The Swedish residential property time bomb

As seen in this month’s Master Investor Magazine.

Property prices have been on the uptack during recent years and have accelerated over the last few in particular. An apartment in the most expensive area of London averages an astounding £11,600 per square metre while the average for the whole London region is still a respectable £4,425. But London is not an isolated case. In the centre of Stockholm an apartment costs on average around £6,250 per square metre, which is at par with prices in Wandsworth, London. The Swedish property market has been on a bull run since the mid 1990s. Fuelled by low interest rates, loose credit conditions, and several supply limitations, the Swedish property market has reached bubble dimensions, and is now waiting to capitulate and drive the rest of the economy towards recession. As buyers and sellers are happy to see their equity rising overnight, policymakers prefer to indulge an unsustainable situation rather than doing something that could disrupt sentiment. But inaction comes at the cost of bigger problems in the future, as everything that goes higher on credit must eventually come back to earth with a crash.

While Swedish property prices seem unshakable, prices have collapsed in many other countries, in particular in the US where a recession was ignited from this market. The 2007-2009 financial crisis, which is still not completely behind us, is a huge piece of evidence that house prices cannot rise forever. Fuelled by cheap credit, demand for houses was stunningly higher than supply for years, leveraging the economy and exposing it to increased downside risks. But a time comes when the market capitulates. A key question that arises is: what contributed to this excess demand? The answer can also help explain what is happening in Sweden.

Central banks miss the big picture

Milton Friedman was always a strong advocate of keeping a tight control of the money supply because he believed that any increase in the rate of growth of the stock of money above the increase in productivity would just lead to an acceleration in inflation. But central banks dismiss this reasoning because they have been able to increase the stock of money, at a time when productivity gains are sluggish, without generating any inflation. They don’t perceive any harm stemming from this policy stance, which aims at creating excess liquidity for years. But they’re wrong about it. According to the Quantity Theory of Credit, developed by Richard Werner, there are two possible outcomes resulting from an expansion of the money supply: (1) consumption credit grows and, with it, demand for goods and services, which creates consumer inflation; (2) financial credit grows, and then the same pool of financial assets is bid up by a greater amount of money, which creates asset inflation that is not captured by CPI measures. In this latter case, there is unproductive credit creation and an asset bubble forms because demand rises while total wealth remains constant.

With the help of the Quantity Theory of Credit, we can better understand why central banks avoided inflation and why central banks created banking crises and property bubbles. During the 1990s, low interest rates helped banks expand broad credit in excess of nominal GDP. Most credit was used to finance the purchase of financial assets and property, leading to a massive and continuous rise in asset prices. Because central banks were targeting CPI indices, they missed this collateral effect. But, unfortunately, such a collateral effect is at the root of the last financial crisis that hit the global economy and will again be present over the next. With central banks reacting to the latest crisis by increasing the pace of money creation, it seems they still fail to understand they are planting the seeds of another financial crisis.

The Swedish case

A particularly concerning case is the residential property market in Sweden. Unlike what happened in Denmark and in Spain where the property market crashed during the European sovereign debt crisis, in Sweden nothing seems to disrupt the interminable ascent of house prices. But what happened in the US, Denmark and Spain just reminds us that the market cannot grow forever. The faster the market grows in excess of GDP, the ever more leverage is attached to it, and the worse the collapse will be. The housing market cannot grow faster than overall wealth forever.

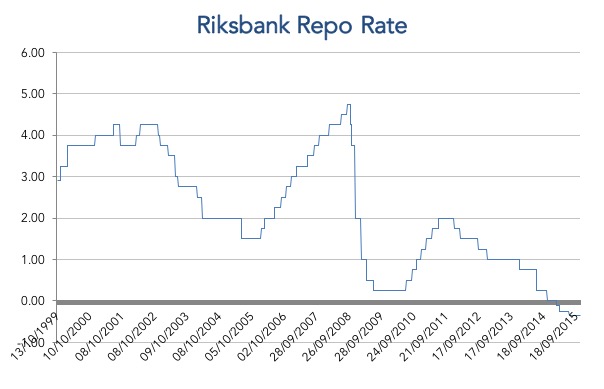

The Riksbank is currently following the ECB’s excessive easing policies, as otherwise the krona would start appreciating against the euro, undermining Swedish external trade. In 2010, and after cutting its key rate to 0.25pc, the Riksbank started hiking it towards the 2.00pc level; but at the end of 2011 it had to revert policy. Currently the Riksbank keeps its repo rate at the -0.35pc level and its deposit rate at -0.75pc. While a central bank would always argue that the interest rate is a general tool that should not be used to prick bubbles (if a central bank ever recognises one), the truth is that it has been creating a few as a collateral effect of its policy.

