Centrica is priced for energy armageddon

Most of the time, when you’re looking for very high yield stocks you end up finding companies which are either small, young or highly cyclical. Sometimes though, you’ll find the exact opposite, and that’s what we have today with Centrica.

It’s a large, mature business operating in what should be a very defensive sector, and yet it has a dividend yield of more than 8%. At first glance this seems odd. Why would a company with such an entrenched market position, operating in such a defensive market have such a high yield? Let’s find out.

In the beginning energy companies were privatised, and it was good

After the energy sector was privatised in the 1980s and ‘90s, energy utilities were about the most boring and defensive stocks you could imagine. For the most part they sucked fossil fuels out of the ground, processed them and sent the end result out to homes and businesses through the national grid. For many years it was a very attractive business to be in. Competition was sparse, demand was almost entirely unaffected by the economic cycle and customers had little or no interest in hunting around for the best deal. And governments largely kept out of the way because they wanted to show that the re-privatisation of the industry had been a success.

Today this situation has changed dramatically, largely because of the financial crisis and its secondary effects. Most important among those effects are: a) the tough economic environment of the last decade; b) an increased distrust of capitalism; and c) government’s desire to appear tough on “fat cat” and “rip off” businesses. I’ll take each of those in turn:

Nobody really wants to buy gas or electricity

When times are tough, the cost of gas and electricity matters. After all, when was the last time you heard somebody say, “I’m going to run up a massive electricity bill this week because I’m worth it!”? My guess is never. That’s because nobody actually wantsto buy what Centrica is selling. They haveto buy it, and there’s a big difference. In that sense gas and electricity are like car insurance. But it’s worse than that. At least with car insurance you can reduce your car insurance costs by buying a smaller car, or not having a car at all. With gas and electricity there’s pretty much no way to avoid them unless you want to live like a caveman.

When the good times are rolling, most people don’t care about their utility bills. But when most of the country is “just about managing”, the cost of those unavoidable bills really sticks in the throat.

Evil capitalists are out to rip you off

I think capitalism is awesome. Yes, it isn’t perfect; far from it. But its ability to efficiently allocate human and physical capital towards activities that society values is astonishing. But, as I said, it’s far from perfect. In the run up to the financial crisis, regulators thought that financial markets worked best when left alone, and the result was a large number of “bankers” pocketing vast amounts of money at the expense of the rest of us. Quite rightly, ordinary people were not overly impressed with this, especially when it created an illusory boom and an all too real bust. But quite wrongly, that distrust of “bankers” has grown into a general distrust of big business and even capitalism itself.

Unfortunately for Centrica and the other big energy utilities, they sit right in the crosshairs of this distrust, largely because they’re big businesses, they’re well-known and nobody wants to buy their product, but everybody has to.

“Rip-off” energy companies are an easy target for politicians

Given this backdrop of falling real wages, dead-end zero-hour contract jobs and a growing distrust of big business, it’s no surprise that political parties want to show they’re standing up for the common folk by squaring up to and facing down those evil big businesses. To a large extent that’s going on with the government versus Facebook, Amazon, Google and Starbucks (to name a few).

As for Centrica and the other big energy utilities, both of the UK’s major political parties have come up with market interventions which are largely responsible for the high yields these companies offer (for example, SSE also has a yield of more than 7%). So what are those market interventions?

The Conservative plan revolves around a price cap on the standard variable tariff which would, in my opinion, be a bad idea. Hopefully this price cap idea is more of a big stick which politicians can use to look tough and cajole energy companies into somehow lowering their prices. However, it could be implemented and if it is, the impact on Centrica and the other big energy utilities would probably be negative.

Compared to the Conservatives, Labour’s market intervention is on to an entirely different scale. Labour’s plan is to nationalise the sector, either just the transmission and distribution network (think National Grid) or perhaps all the big energy suppliers as well, including Centrica. I think a programme of mass nationalisations is both a) likely to be inefficient and lead to worse service and significant subsidies from the taxpayer and b) a very real risk to shareholders.

A misguided regulatory sledgehammer to crack a relatively small nut

Both the price cap and nationalisation ideas are attempts to fix a broken market. And if the energy market was seriously broken, then perhaps a reasonable argument could be made for such extreme measures. But I just don’t see any evidence of widespread market abuse.

If, for example, Centrica was systematically ripping off the majority or even a substantial minority of its customers, then it would show up in its accounts. Centrica would be consistently earning excess profits beyond those possible in a reasonably competitive market.

My preferred measure of profitability is return on capital employed (ROCE), which shows how much profit a company makes from its fixed capital assets (e.g. oil and gas infrastructure) and its working capital (e.g. cash in the bank or oil and gas in storage). On average, companies on my stock screen (which covers about 200 dividend-paying FTSE All-Share companies) produce post-tax returns on capital employed of about 10% per year. Weak and uncompetitive companies produce returns on capital employed as low as 5% (if they produce any returns at all) and companies with strong competitive advantages can produce consistent returns on capital employed of 20% or more. So where does Centrica fit into this spectrum of profitability and competitiveness?

