Can the ECB Boost Bank Lending?

Starting with good intentions

The idea of creating an independent central bank to assure that money flows efficiently through the banking system and in the direction of the real economy is good in principle. A central bank can provide high street banks with the necessary reserves for them to back up their lending activities, and convert their illiquid collateral into the most liquid assets on earth: reserves and physical currency. When a liquidity crisis occurs – and everybody reaches for physical currency at all costs and interbank lending fails – the system would brutally collapse, dragging solvent banks underwater and preventing households and non-financial corporations from getting the funds they need to finance their day-to-day activities. While one can argue both sides of whether an insolvent bank should be bailed out or not, there is a wide consensus that we should create conditions for solvent businesses to survive. A central bank that converts high quality collateral to bank reserves is of significant value at such times.

But the idea of a central bank working like a blender where banks insert their solid collateral to liquefy them into liquid reserves became too passive for central bankers. It requires them to wait for banks to come up with collateral before doing anything. What about if the central bank could just liquefy whatever it wants by forcing banks to convert illiquid collateral into bank reserves?

That is exactly what happens today. Central banks use open market operations and large-scale asset purchases to convert illiquid assets into reserves in the hope that they can seduce banks to lend more to boost investment, output, employment and, ultimately, inflation.

After the Lehman Brothers collapse in September 2008, banks entered a period of massive deleveraging, during which they saw their balance sheets shrink while households and companies also had to cut their expenses. To boost growth and avoid a depression, central banks quickly started cutting interest rates. Ben Bernanke convinced everyone of the need to boost banks’ liquidity for them to start lending again. The ECB, by its turn, quickly cut its 4.25% main refinancing rate to 3.75% just after Lehman’s collapse and then successively cut it to the zero lower bound. At the same time, the ECB also tweaked its main refinancing operations, giving them a new body with full-allotment and fixed rates to assure banks could get all the liquidity they needed. So far, so good. In the interest of preventing banks from failing en masse, the liquidity-providing operations were key, in particular in Europe where bank lending is the main source of financing for small and medium sized businesses. But Bernanke and Draghi failed to understand that banks’ balance sheets shrank, not because of a lack of liquidity, but rather because there were no borrowers, and then no deposits.

Forcing reserves into the system

Providing liquidity at banks’ discretion is no longer the goal of a central bank. The central bank now provides liquidity way beyond banks’ needs. Ben Bernanke flooded the banking system with trillions of dollars and the ECB is now following the same route. The problem is that banks, flooded with liquidity, and facing very low rates and weak economic prospects, are unable to lend the excess reserves and instead simply deposit it back at the central bank. To avoid this leak, the ECB cut the rate on its deposit facility to a negative value. Still, such a measure was unable to do much for bank lending.

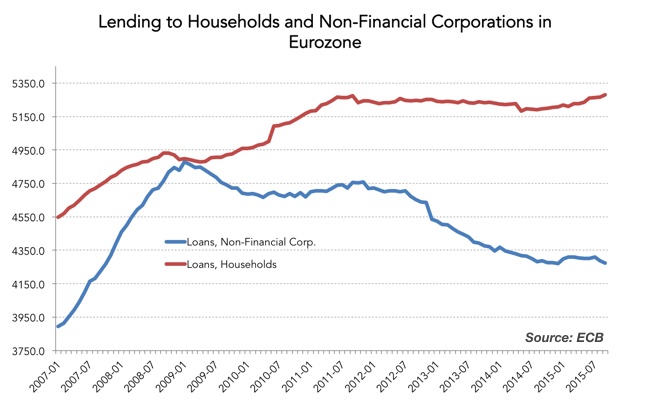

Bank lending in the Eurozone had been growing spectacularly before the financial crisis. Lending to non-financial corporations peaked at €4.88 trillion in January 2009, after growing 10% in 2008 on top of 14.3% in 2007. For the entire period between 2000 and 2008, loans to non-financial corporations grew at a compound rate of 7.9%. Such a growth rate certainly surpassed GDP growth by a significant margin, and contributed to inventory accumulation and what the Austrian school of economics would denominate as ‘malinvestments’. At the same time, loans to households also grew significantly (albeit at the slower pace of 6.6%).

