Mercifully, the ECB under-delivered

Yesterday, the ECB extended its QE programme until March 2017, cut its deposit rate to -0.30pc and extended its asset purchases to municipal bonds. But with the market expecting an expansion of monthly purchases of around €15 billion and deposit rates to be cut by at least 20 bps, the policy announcement seems more like tinkering than a real attempt at increasing inflation expectations. With the central bank cutting its inflation projections at the same time, it failed to deliver what the market was expecting. The announcement was a massive disappointment for all… well, not all, as the Swiss, the Danish, and the Swedish are certainly now celebrating and taking a deep sigh of relief.

The massive gamble conducted by Mario Draghi cannot pay off at all times. In the past, Draghi was able to over-promise to the market and then convince the other ECB policymakers to back his promises. That was the case when he pledged to do “whatever it takes” to save the euro. It was also the case at the end of 2014 when he hinted at the possible launch of an asset purchase programme to fight deflation. But this time Draghi seems to have been unable to gather the necessary support at the ECB to expand the current asset purchase programme to €75 or €80 billion per month or to cut deposit rates in a significant way. Germany has been opposing the whole programme and the current vote rotation at the ECB was less favourable to Draghi’s ideas than at prior meetings. Some policymakers inside the central bank may even believe this is not the right time to announce any new measures, as the FED is expected to hike its key rate by 25bps at its 16th December meeting, which may play favourably to the Eurozone and remove the urge for further action from the ECB. But still, the under-delivery may create new headaches for the central bank by pushing the value of the euro far too high and by imparting a decrease in inflation expectations that could contribute to an increase in the real interest rate. The Santa Rally has just derailed. All eyes will now be on Janet Yellen to check if she blinks.

In my view, the fact that the ECB is not expanding its asset programme in a significant way is good news. In order to expand its current asset purchase programme the ECB would have to cut its deposit rate further, to -0.40pc or even -0.50pc while also extending the pool of assets eligible for purchase, as government bonds could prove insufficient to feed monthly purchases of more than €60 billion. This could mean extending asset purchases to regional and corporate bonds, leading to a new wave of disagreement inside the central bank. At the same time there are several reasons to question the effectiveness of an asset purchase programme within the Eurozone: (1) corporate financing is highly dependent on bank lending and not on financial markets; (2) the majority of companies are small to medium sized with no access to markets as a funding source; and (3) there is no tradition of households owning financial assets. A few monetary policy channels are expected to fail here.

The core problem in the Eurozone is the disconnect between base money and bank lending, which seems not to have been solved by the adoption of asset purchase programmes.

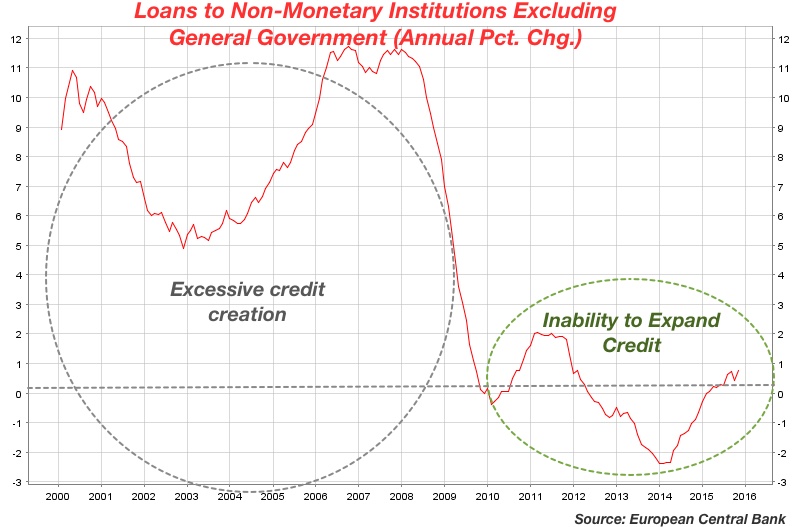

Even though the ECB has been cutting its three key rates since 2008 and adopting several credit enhancing programmes to restore credit conditions, nothing has been effective so far. Since the adoption of the Euro in 1999, until 2009 the expansion of credit to non-financial corporations and households had been growing at stunning rates. Then, suddenly, with the financial collapse felt in the US and its contagion spreading to Europe through the banking system, credit growth turned negative. The above chart shows that loans are not growing; they’re decreasing at ever lower rates. Provided that the ECB is unfolding an asset purchase programme totalling €1.1 trillion (now €1.3 trillion) on top of years of credit-enhancing measures, the effectiveness of such measures is dubious to say the least. The credit channel of monetary policy doesn’t seem to be working properly in a region where bank credit is the main source of funding to corporations.

