Passive strategies for exploiting a rise in IPOs

The second quarter is expected to experience a huge increase in initial public offerings (IPOs), reports Filipe R Costa.

While the global economy fluctuates and there is still considerable uncertainty surrounding the Covid-19 pandemic, investors need to look for alternatives to a plain ‘vanilla’ investment in stocks and bonds. With so much money sitting on the sidelines, central banks pushing markets and chief executives seeking a piece of glory, initial public offerings (IPOs) may offer a good opportunity for investors in the second half of the year.

We’re only halfway through the year and we have had enough of it already. At the time of writing, the Covid-19 pandemic has hit 8.6 million people and taken the life of almost half a million. In the US alone, there are 2.3 million cases on record and the numbers are still growing quickly in some states. The US economy contracted by 5% during the first quarter and is expected to contract by 40% during the second quarter. Unemployment quickly rose from a record low at 3.5% to 14.7% − a level not seen since 1939. President Trump is desperate to recover his lead in time for the US election, but negative events are coming thick and fast. In Europe things aren’t much better, as output levels are depressed. However, the latest data published across the globe show signs of economic improvement, which is keeping markets afloat. But the choices investors need to make are still difficult. On the one hand, markets are rising. On the other hand, there seems to be a disconnection between markets and reality. For this reason, it is not time to go all-in but rather to carefully choose some niche investments. The market for IPOs may offer some good opportunities.

Investors are looking ahead

IPOs have gained steam since the beginning of the pandemic. The market is expected to grow in the second half of the year, as companies that postponed or cancelled their initial offerings are reassessing their prospects, as the equity market stabilises. In March, the VIX hit a level above 80 while the S&P 500 entered bear territory, when it was declining more than 30%, at one point. But, in the meantime, economic conditions improved, as the number of new Covid-19 cases decelerated, allowing for a reopening of economies. The S&P 500 managed to erase a large part of its losses, now just down near 4% for the year, while the VIX trades at 35, way down from a peak above 80.

Apart from a depressed stock market, there are other challenges for those trying to undertake a public offering. Chief executives need to present their companies to investors, a task usually accomplished through roadshows. But that’s not possible during a pandemic. However, they found alternative ways of presenting their companies through virtual roadshows, ie meeting with investors via teleconference from home. That would have been unthinkable just a few months ago, but at a time when everyone was setting up a home office, it became standard practice.

With the pandemic easing, a few companies have already tried their luck and gone public. Examples include the used-vehicle dealer Vroom (NASDAQ:VRM), the online insurance provider SelectQuote (NYSE:SLQT), the sales-software data provider ZoomInfo (NASDAQ:ZI) and the record label Warner Music Group (NASDAQ:WMG). Others like AirBnb, Palantir, Lemonade and DoubleDown Interactive may be preparing their debut for the second half of the year. The pandemic had an impact on all sectors, but it accelerated the existing process where customers are buying online rather than from high-street companies. The emerging public companies are more receptive to the adoption of technology in delivering products and services like e-commerce, online learning, streaming, delivery and telehealth. They have their chance now.

With central banks injecting trillions into the market by purchasing government and corporate bonds around the globe, while keeping interest rates near zero, conditions are favourable for equities. But there’s a lack of real investment opportunities at this point, as demand is lagging. There is, however, a lot of money sitting on the sidelines looking for yield. IPOs of companies operating in a more digitised space may attract investors during the second half of the year, as they’re better prepared to work well even in a scenario of continuing pandemics. With this in mind, and at a time when I’m still cautious about the stock market, I suggest four ETFs that allow investors to get an exposure to the IPO market in a systematic and passive way, to avoid the problems and difficulties often related to hand picking stocks.