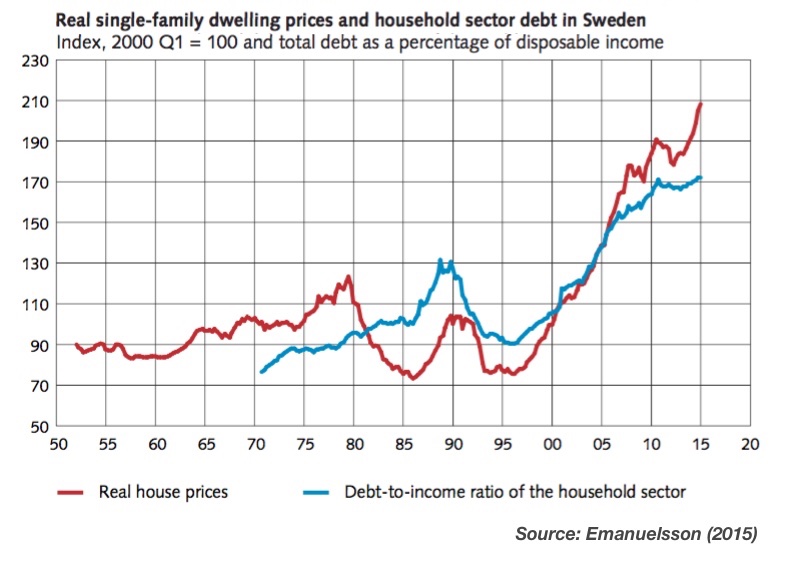

When house prices rise too much and for too long, new home buyers are attracted, as they fail to foresee the risks of a collapse in their equity. Banks, by their turn, are also usually enthusiastic about the extra income they can generate by lending more. When interest rates remain at very low levels for a long time, the central bank gives out the wrong signal to the economy and decisions are taken based on the prospects of that rate remaining at such low levels for an indefinite period. Such policy has been helping to drive real house prices higher and, in turn, generate an unsurmountable expansion of household debt. In Sweden, household debt-to-income grew from around 90% in 1995 to 175% in 2015. House prices grew almost 175% in the same period. While the price rise certainly contributes to household wealth, the overall debt assumed to purchase houses is growing faster than income. Household leverage is growing too fast, exposing the economy to a downturn in economic conditions. If a recession occurs (which it will, sooner or later), bad loans will pile up and banks may need to be bailed out. Household wealth, which is ever more dependent on those skyrocketing house prices, would by then crash.

Demand gets a boost…

Over the last few years, Sweden and other Nordic countries have been attracting large inflows of money. While none of these countries are genuine safe havens, they were seen as much safer than other European destinies when the sovereign crisis emerged. By then Swedish government bonds were seen as a safe investment, which helped keep interest rates lower than they should have been, and for longer. With the European economy severely wounded in general, the excess liquidity in Sweden contributed to a rise in demand for financial assets and property.

But the Swedish housing bubble is not just being driven by central banks. Rather, there are several other features also contributing to it. While credit has been widely and cheaply available, banks have magnified this effect with the use of interest-only loans. This kind of loan is a great emergency tool to absorb the negative effects stemming from a recession, as it can help households retain their assets during adverse situations (and this way also help to avoid a banking crisis). But banks have been assigning these kinds of loans when the economy is under extremely favourable conditions, thus extending leverage to the limit and then reducing the degrees of freedom in the system. In an economy where households have the opportunity to purchase a house when its price is the highest and when mortgage costs are the lowest, and through paying interest alone, I wonder what could happen if just one of these features deteriorates a little. The Economist reports that 40% of loans are currently not being repaid at all, as households are just paying interest. These data are alarming.

If asked about this, the Riksbank (as well as many other central banks) would claim that any potential bubble should not be dealt with by the use of interest rates. They would refer to macroprudential regulation as the adequate way of dealing with collateral effects. But the Swedish government has so far failed in approving regulation capable of curbing any rise in demand. As long as sentiment is high and there are solvent buyers, banks continue to lend money, no matter what the government does. Tight capital requirements on mortgages, caps on borrowing by individuals, and other restrictions aimed at limiting the purchase of property have been imposed without any significant success. Banks and borrowers always find a way, even if that means getting part of their loans at higher rates than before. After all, banks borrow money at negative rates from the central bank so they have a clear incentive to be creative in finding ways to bend regulations, and households have a track record of ever increasing house prices so they have a clear incentive to purchase. Of course, new laws could be approved to block demand, but any less moderate measures reducing credit in a significant way would also lead to a sudden crash in house prices – a result no one is willing to contemplate, because of the potential consequences for the overall economy.