Over the last decade, Centrica’s post-tax ROCE has averaged 11%. That does not look like a company ripping off the majority (or even a significant minority) of its customers to me. It looks like the returns of a reasonably competitive company in a reasonably competitive industry. If Centrica is ripping people off left right and centre, where exactly is it hiding the profits?

For more investment ideas, subscribe for FREE to never miss an issue of the Master Investor Magazine.

I’m not saying Centrica or the other big energy utilities don’t overcharge some vulnerable customers who are not capable, for whatever reason, of constantly switching to the cheapest supplier. And I’m not saying the energy market couldn’t be improved. What I am saying is that there’s no obvious evidence I can see that a large percentage of Centrica’s customers are being ripped off.

That’s why I think the solutions offered by both political parties are way over the top, especially the idea that nationalisation will somehow lead to better outcomes. Remember British Leyland cars? Ah, those were the days (of rust and constant break-downs). As far as I can see, these proposed interventions are largely driven by vote chasing rather than a real concern for the effectiveness of the energy market and outcomes for those who are “just about managing”.

And they won’t work anyway. Not in any meaningful way. That’s because energy utility profit margins are about 5%. So even if the energy utilities made zero profit, your energy bill would only fall by about 5%. Big deal. A better solution would be to remove green and social “taxes” from our energy bills and move them onto our income tax bills. That would reduce energy bills by about 10% and make those green and social costs progressive rather than regressive.

In summary then, Centrica faces potentially serious and largely unquantifiable regulatory risks. That will put many investors off completely. However, I’ll assume you’re not one of them, so let’s carry on and look at what Centrica is doing in this tough and uncertain environment.

Centrica’s response is to refocus on its customer-facing business

Following weak results in the years leading up to 2015, Centrica carried out a major business review and concluded that it needed to focus much more on efficiency and its customer-facing businesses, and less on fossil fuel exploration and production.

Its multi-year plan is currently about half-way through the first stage, which runs to 2020. On the efficiency side, some 6,000 jobs are expected to go by 2020. Along with many other changes, this will hopefully lower costs by around £750 million each year. The company’s focus is also materially moving towards its customer-facing business, with some £900 million being realised from exploration and production disposals, which is helping to finance an investment of up to £1.5 billion into customer-facing activities.

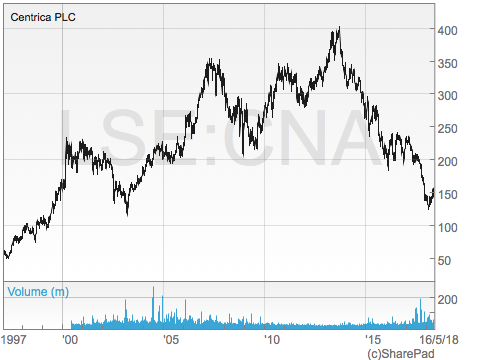

How all this will affect the company’s results is yet to be seen, but Centrica had to do something. Over the last decade the company has pretty much gone nowhere, with earnings and dividends more or less unchanged since the financial crisis. Once inflation is factored into the equation, Centrica has actually shrunk quite a bit over the last decade.

Historically, another potential sticking point has been Centrica’s relatively high capital intensity. In other words, extracting, refining, storing and burning fossil fuels takes a lot of capital assets such as oil rigs and refineries. If Centrica wanted to expand its exploration and production business, it would have to invest huge sums up-front in these assets before it could generate a penny of revenue or profit. This makes growth much more expensive and much more difficult, although one upside is that high capital intensity puts off would-be competitors from entering the market.

This is now changing as Centrica moves away from that sort of capital intensive exploration and production activity. In the last few years its capex ratio (the ratio of capital expenses to net profits) has fallen from a relatively high 100% or more (i.e. the company spent more on capital assets than it made in profits) to a much more typical 60% or so. That’s because customer-facing activities like supplying energy and fixing boilers is much less capital intensive than extracting oil or gas.

So capital intensity is no longer such a problem, but its debts and pension obligations are. This does seem to be a recurring theme at the moment, largely because extraordinarily low interest rates have seduced companies into taking on more debt whilst also inflating the size of their pension obligations. In Centrica’s case, it has debts of more than £6 billion, which are more than four-times its recent average profits. That’s high, but it doesn’t break one of my investment rules:

INVESTMENT RULE: Don’t invest in a defensive company if its debts are more than five-times its recent average profits

As well as fairly high debts, the company has considerable retirement obligations as well. Currently these run to just over £9 billion, or 6.6-times recent average profits. The pension scheme also has a deficit of almost £1 billion which is effectively a debt to the pension scheme which must be repaid. With borrowings of £6 billion and a pension deficit of £1 billion, Centrica does indeed start to look uncomfortably indebted, with a debt ratio of five once the pension deficit is included, and that’s right on the limit of what I would call an acceptable level of debt. But it gets worse. I have another investment rule relating to pension obligations:

INVESTMENT RULE: Don’t invest in a company if its combined debt and pension obligations exceed ten-times its recent average profits.

