There’s smoke on the horizon

The latest news about property-development company, China Evergrande Group (HKG:3333) seems to have caught investors off guard across the globe and hit equities heavily. The company will likely default on its debt obligations and its 2022 bonds are now selling at 29c to the dollar and yielding more than 500%. The S&P 500 was pushed back 1.70% on Monday and European markets declined even more.

The People’s Bank of China can do whatever it wants to ‘clean the sheets’ of state-owned banks carrying Evergrande’s debts, without allowing any ripple effects into the financial system. Regarding the property sector, things may be a little nastier. If other property companies run into trouble, this may have repercussions in the Chinese economy, denting growth, because the sector contributes a large part of GDP. And if Chinese growth declines, so will global growth. For now, the matter is worrying but contained. But this should be taken as a global warning on property prices and the construction sector. These companies clearly run into more debt than they can handle during troubled times and what goes up must go down.

Where’s inflation?

Speaking of price increases, consumer prices are on the rise. The OECD has just revised higher its inflation predictions for G20 countries. US and UK inflation were revised from 2.9% and 1.3% to 3.6% and 2.3% for this year, respectively. Inflation predictions for France and Germany were also revised higher, as the OECD believes that the fast economic recovery from the pandemic will lead to a temporary rise in prices. From the perspective of a central bank this should be good news. After more than a decade with near-zero interest rates and massive asset- purchase programmes, they could finally reach their inflation targets. However, in my view, the rise of consumer prices is more the result of supply disruptions created by the pandemic than a monetary-policy effect.

While prices are rising, they aren’t exactly flying high. Richard Werner’s quantity theory helps understand why. The money created by central banks is not being used to purchase GDP items but instead to purchase stocks and cryptocurrency. According to Refinitiv data, global ETFs received an inflow of $640bn in the first half of this year − more than double the inflow in the same period last year. More worrying is the data from the Bank of America, reporting that money inflow to stocks between November 2020 and April 2021 hit $576bn, which compares with $452bn between 2008-2020. More money entered the stock market in just five months than over a period of 12 years. Maybe this helps clarify why prices are not exploding this year, despite the massive amount of money thrown into the economy. However, stock prices are rising faster than the corresponding profits, and the two metrics will have to catch up at some point. This is the main reason why I’m worried about investing in stocks. Borrowing against portfolios is now declining a bit since July but has already hit record levels this year and is still elevated.

Unshining gold

BlackRock is cutting gold holdings to near zero. The company says it: “… primarily thinks of gold as a hedge against equity risk, and that works when you’ve got an environment with real rates that are flat and declining”. While I hardly see gold as a hedge against equity risk, I understand that BlackRock is foreseeing an end to the current monetary-policy stance and predicting an interest-rate rise. Both the Fed and the European Central Bank are giving clues that they will start hiking their rates sooner rather than later. If that’s the case, gold appears less attractive because it doesn’t pay interest, unlike bonds. However, long-term bonds are also not attractive because of interest-rate risk increasing with duration.

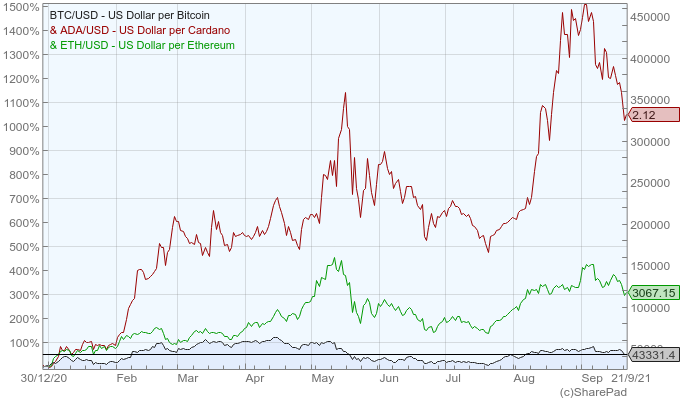

Bumpy crypto

In the crypto complex, the bumpy ride continues with many tokens frequently showing two-digit daily percent changes. For example, Bitcoin saw its price move more than 10% in 10 sessions this year and Miota in 46 sessions. Unlike the US dollar, which acts as a safe haven, crypto tokens are the first to be dumped during troubled times.

Apart from the high risk incurred in alt coins, there’s an additional growing risk, related to the safest’ part of the crypto market. It seems that Tether, a so-called stablecoin, which is pegged to the dollar, may be less stable than advertised. The company behind the coin, Tether Holdings Ltd disclosed last month that about half of its assets were held in commercial paper or certificates of deposit. Without more details given, there’s a real suspicion that the company is heavily exposed to Chinese commercial paper. While Tether doesn’t hold any of Evergrande’s securities, an Evergrande collapse may trigger further collapses, which could impact on some of the commercial paper held by Tether. This is a ‘stone in the shoe’ for crypto investors one not to ignore.

One way or another, there’s smoke on the horizon. And where there’s smoke …

Comments (0)