Get Ready for an Emerging Markets Crisis

Planting the Seeds

The financial crisis of 2007-2009 is often seen as one of the worst ever crises faced by the US economy. The capitalisation of the S&P 500 was halved, the unemployment rate was doubled, and the Federal Reserve had to go out of bounds in rescuing the economy to avoid the collapse of the whole financial sector. But while the crisis was severely detrimental to the lives of a large minority, in terms of human suffering it was in fact relatively moderate, particularly when we compare it with the Great Depression of the 1930s. If a 10% peak in the unemployment rate and a 4.3% decline in GDP seem damaging, just imagine how decimating the 24.9% unemployment rate and 26.7% decline in GDP were in the 1930s.

What was not so moderate this time round was the intervention of the Federal Reserve. In an attempt to a) provide the needed liquidity; and b) massively increase equity prices and reflate the economy, the Federal Reserve cut its key rate to near zero and injected trillions of dollars to contain the spill-over effects from the financial the crisis. Six years after the peak of the crisis the Federal Reserve is preparing for its first rate hike.

But while everything seems under control in the US, it certainly isn’t in Europe. The spill-over from the US financial sector has engendered huge damage in the fragile Eurozone construction. Without the same kind of help from the ECB that corporate America received from the Federal Reserve, some peripheral countries quickly dove into the cold waters of the Atlantic while others were eventually lost in the Calypso deep of the Mediterranean Sea. But the ECB seems to have learned its lesson and is preparing to follow in the footsteps of the Federal Reserve, in an attempt to revive the drowned European patient by injecting €1.1 trillion directly into his veins.

Ultra-loose monetary policy is the modern solution for all kinds of growth problems; one that is welcomed by investors and emerging markets in general. The near-zero interest rates mixed with large-scale asset purchases led asset prices to explode and made it easier for emerging markets to cut interest rates and issue new debt at a much lower cost. But the ultra-loose cycle always ends in tears when the policy is reversed, often leading to massive currency crises in emerging markets. With the Federal Reserve paving the way for its first rate hike, we can only predict tough times ahead for emerging markets. The first signs are already in place but it is still not too late to act and protect portfolio profits.

Surprise! I Just Cut the Interest Rate…

Since the beginning of 2015, the only business model followed by central banks around the world has been that of cutting interest rates. Asian emerging economies have been particularly busy on the matter, with Singapore, Indonesia, China, Thailand, India and South Korea being just a few examples in a long list of countries following that path – and many of them taking markets by surprise. With the price level under control and record high capital inflows emanating from the zero-yield, developed world, these countries had an epic opportunity to cut rates and regain some economic strength through competitive exchange rate devaluations. It normal times, they would need to keep relatively high interest rates to avoid downward spiralling currency depreciations and the consequent uncontrolled rise in prices, but with major central banks around the world keeping very low interest rates and oil prices plunging, these countries were able to tweak their original business model in their favour.

Situated near Japan and heavily influenced by such a big trading partner, many Asian economies have been benefiting from “Abenomics”. Let’s take the case of South Korea as an example. The country was able to reverse the upward pressure on interest rates in January of 2012, which coincides with Shinzo Abe’s ascent to power and the resulting introduction of a bold plan to reflate the Japanese economy through large-scale asset purchases via the central bank. From a level of 3.25% in 2012, the Bank of Korea has been cutting its benchmark rate to the current record low level of 1.75%, settled on 12th March.

According to IMF data, emerging markets have been experiencing a surge in capital flows from the industrialised world in recent years. Between 2009 and 2012, these countries received inflows amounting to $4.5 trillion (£3.1 trillion). With the advent of negative interest rates in some European countries and the consequent crash in yields, many investors from Europe have been contributing to this trend, which pushes the currencies of these countries higher and helps to sustain abnormally low interest rates.

While there’s no reason to turn away capital inflows, neither is there any reason to open the best French champagne to celebrate it. These countries should distinguish productive capital, which is long lasting and stimulates growth, from hot money flows, which just keeps looking for the best yields and disappears overnight. During recent years, emerging economies have received inflows from many international institutions aimed at building infrastructure, but the bulk of the movement has been speculative in nature and is expected to reverse some time soon. Central banks in Asia are not fully discounting the risks of an interest rate increase in the US, which will most likely pose severe difficulties for them, as hot money will very quickly fly away.

We have already had a glimpse of what could happen, when in 2013 the “taper tantrum” episode led to massive outflows in India and Turkey, as Ben Bernanke hinted the quantitative easing programme would be progressively wound down. If the reaction to a hint of a deceleration in easing is huge, just imagine what would happen when the threat of higher interest rates crystallises into real action. At that point interest rates will rise exponentially in emerging markets to contain massive capital outflows. At a time when economic growth is fading and with country-specific reforms having been postponed, the odds for an emerging markets collapse are very high.