Four ETFs to benefit from IPOs

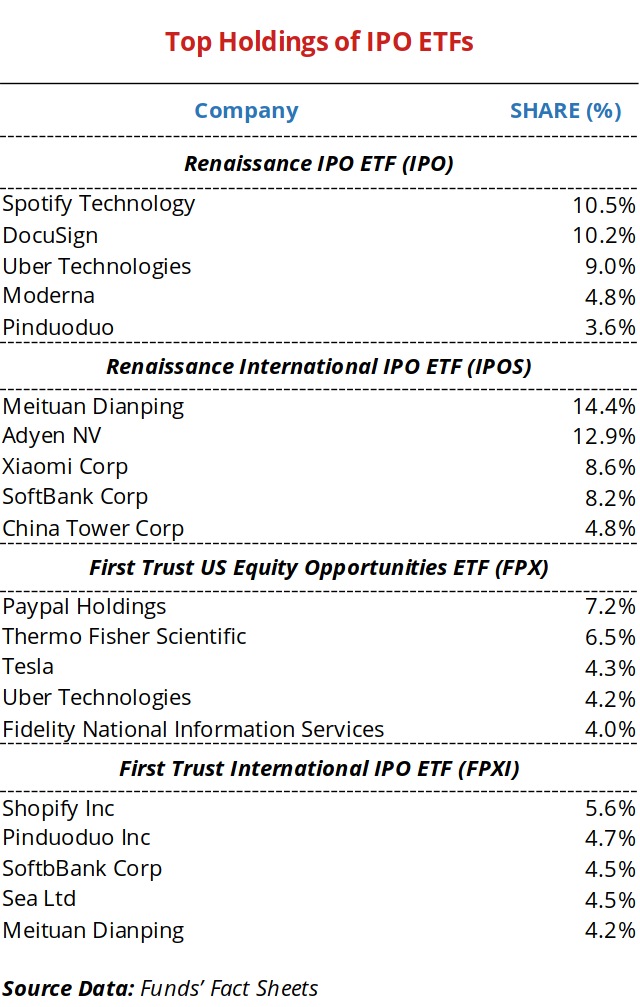

Renaissance IPO ETF (NYSEARCA:IPO)

The Renaissance IPO ETF was created in October 2013 to capture the returns of the most significant US IPOs. New positions to the fund are added on the stock’s fifth day of trading or upon quarterly review. These positions are then removed after two years of trading. IPO is a rules-based ETF which attempts to replicate the price and yield performance of the Renaissance IPO index. Roughly half of its holdings are large-caps, with the other half mid- caps, and they currently include Uber, DocuSign and Spotify. The fund provides an interesting way of getting exposure to rising companies in the US even though it is probably not worth an investment over the longer term, as its performance has not been better than that of the broader market. The expense ratio is not low at 0.60% but it’s not too high for this kind of ETF.

Renaissance International IPO ETF (NYSEARCA:IPOS)

One year after launching their IPO ETF, Renaissance created this additional ETF, which is tailored for investors seeking IPO opportunities around the globe. IPOS only invests outside the US, which means this is the international, non-US version of IPO. For that reason, investors may invest in IPO and IPOS at the same time, as they’re not investing in the same companies. This is confirmed by the correlation between IPO and IPOS being lower than 0.20.

The largest holdings include Meituan Dianping, SoftBank and Xiaomi. The majority of the holdings are from China (46.0%), followed by the Netherlands (10.4%), Japan (6.3%), Germany (6.3%) and the UK (5.3%). IPOS has an expense ratio of 0.80%, which is higher than IPO’s expense ratio. But, in general, the expenses are higher for funds investing internationally.

This ETF adopts a similar stock-selection process to that followed by IPO. Companies are only included on their fifth trading day or upon an end-of-quarter revision.

First Trust Equity Opportunities ETF (NYSEARCA:FPX)

As an alternative to the Renaissance funds, the First Trust Equity Opportunities ETF also invests in the stock of IPOs in the US market. The key characteristics of FPX aren’t much different than those of IPO. However, there are a few subtle differences. FPX seeks investment results that correspond to the price and yield of an equity index called IPOX-100, which is a modified value-weighted price index measuring the performance of the top 100 companies ranked quarterly by market capitalisation in the IPOX Global Composite Index. Roughly speaking, it attempts to capture the performance of the largest IPOs in the US. The constituents of the fund are selected using a rules-based approach. They’re added to the fund on the sixth day of trading and remain eligible to be included in the index for approximately four years. In comparison to IPO, FPX extends the investment period from two to four years and enters a stock one day later.

An important difference between IPO and FPX relates to risk and diversification. FPX invests in 100 stocks, which is more than double the stocks in which IPO invests. It spreads the money more evenly among its holdings and comes with much less risk (as measured by the standard deviation of daily returns). Thus, for risk-averse investors, FPX may be a better choice. Top holdings include Paypal Holdings, Thermo Fisher Scientific, Tesla and Uber Technologies. No holding can surpass 10% of the portfolio. The expense ratio is 0.59% and the inception date for this fund was April 2006.