The financial and debt crises are partially the natural consequences of years of unsound credit growth. The best the central bank could do would be to provide the necessary liquidity as a lender of last resort to avoid an unorderly collapse, but to stop right there. If too much credit is at the root of the problem, seducing banks to provide credit again is counter intuitive, to say the least.

After peaking at €4.88 trillion, loans to non-financial corporations declined over time until reaching the current level of €4.27 trillion, which is more or less at its lowest level since peaking in January 2009. Not even the €60 trillion asset purchase programme deployed by the ECB was able to boost lending in a significant way. Loans to non-financial corporations grew 0.04% this year while loans to households grew 1.4%. Of course, in a system that depends heavily on credit, this massive deleveraging could only result in sluggish growth, high unemployment levels, and a lack of inflation.

During recent years the ECB has resorted to every trick in the book: low interest rates, enhanced credit measures, extensions of existing open market operations, negative deposit rates, large-scale asset purchases. Nothing seems to work in terms of converting reserves into deposits. But the ECB continues to insist on lowering the real interest rate because it sees that as being the most influential variable on which companies base their investment decisions. David Stockman very well explains the problem faced by Ben Bernanke (which is not much different in essence from that faced by Mario Draghi):

“Friedman and his followers, including Bernanke, came up with an academic canard to explain away these obvious facts. Since the wholesale price level had fallen sharply during the forty-five months after the crash, they claimed that “real” interest rates were inordinately high after adjusting for deflation. Yet this is academic pettifoggery. Real-world businessmen confronted with plummeting order books would have eschewed new borrowing for the obvious reason that they had no need for funds, not because they deemed the “deflation-adjusted” interest rate too high.”

The key to the puzzle is a lack of real opportunities to lend money. Banks no longer have the same level of solvent clients as they did before the crisis to whom they can lend money. At the same time, demand for money is also limited, as companies still face high inventories, too much capacity, and a very sluggish consumer. Any attempt from the central bank to pump reserves into the system through a one-way pipeline (with the help of a negative deposit rate) will just derail in the direction of financial markets. But the ECB still believes it can boost growth and inflation with excess reserves and then will eventually increase the pace of its asset purchases to something near the €75 trillion level and push its deposit rate into further negative territory at -0.30%.

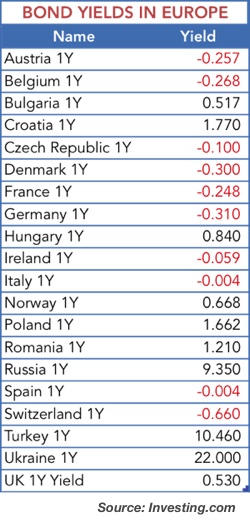

While blindly trying to boost inflation because of an ill-formed concept that sees investment as a positive function of deflation-adjusted interest rates, the ECB (along with many other central banks) is just creating huge economic distortions and asset bubbles. Yields on European sovereign bonds are insanely distorted: seven countries are now showing a 5-year negative yield, Switzerland also shows a negative 10-year yield, and for a 1-year maturity many of them are already near the -0.30% threshold that investors expect the ECB to set its deposit facility at in December. Under these conditions yields no longer reflect economic reality.

Allow me to mention David Stockman once again. He very well claims that central bankers have an ill-formed view about what happened during the Great Depression in the 1930’s. They believe that, had monetary policy been more aggressive during the crisis, the Great Depression could have been avoided. But the main problem is that they wrongly believe that the economy shrank because banks cut lending. Actually, banks saw their lending decline because there was a lack of borrowers. When growth is financed by skyrocketing debt, a time comes when the unsustainability of it becomes evident and inventories start accumulating. At that point, a central bank may provide liquidity to prevent a wider collapse of the economy, but it is unable to boost investment through a deflation-adjusted low interest rate. Banks follow the economy and then are unable to lend. The economy needs to get rid of past excesses and any attempt to boost lending will result in further distortions and bad investment decisions. Europe has already lost a decade. Does it really need to lose another?

Comments (0)