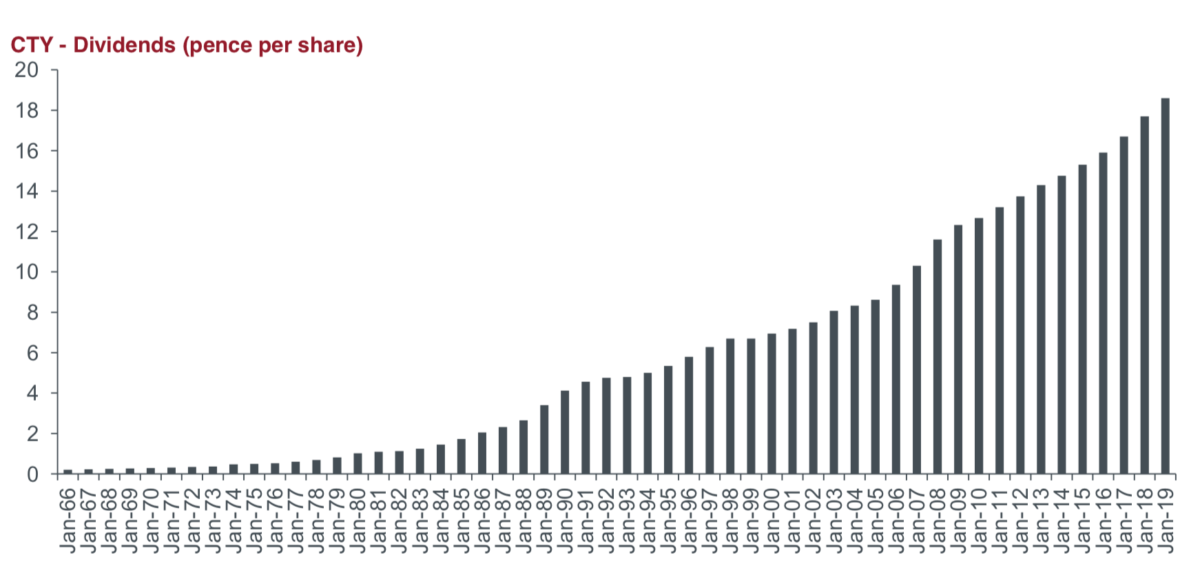

City of London Trust has raised its dividend for an astonishing 53 consecutive years. Last week, I had lunch with its manager, Job Curtis, to find out how.

In today’s world of rapid change and upheaval, it is unsurprising that many investors are searching for something that has stood the test of time. Investment trusts represent some of the oldest collective investment vehicles in the world, and many have a pedigree stretching back over a hundred years. One of them is City of London Investment Trust (LON:CTY), which was founded in 1891. With 53 consecutive years of dividend increases under its belt, City is one of the Association of Investment Companies’ (AIC) ‘Dividend Heroes’ and boasts the longest unbroken record of dividend increases of any investment trust. Last week, I was lucky enough to be invited to a press lunch to learn more.

Its mild-mannered manager, Job Curtis, is the archetypal safe pair of hands. The antithesis to the flashy fund manager, Curtis admits he is “conservative by nature” – a trait that is reflected in his investment style. There are no punchy outsized positions in City’s portfolio, which will no doubt come as a welcome relief to those investors caught out by the Woodford debacle. If Curtis possesses an ego, it is certainly not apparent. This is not a man to take undue risks with his investors’ money.

With net assets of around £1.6 billion, City is one of the largest UK equity income trusts, and in fact it has been growing rapidly of late. The Retail Distribution Review, which re-jigged the rules for how financial products are sold to retail investors, led to a surge in demand for investment trusts – and City has been taking full advantage of this. Over the past nine years it has issued no fewer than 170 million new shares at a premium to net asset value* (NAV) (note that issuing shares at a premium has a positive effect on returns for existing holders), thereby increasing its share capital by 82%. At the same time, this has helped to enable the board of directors to negotiate a reduction in the investment management fee it pays to Janus Henderson, to just 0.325% of net assets (it was in fact already one of the lowest in the sector). What’s more, the board expects ongoing charges “to fall further” during the financial year to 30thJune 2020.

Curtis is quick to point out the value to shareholders of having an independent board of directors fighting their corner. But this is just one of the benefits of the investment trust structure. Investment trusts are what is referred to as “closed-ended” investment vehicles. This means they have a fixed share capital structure, much like any other listed company. As such, their shares are bought and sold on the open market, which stands in contrast to “open-ended” funds, which see their investment capital rise and fall as investors buy or redeem units, respectively. One of the great advantages this conveys to managers of closed-ended funds is the fact that they don’t have to concern themselves with making sure there is enough liquidity in the fund to meet client redemptions. This means they can focus more of their attention on the fund’s investments, and they can avoid being forced to sell investments at inopportune times (i.e. when markets are falling).