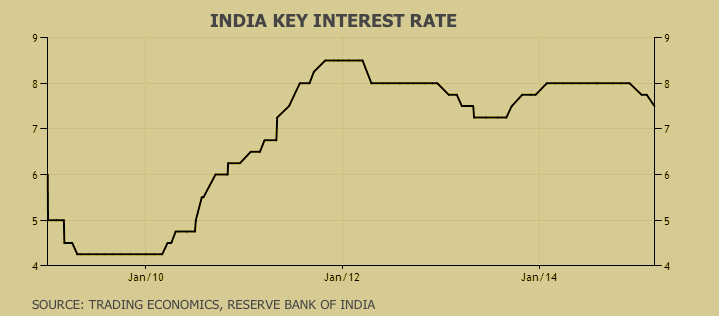

In addition to the potential for capital outflows, there’s another big issue emerging. During the last few years, many companies in emerging countries borrowed funds in US dollars, as they were seduced by a mix of a depressed dollar and an ultra low interest rate. Corporate debt has risen too quickly over the last few years to hit very high levels. When their home currency gets pressured these companies will find it difficult to repay the loans. India is an example of a country that will eventually face such a situation. The Reserve Bank of India does not seem to acknowledge the problem as they joined the group of countries cutting interest rates this year. With a highly indebted corporate sector, the rupee will be one of the first currencies to be pressed, which will force the central bank into action if it is to avert a collapse.

America Vs Asia – Two Different Realities

While everything seems fine in Asia (for now), the pressure has already begun in America. Brazil, the second largest emerging economy, is walking on very thin ice, and has been shaken by a mix of political scandals and a stronger dollar. Even though one cannot forget the political issues involved in the current picture, the rising dollar is still largely responsible for the looming crisis.

The rising dollar presses Brazil in two ways. Firstly, as commodities are quoted in US dollars in international markets, a rising dollar often means declining commodity prices. For a country so heavily dependent on commodity exports, GDP growth is severely affected by such a decline. Secondly, the rising dollar leads Brazil to import inflation, which is already reflected in the acceleration of its inflation rate to 8% per year.

The Brazilian central bank’s key rate is currently set at 12.75% – the highest level in 6 years – but that is still not enough to contain the depreciation of the Brazilian real against the US dollar. The central bank assumed its currency would trade at an exchange rate of R$2.65 per dollar over the next 2 years (on average), but the current rate is already at R$3.25, or 22% above its 2-year projection. The advent of the financial crisis helped the Brazilian real, which traded at a high of R$1.50 in July 2011, but as the dollar started strengthening with the prospects of a monetary policy inversion in the US, the currency lost value very quickly. The dollar has gained 22% against the Brazilian real year-to-date. An interest rate rise to the 20% seen in 2005 should not be ruled out for the near future; a level that may prevent further depreciation but would certainly throw the country into a heavy recession.

Now let’s take a look at the US’s southern neighbour – Mexico. The Banco de Mexico has its key interest rate at 3%, as inflation is still subdued. But the exchange rate between the dollar and the Mexican peso is quickly appreciating. While you could buy a dollar with Mex$12.8 in May 2014, you now need Mex$15.5. I guess it won’t take long for inflation to start rising, pressing the central bank to increase interest rates to avert a currency crisis. For now, many still predict a further rate cut of 25 bps, which seems ever more unlikely for me, especially given the likely scenario of rate increases in the US.

Final Comments

Declining global US dollar liquidity growth mixed with falling commodity prices are the necessary ingredients for an emerging markets crisis. For now the emerging markets world seems very quiet and the main equity indices are still not showing any severe weakness, as plunging oil prices have helped contain production costs in many of these countries and European QE has offset some of the fears over Federal Reserve tightening. But I expect the current trend to be reversed very quickly as the first rate hike in the US approaches. The pressure in South America is already visible and should serve as a preview for what the future holds for the other countries.

In a world led by central bank action and by manipulated interest rates instead of substantive action to address the real problems facing the global economy, we will simply lurch from one crisis to another. Today’s crisis in country A becomes tomorrow’s crisis in country B, in a Ponzy scheme that can only end in disaster.

Instead of allowing malinvestments to be liquidated, central banks keep adding credit to a bankrupt system. But such a system is unable to generate any wealth and only looks temporarily profitable due to the artificially low interest rates set by central banks. When monetary policy ultimately returns to some kind of normality, the problem will by then be bigger than ever, albeit shuffled to a different place… that place is now the emerging markets.

Comments (0)