…and supply is limited

A mix of low interest rates and favourable conditions is boosting demand for residential property in Sweden, which is pressing prices to appreciate uninterruptedly and at a very fast pace. But this is only half of the story. There is a whole set of issues on the supply side also contributing to the observed path of price increases. Prices wouldn’t have risen as fast if supply were not as tight as it has been. A study by Robert Emanuelsson from the Financial Stability Department of the Riksbank evaluates the Swedish residential housing market in detail and shortlists the factors contributing to a shortage of residential housing as follows: (1) high land prices and construction costs; (2) demanding processes for land and planning; (3) municipalities’ planning monopoly; (4) lack of competition in the civil engineering and construction industries; (5) regulation of the rental market; and (6) strict legislation on quality of housing.

The Swedish residential market suffers from quite a few market failures (which bestow pricing power to land owners and construction companies), and has been negatively impacted by approved legislation. This mix imparts rigidity on the supply side and helps explain why in a 20-year interval supply has not expanded to absorb the excess demand. There is an overall sense of shortage but supply doesn’t move accordingly.

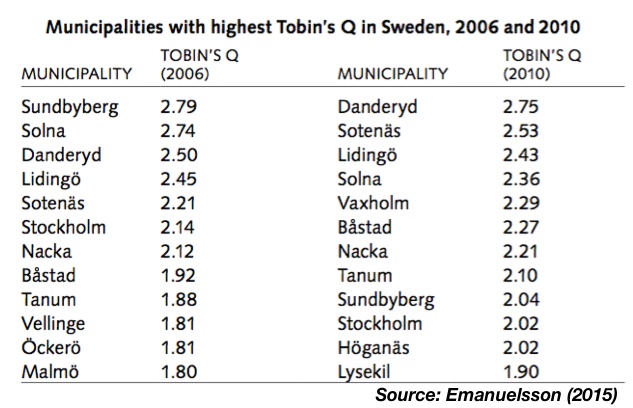

To evaluate how profitable it is for a supplier to build a house, the Tobin’s Q ratio developed by Tobin (1969) is of good use. While first developed for use in capital markets, the ratio is flexible enough to be applied in many sectors and industries. The idea is very simple: if the cost to build a house is lower than its market price, then it is profitable to build. In a free market, houses would be provided until the market price is equal to the cost of producing them. The Tobin’s ratio is then expressed as the ratio of market price of an existing home to the total production cost of a new, similar home. In a competitive market this ratio should tend to gravitate towards one. Emanuelsson shows that this ratio is near two in many municipalities in Sweden, which means that home builders are able to double their investments. In Stockholm the ratio was 2.14 in 2006 and still 2.02 in 2010. In a competitive market such a situation could not last because other suppliers would enter the market and provide additional housing, causing a decline in house prices. Equilibrium would be reached only when the ratio decreased to near one.

When the Tobin’s Q ratio persists at such high levels, it is clear that some monopoly power and limitations exist within the sector. In fact, as pointed out in the report, there are two sources for this. First of all, municipalities have control over land and retain their pricing power by keeping the supply of land for construction tight. With a growing population, particularly in big cities, house prices can only rise. There are even reports of people buying houses without ever visiting the house. Second, there are several barriers to entry in the construction market and the existing companies act within an oligopoly framework, retaining pricing power by providing fewer houses than the market would be willing to absorb.

A few final words

When considering the country as a whole, there is no shortage of residential housing in Sweden, but the process of urbanisation has created severe imbalances across municipalities. While people migrated to the big cities on a large scale, the existing market failures prevented supply from adjusting, creating a large shortage of housing in the big cities. Instead of helping to reduce the pressure created in the market, policymakers just made it worse, by boosting demand through ultra loose monetary policy and ill-designed fiscal incentives. The resulting outcome has been a massive price rise, economic inefficiency, and extreme vulnerability to deteriorating economic conditions. In a country where 40% of home loans are not being paid down, any sudden change in economic conditions can only lead to a crash and a severe crisis.

Comments (0)