First Trust International IPO ETF (NASDAQ:FPXI)

To extend its reach to the international IPO market, First Trust offers FPXI, which was created in November 2014 and has expense ratio of 0.70%. The strategy followed is similar to those of the other funds reviewed above. The key goal is to capture the performance of IPOs outside the US. The fund replicates the performance of the IPOX International Index, which tracks the performance of 50 companies. Similar to FPX, the fund invests in stocks on the sixth day of their debut and may keep them for up to four years. Top holdings include Shopify, Pinduoduo, SoftBank, Sea and Meituan Dianping. In terms of country exposure, China represents 40.8% of the fund which is a substantial amount but significantly less than in IPOS. Other country exposures include Germany (9.3%), the Netherlands (8.2%), Japan (7.1%) and Sweden (6.3%).

Interestingly, even though both FPXI and IPOS cover the international public offerings the correlation between them is just 0.21. These two international funds are significantly different, which allows investors to think about them more as complementary rather than as substitutes. However, the risk involved in FPXI is lower than the risk associated with IPOS.

One point to consider is the fact that, unlike what happens between IPO and IPOS, the correlation between FPX and FPXI is a bit high at 0.63. This is not a problem but it’s something to consider for investors willing to invest in both funds at the same time, as a higher correlation means more co-movement and thus less diversification.

Making the right choices

At the moment, it is still too soon to know whether the worst is already behind us or not. The year has been a roller coaster for markets, with bulls and bears fighting hard and market volatility on the high side. Following any good run, the market then seems to be dragged down again, as investors have no idea what the future of Covid-19 will be. We don’t know whether there will be a second wave or not. To be precise, we can’t even say for sure that the first wave has gone, as the number of new cases continues to rise in some parts of the globe. In addition, a US election is coming that promises to be a tough contest, as President Trump is lagging behind and is desperately trying to reopen the economy no matter the consequences.

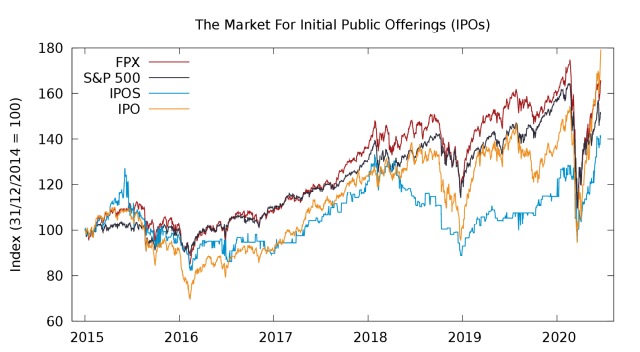

In these circumstances, there are arguments favouring both a bull and a bear market, which means investors need caution. Still, there are a few opportunities in battered-down sectors and in very specific niches. As many companies have been holding back on their IPOs, the second half of the year is expected to see plenty of public offerings and with so much money being thrown at markets by central banks, I believe many of these public offerings will do particularly well. Starting with either IPO or FPX to cover the US market and then adding both IPOS and FPXI into the portfolio offers the tilt I’m looking for here.

A comment on my past passive strategy choices

In previous magazine editions (Passive strategies to exploit an oil recovery − May) and (Passive strategies to benefit from both lockdown and recovery − June), I picked a few oil ETFs in the first case and airlines and gaming ETFs in the second. The oil ETFs are now underperforming the broad S&P 500 market. At the beginning of June, they were clearly outperforming the market but with the volatile moves the market experienced between 7 and 10 May, these stocks were pushed down. However, the market has been recovering part of those losses and I believe the time is still right to keep these ETFs. Since publication on 4 May, an equal-weighted portfolio with these stocks is up 5.8% against 9.0% for the S&P 500. Looking back at my June article, where I highlighted the ETFs JETS, HERO and ESPO, I would still keep them for the months to come. An equal-weighted portfolio composed of the three is up 9.0% since 1 June, while the S&P 500 is up by just 1.4%. As I said at the time, this is a portfolio suitable for recovery and lockdown, as JETS clearly benefits from the reopening of economies while HERO and ESPO can do very well during a lockdown. At times of uncertainty and with Covid-19 numbers still on the rise in some parts of the planet, HERO and ESPO are looking very good.

Comments (0)