Another advantage of the closed-ended structure is a flexible balance sheet. While open-ended funds have to pay out all the dividends they receive as income to shareholders, investment trusts can hold back up to 15% of income each year in what is known as a revenue reserve. The revenue reserve can then be drawn upon in the leaner years to augment the portfolio’s underlying income and grow or maintain the pay-out to shareholders. Curtis notes that he would not have been able to achieve the trust’s astonishing record if he had not had recourse to the revenue reserve – during a 28-year tenure he has drawn on the reserve on no fewer than seven occasions to keep the dividend growing.

In addition to the revenue reserve, investment trusts can also ‘gear up’ the balance sheet by taking on debt. This has the effect of accentuating performance, both to the upside and the downside. Used wisely, gearing can augment returns, but it can also exacerbate losses if a manager gets caught out with too much gearing in a downturn. As one might expect given the temperament of its manager, City’s gearing is relatively low at 7.9% (as at the end of June 2019), but its use during the course of the 2019 financial year serves as a good illustration of how, when used skilfully, gearing can augment returns. At the beginning of the financial year, gearing stood at 7.7% and was gradually increased to 11.9% as markets fell towards December – a classic example of a manager acting counter-cyclically – only to be reduced again to 7.9% by the year end as markets recovered.

As for the portfolio itself, the top ten is a rollcall of FTSE 100 defensive names such as spirits maker Diageo (LON:DGE), consumer goods giant Unilever (LON:ULVR) and pharmaceuticals firm GlaxoSmithKline (LON:GSK). While City is indeed a UK-focused equity income trust, it should be noted that all but one of the top 10 portfolio constituents are truly global businesses that generate considerable overseas earnings. As such, the trust is relatively well insulated against the gyrations stemming from Brexit.

That said, Curtis is pretty sanguine about the UK’s prospects post-Brexit, and he thinks the economy is in “pretty good shape”. As such, he isn’t afraid to take the odd contrarian bet with domestically-oriented stocks such as housebuilders, which he believes could be in for a “Brexit bounce” once the clouds of uncertainty are lifted. As for when that will happen, Curtis admits that’s anyone’s guess right now – and indeed there could be further downside for stock prices in the near term – but nevertheless, valuations among domestics appear “extremely depressed”, in Curtis’s view.

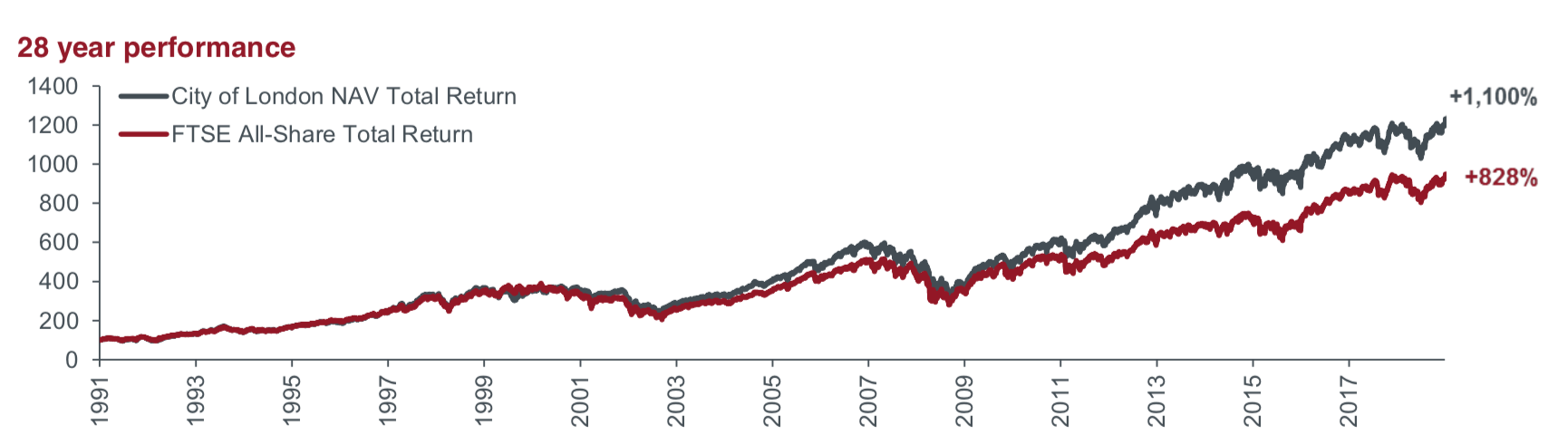

What I like about City is the fact it – like its manager – is understated. While some will shout from the rooftops about their achievements, City has been quietly getting on with providing investors steady returns for over a hundred years. Yes, there are funds and trusts out there with a better performance record, but for those investors who are looking for a relatively secure source of income from UK equities that rises steadily, you can’t go too far wrong with City of London, in my view.

* Investment trusts and other “closed-ended” funds can trade at a premium or discount to their net asset value (NAV).

Comments (0)