Additional measures should have been taken long ago. There is no lack of liquidity in the Eurozone. On the contrary, banks have excess liquidity and just don’t have any good uses for it, as there’s no demand for loans, there’s no place to put the excess money and there’s no will to lend because of depressed margins. An expansion of the current asset purchase programme and a deeper cut in deposit rates would further add to banks’ problems, not help alleviate them. If Mario Draghi is allowed to further enhance the current measures, we risk entering a downward spiral in prices and not the opposite. Money will just flow to the equity market until the point the bubble becomes clearly evident and the market crashes.

Another effect of monetary easing occurs through the exchange rate. Since the beginning of this year the ECB has been able to drive the value of the euro down significantly. After today’s big correction, the euro is still down 10pc against the dollar and 7pc against the pound. But, no major development should result from it, as the Eurozone is a relatively closed economy. There’s a lot of trade between member countries but not much with outside countries. The exchange rate can almost be ignored by the ECB. That is not the case for the Riksbank or the SNB, where all that matters is the exchange rate between the krona and the euro (in the first case) and the franc and the euro (in the second). Any change in those rates can lead to massive GDP and inflation changes in the aforementioned countries because they are highly dependent on trade with Eurozone countries.

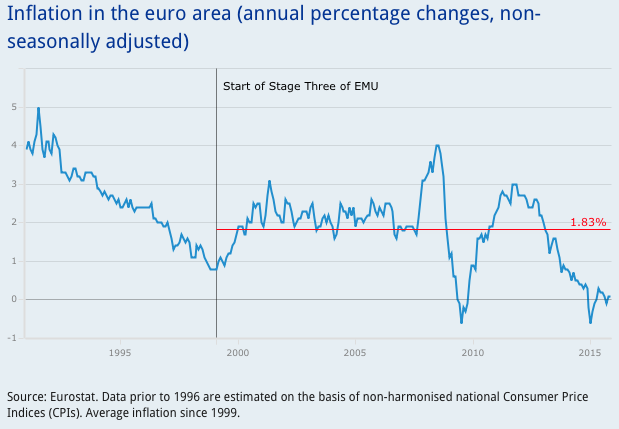

With the exchange rate being a secondary tool, the ECB still aims to change the prices of other assets like equities and residential property in order to create a wealth effect and drive investment and consumption higher. But while we cannot say it has been ineffective in driving the price of both these assets, the change in wealth has not translated into more investment, consumption, and ultimately inflation. Growth in the Eurozone is sluggish and doesn’t show any signs of improvement, and the ECB has just slashed its inflation projection to 0.1% this year, 1.0% in 2016 and 1.5% in 2017.

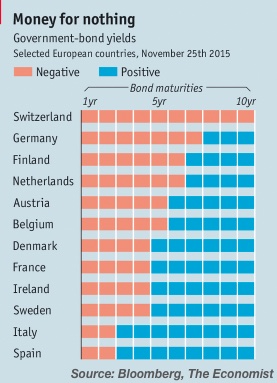

The ECB still believes that it must encourage a decrease in the real interest rate to boost investment. But faced with deflation and already near-zero interest rates, the only way to drive real interest rates down is through surpassing the zero lower bound and setting rates at negative values. The ECB has maintained negative deposit rates for over a year and still seems willing to cut them further. These cuts, along with asset purchases, have led to the proliferation of a negative rate wave, with German government bonds showing negative yields on maturities up to seven years. Even in countries severely hit by fiscal vulnerabilities, like Spain, yields are negative for terms of up to two years. But, in the end, not even negative rates could help convince non-financial corporations and households to invest and buy more. There’s still a missing link that is better explained by the current blind fiscal austerity.

The ECB has exhausted its policy tools without much success. The European economy needs to ease back on austerity and to adopt some serious measures aimed at enhancing the availability of credit for investment purposes. It is not a matter of providing liquidity to banks and forcing them to lend when they just don’t want to; it is a matter of creating the conditions for banks to lend more (in particular for investment purposes). For that to happen we need the central bank to stop trying to depress rates (that should otherwise set freely at much higher levels) and governments to ease back on austerity. Higher rates mixed with less austerity would provide conditions for aggregate demand to rise, for margins to be restored at banks, and for lending to increase.

But instead we have a central bank committed to keeping rates at negative values and creating massive distortions. In the near future we will have corporations trying to pay suppliers in advance and accumulating inventories to safeguard excess money while consumers will be accumulating credit in prepaid phones and in public transport season tickets, as a way of keeping their money in zero-yielding assets.

Traditional wisdom believes that lowering nominal interest rates leads to lower real interest rates. But we have been sketching out a different story, where lower nominal rates lead to lower inflation. It seems that prices adjust in order to keep the real rate unchanged. Under these conditions, the more the central bank pushes rates down, the more entrenched deflation becomes and the more we risk entering a deflationary spiral. Eventually, it would become apparent that the best way to stop deflation would be to allow rates to increase instead.

Comments (0)