With borrowings of £6 billion (excluding the £1 billion pension deficit) and total pension obligations of £9 billion, Centrica’s combined debt and pension obligations of £15 billion are about 11-times its recent average profits of £1.4 billion. That takes it above and beyond the level I’m comfortable with.

The verdict

Overall then I would describe Centrica as a mature, well-known business operating in what should be a very defensive sector. Unfortunately, mature also means low growth in this instance. Add to that low growth the external risks of populist regulatory changes and the internal risks of large financial obligations and it’s easy to see why the company has a dividend yield over 8%. Because of these various problems, I would not buy Centrica today. I think there are other stocks which offer a better risk-adjusted reward, although I must admit I do find that 8% yield enticing.

Somewhat contradictorily, I actually own shares in Centrica. I’ve owned them since 2012, which means the investment is about 50% underwater. Some investors would say I should sell the company if I’m not willing to buy more shares today, but I disagree. Yes, the investment has not gone well, at least so far. And yes, I would not buy shares in Centrica because of the regulatory risks and its large financial obligations. However, that doesn’t mean I have to sell. The future is a very uncertain place and nobody knows what it will bring, especially where investments are concerned.

Perhaps there will be no nationalisation programme and perhaps the price cap will either never happen or will be watered down and temporary. Perhaps Centrica can turn things around and return to modest growth by concentrating on customer-facing activities. If the dividend is maintained for long enough then investors are likely to become less pessimistic.If that happens, the dividend yield is likely to return to a more normal 4% or 5%, which would mean a significant increase in today’s share price. Obviously, I’m not saying that will happen, but it could. And since I’m here already and Centrica is about 1% of my portfolio, I might as well wait to see what happens.

Very comprehensive report , but no mention of centrica being a takeover target I think after July when the cap if a cap is decided upon you may see a bid and I think that may come from shell

Share buy-backs and shares given to Directors as bonus has also taken their toll on Cetrica’s share price. Its Board is not shareholder friendly, neither is Ofgen. Like the writer, John Kingham, I am underwater, have been for years which has prevented my selling of my shares and will certainly not be buying any more.

I can’t see a snowball’s chance that Shell will pony up £8.5bn++ to buy Centrica. As to continuing to hold, most brokers expect this dividend to be cut from 12p to more like 9p. Just sell.

What are your thoughts on National Grid?

As the share price crashes 15% overnight on 16 / 17th of May, my previous pessimistic note is entirely justified. Could Centrica be another Carillion Management collapse for similar reasons I wonder. There is talk of a profit warning…..

In my opinion, the prospects for the company’s near term profits, and therefore the share price over the next 6 months all hinge on the outcome of the price cap. The cap will almost certainly happen by the end of 2018 although the bill still has to go through Parliament before the summer for that to happen. Having said that, it should be a formality as who is going to vote against it? It is a no brainer vote winner for politicians for reasons discussed above. The more critical point then becomes how draconian the price cap is. Critically also the cap needs to be consistently applied across all energy suppliers. Finally, the cap needs to be set at a level that allows an efficient operator to be able to finance its activities – which we all know Centrica is not there yet. In my view the market is erring on the side of caution here and expecting a bad outcome. However if the cap is set at too tough a level or is applied inconsistently across energy suppliers then it will an easy challenge at a judicial review which is where it will end up. That will push back the implemetation of the cap well into 2019 and likely get a more foavourable result. Even if the cap is set at what I believe is the expected “£100 off” level being discussed by the industry, then it doesn’t affect all suppliers equally. I run a comparison website http://www.TheEnergyShop.com and have a detailed insight into the releative pricing of products across the majority of suppliers. British Gas (Centrica) will do relatively better, as its Standard Variable Tariff (SVT) is already cheaper than the majority the other Big 6 providers. BUT, and this is important, a tough cap like this will start to take down some of the smaller inefficient energy suppliers whose SVTs are already more expensive than those of Centrica. It also puts a questionmark over the current operating model of most new suppliers – buy customers on loss leading tariffs then stuff then onto expensive SVTs once the contract term is up. If you can’t stuff the customer anymore then the whole loss leading thing starts to look a bit shaky. The cap will change the competitive dynamic in the market. Some smaller suppliers will go bust, price competition will ease and incumbents will start to see less competitive pressure. I bought into Centrica at 125p earlier this year and topped up at 136p following the prelim results. In my opinion the market is pricing in a bad outcome for a price cap without thinking through the offsetting consequences. I could of course be wrong – we will know by the end of the year.

Hi William,

Are you sure you are talking about the same company here. Centrica fell 2.7% on 16 May becasue Morgan Stanley cut their price target on the stock. It did not fall 15%. Also Centrica is nothing like Carrilion. The supply business is low margin but pretty much all the costs are variable. Once it loses a customer it loses pretty much all the costs of provisioning that customer. So all it loses is the gross margin per customer. Carillion went down becasue of fixed price contacts and cost overruns. Centrica has certain fixed price deals with custoners but these are hedged. With its variable rate customers the costs and revenues are all matched and variable. Totally different operating model.