The defensive REIT trading on a 17% discount and yielding 6.7%

The Real Estate Investment Trust (REIT) sector has experienced a dramatic sell-off during the last month or so due to the sharp increase in gilt yields. Some of these write downs are undoubtedly justified, especially in the case of properties that are exposed to more economically sensitive areas, but there has also been an element of indiscriminate selling.

According to the broker Winterflood, one trust that has been oversold is the Impact Healthcare REIT (LON: IHR), which has just released its quarterly update to the end of September. The care home provider reported a modest NAV total return of 1.8% during the period, thereby demonstrating its resilience to the various headwinds facing the economy.

Despite the market uncertainty, the independent valuer found no reason to justify a shift in investment yields for healthcare real estate in the quarter. This enabled the NAV of the portfolio to increase by 0.4% as the impact of inflation-linked rent increases and capital expenditure on the properties outweighed the slight deterioration in the performance of the homes.

Resilient portfolio

At 30 September, the portfolio comprised 136 properties, with 134 of them let to 13 tenants on fixed term leases of 20 to 35 years with a weighted average unexpired lease term of 19.7 years. The total valuation was £543m and after the end of the period a non-core home was sold for 40% above its book value.

All of the portfolio’s properties are let with inflation-linked leases that are typically subject to a four percent cap and two percent collar. There were 12 rent reviews completed in the period at an average uplift of 4.69% per annum, which was in line with the rental increase cap, with the rent roll rising from £42m to £43.2m after taking into account the three new acquisitions.

Underlying occupancy rose to 87.3% with the fund receiving all of the rent due for the period. At the end of September the trust had cash of £23.2m on the balance sheet with £131m of its £206m debt facility drawn down, the majority of which is hedged at a fixed interest rate of around three percent.

Defensive trust that has been unjustifiably sold down

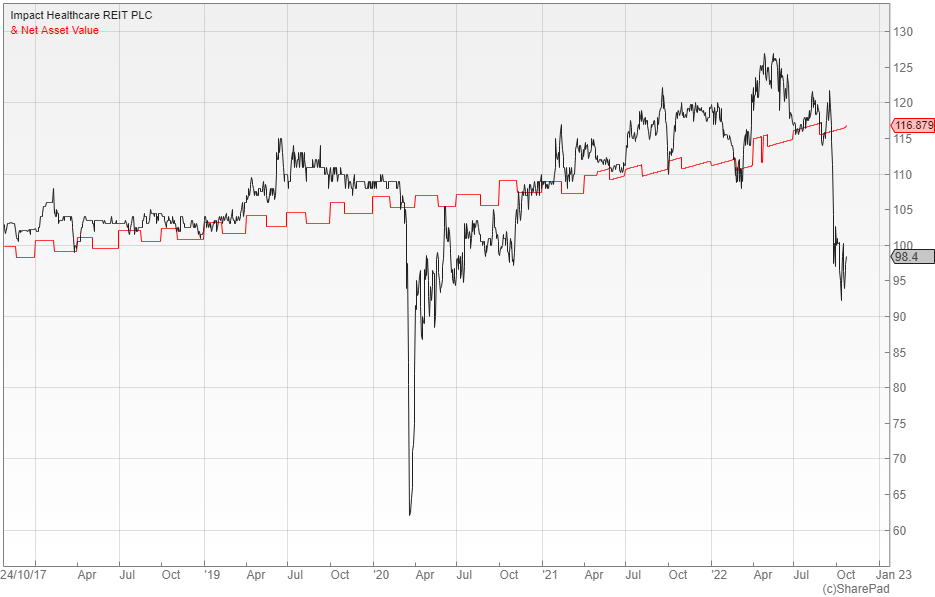

A quarterly dividend of 1.635 pence per share was declared during the quarter that was fully covered by earnings and in line with the annual dividend target of 6.54p for the financial year ending 31 December 2022. With the shares trading at around 98p this gives them a prospective inflation-linked yield of 6.7%.

Winterflood says that the underlying rental income and asset values should be much less exposed to an economic downturn than traditional commercial property and the inflation-linked revenue will help to offset the negative impact of rising interest rates on the fund’s borrowing costs. They also point out that the balance sheet remains strong, with a reasonably low loan-to-value ratio of 21.4% and 77% of the drawn debt hedged.

The trust has historically tended to trade at a small premium to NAV, but the recent sell-off has opened up a discount of 17% that is unprecedented other than during the initial Covid-induced crash. Winterflood describe this as an attractive entry point, with the prospective yield standing at 6.7%, although they acknowledge that there may be further near term volatility.

Comments (0)