The dividends continue to flow at Diversified Energy Company

Diversified Energy (LON:DEC) continues to churn out generous quarterly dividends to investors through its unique business model, writes James Faulkner.

Readers may recall that I originally covered Diversified Energy (then known as Diversified Gas & Oil) back in June 2020 during the time of the slump in energy prices. I argued that the company was a special case despite its then double-digit yield, and that investors would continue to enjoy a very generous – and growing – income stream for the foreseeable future.

Indeed, that has proved to be the case, with the quarterly pay-out rising from 3.5 cents per share in September 2020 to 3.75 cents in December and being maintained at the current level of 4 cents per share since March. Investors buying in today will be eligible for the fourth quarter dividend of 4 cents per share and the first quarter dividend of the same, payable in June and September respectively. However, investors should bear in mind that the sterling value of these dividends can fluctuate given that they are declared and paid in US dollars.

Since my initial write-up last June, the shares have also put in a decent performance in terms of capital appreciation, rising from around 100p to the current price 119p at time of writing. Although this is less remarkable than some of the company’s peers, many of the latter were hit very hard by the slump in energy prices whereas DEC shares held up comparatively well. But with the dividend yield still over 9%, the shares are still attractive to investors looking for income.

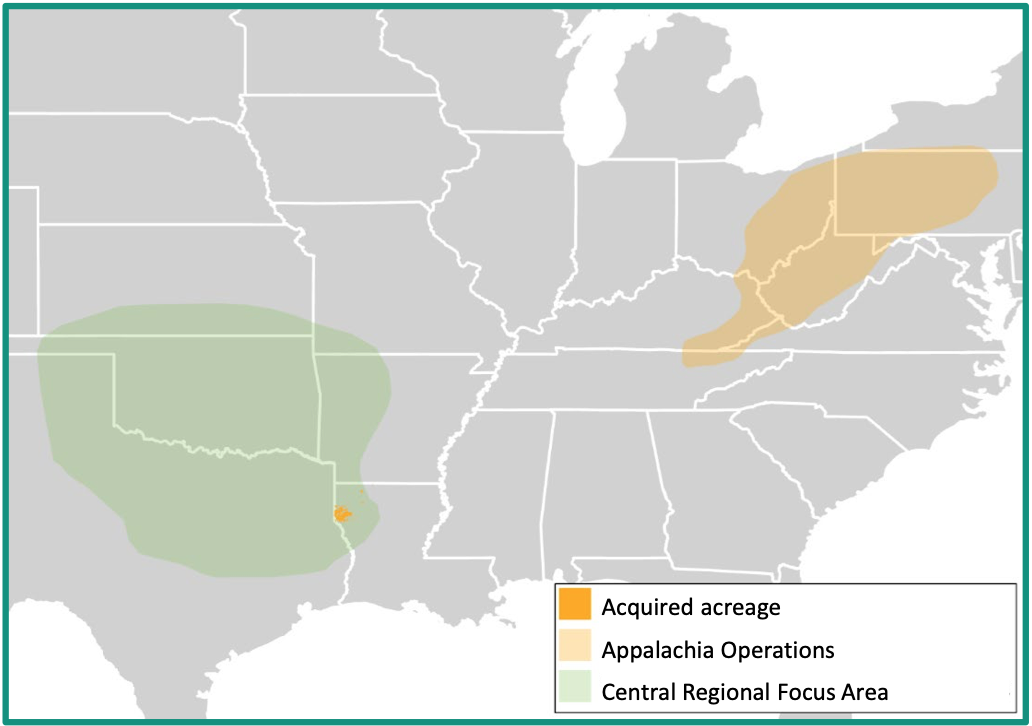

At this point, I should like to point readers towards my initial write-up on DEC, which outlines how their unique business model revolves around acquiring producing assets that are considered non-core to the vendor and maximising the efficiency of those assets in order to extract value for shareholders. The latest such acquisition came in April, when the firm agreed to acquire a portfolio of Cotton Valley upstream assets and related facilities from Indigo Minerals for US$135m.

The assets, which are located in a newly identified regional focus area (RFA) primarily situated in the state of Louisiana, include 815 wells and add 16,000 boepd (a 16% uplift) of daily production. The acquisition also adds 305Bcfe (50mmboe) of proved-developed-producing reserves (an 8% uplift). Furthermore, with similar characteristics to the firm’s existing Appalachia portfolio – i.e. long-life (50+ years), low-decline (6% terminal decline) production profiles – this will enable DEC to optimise and enhance the value of the assets through its proven Smarter Asset Management initiatives.

The purchase price gives a 2.9x multiple on around $40m of adjusted EBITDA, which looks good value on the basis that the deal is 13% accretive to the firm’s 2020 adjusted EBITDA while DEC equity trades on an EV/EBITDA ratio of around 7. Moreover, PV10 (present value using a 10% discount rate) of around $175m suggests a 23% discount for the purchase price. And bear in mind that is before DEC works its magic in terms of efficiencies etc.

The firm’s proforma net debt to EBITDA stays around the same at 2.3x after the deal with available liquidity of around $200 million, and CEO Rusty Hutson hinted at further deals to come in the update in April:

“Our new regional focus area covers a multi-state area in a similar size footprint to Appalachia, and meets our expansion criteria in terms of asset quality, infrastructure, market dynamics, opportunity set and supportive regulatory environment. This first strategic acquisition outside of Appalachia also reflects our continued commitment to a consistent asset profile and valuation while affording us expanded value-accretive roll-up opportunities in this new region that will enable us to quickly build scale and drive efficiencies. Our financial and operational strengths continue to uniquely position Diversified to capitalise on current market conditions as the PDP buyer of choice.”

With DEC sticking to its knitting, and with natural gas set to remain a feature of the energy mix for decades to come, I think holders can feel confident that the dividends will continue to flow.

You again fail to mention the witholding tax , so UK shareholders loose 30% of the dividend to this tax. Brokers, when challenged are claiming that having a W8-BEN in place makes no difference with this share.

So hold it in a tax paying account and take the credit in your tax return

I completed a W8-BEN a few months ago and the last div was paid minus 15% tax. Your broker is not giving you the correct info.

I would suggest you give some thought to finding a competent firm to handle your holdings.

Mine is ii.

werrento I’d really like an answer on that one!

Steve L.

From discussion elsewhere, there does seem to be a bit of a pattern whereby “independent” brokers honour the W8-BEN system, whereas bank-linked brokers may not.

Thus Lloyds/Halifax/IWeb point blank refuse to pay out the proper amount (ie the dividend less the 15% tax). They claim the difference is being witheld from them by their custodian – Crest. They say that “the company is subject to US tax as that is where they declare it, and so it is out of our control what happens with the tax as all dividends are taxed before we receive them.

Crest does not have a service in place where by we can apply W8-BEN to stocks held in Crest where this company is held. This again is beyond our control and the custodian we use will not be changing, as that is a business decision,and has been for many years”.

As it stands if you continue to hold the stock with us then you will continue to be taxed at 30%.

So Steve L.’s recommendation is most relevant.

Caveat emptor.