The FED loses momentum again with ‘dusty’ jobs report

After a quiet August, we are back to business as usual, which is 90% about following central banks and 10% about following everybody else. Almost one decade after the peak of the financial crisis, global markets still rely heavily on central banks, with short-term volatility being fuelled by all kinds of speculation about expected central bank action. Last Friday was one of those ‘big Fridays’, when the US Labour Department released its monthly jobs data. Those anxiously waiting for the report to clear the picture about the next rate hike, have mostly been hit with dust, as the soft numbers just released don’t help much. Markets are rising but the FED seems to have lost momentum once again. With investors cutting the odds for a September hike, the FED may opt to delay intervention, to avoid a market crash at a time when jobs data is softer. The million-dollar question “when will the FED hike again?” regained life on Friday and the FED will most likely wait for further updates on the job market before doing something. If there’s a winner this year it must be gold, which seems to be a safer bet regarding the suspense around central bank action, the perpetual delay in rate hikes and the still-low-but-rising probability of a surprise inflation occurring at some point in the very near future.

The FED has been playing games with investors for years, always trying to massage expectations in an attempt to accommodate the best scenario to introduce rate hikes. But, while seeking the optimal scenario, the central bank has been losing momentum, as the data continues to come in softer every time a rate hike becomes more likely. This time it was about the job market, which added 151,000 jobs in August, much below the expected 180,000 (according to WSJ surveyed economists). The Labour Department revised past figures but without producing much of a net effect, as June was revised down from 292,000 to 271,000 while July was revised up from 255,000 to 275,000. The jobless rate remained at 4.9% for a third straight month and the average hourly wage growth came in at 2.4%.

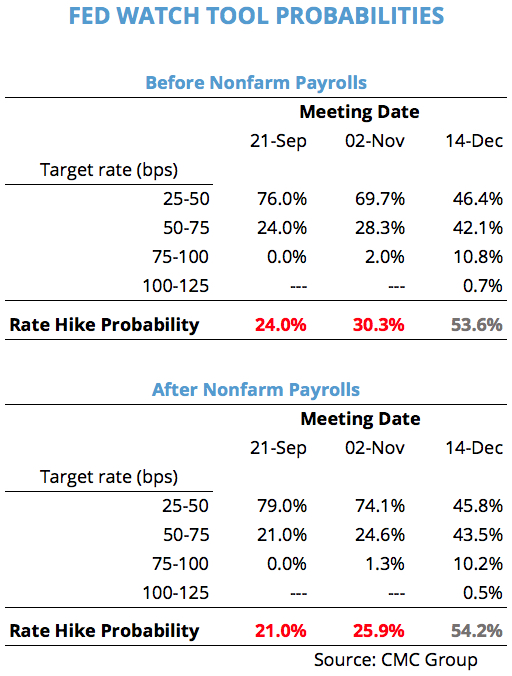

The jobs data reported in June and July was really strong and if proceeded by a strong jobs report last Friday, would likely create the conditions the FED was looking for to hike its key rate in the next meeting on 21 September. But with the numbers coming in below 200,000 and much softer than expected, the uncertainty about the next rate hike timing remains, with the decision eventually being pushed further to the end of the year when more data would be available on the relative strength observed in June/July.

There are four key points to focus on the August jobs report: (1) the pace of hiring dictated by jobs growth, (2) the jobless rate, (3) the pace of wage gains, and (4) changes in the participation rate.

The pace of hiring

Regarding the pace of hiring, the report is unclear. The soft numbers coming on top of the best two-month period in years make us believe that August may be an exception rather than an inversion in trend. In fact, August has been historically the worst month in terms of job gains over the past 25 years. Additionally, August is the month when the Labour Department re-benchmarks a lot of employment data. For the last 4 years’, payroll numbers have been lifted by an average of 71,000 jobs on subsequent revisions. If that trend remains, the numbers may be substantially revised higher in September and/or October.

A breakdown of job gains by sector shows that food services and drinking places along with healthcare and professional business were the sectors adding more jobs (34,000 and 22,000 respectively). These are not the higher-paying sectors everyone is waiting for to help justify a rate hike.

Jobless rates

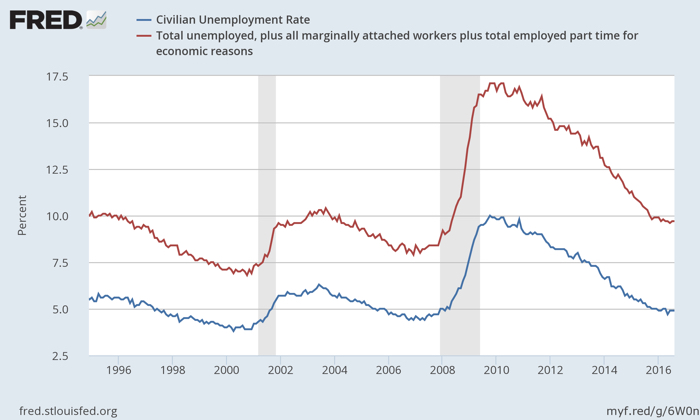

Let’s start with the key jobless rate, which is the U3 measure. The numbers came in line with the last three months at 4.9% but are slightly higher than the expected reduction to 4.8%. While being a decent number, it doesn’t tell the full story. The U6 measure is preferable in helping to understand how tight the job market is, by adding discouraged workers, marginally attached workers and part-time workers for economic reasons to the jobless rate. However, these people are working in sub-optimal conditions. When the job market becomes tighter it is expected that the U6 measure continues to shrink even if the U3 measure remains relatively unchanged. That has not been the case for the last few months as both measures seem to have stagnated. In my view, this means that the job market is not really close to full employment and that is the main reason why inflation isn’t picking up and wage growth is not great.

The U6 measure is still much above its pre-crisis level, which will certainly be weighted by the FED.

Wage Gains

The numbers are not bad at all, as wages grew by 2.4% from a year ago. But again, by looking at the relative high figures for the U6 statistics, it doesn’t appear that we are at a juncture where wage growth is going to spiral higher.

Participation rate

The participation rate continues to be at a very low level by historical means, near 62.8%. The number has been hovering between 62% and 63% for more than two years, down from 66% at pre-crisis. While there are certainly several reasons explaining the decline, there’s one that stands out: many workers abandoned the workforce as they couldn’t find a job. So, thinking in the opposite direction leads us to believe that before the job market really warms, we still need to see this figure going higher again. Improving conditions attract more people to the workforce. That doesn’t seem to have been the case so far, even though the 4.9% unemployment rate makes us believe that.

What it all means for investors

While the knee-jerk reaction has been to significantly downgrade projections for rate hikes in September and/or November, in the meantime the odds were smoothed. Like I previously mentioned, if anything, this job report adds dust to the overall picture and requires us to wait for the next report to get a clearer picture, in particular because of the reasons shadowing reports published in August, as pointed out above.

Overall, I believe the job market is recovering well in the US and doesn’t justify a rate of just 0.50%. But the FED is too concerned with the market reaction to any hike and is waiting for the best momentum to do something. This job report certainly eroded its prospects and a rate hike in September is now less likely. But if the August numbers are significantly revised higher at the end of September and the data for the month of September confirms the June/July strength, the door would be finally open and the FED would by then take the opportunity.

For now I’m still happy with Market Vectors Gold Miners ETF (NYSEARCA:GDX) and with Market Vectors Junior Gold Miners ETF (NYSEARCA:GDXJ), which are leveraged bets on gold. I suspect the USD may ease a little but more as a pause in the current upside rather than as an inversion in trend.

Comments (0)