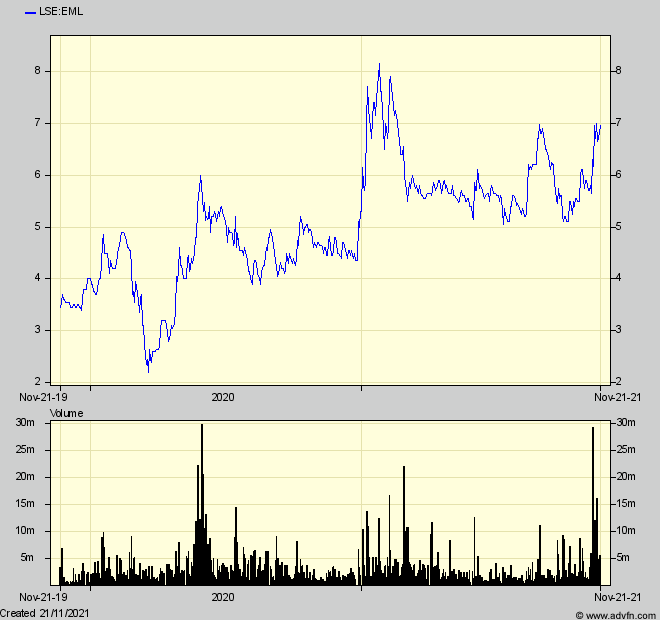

Emmerson on the move in Morocco

When, last March 3rd, I mentioned Emmerson (EML) – developing its Khemisset potash project in Morocco – the shares hadn’t moved much from my initial one in Sept 2020. Then I had said EML looked interesting with my projection for a NPV per share around six times the then share price – after what I thought would have to be a similar % increase in its shares to part pay for Khemisset’s $400m up-front capital cost.

After a rather long drawn-out search for the project funding necessary on top of that share increase, a key milestone has now been achieved with the coming on board of a strategic investor, providing funds to help along the work still needed to persuade the banks, and perhaps off-take partners, to commit what looks like $350-$400m still needed before construction can start – hopefully in mid 2022, with first revenues in 2024.

But the shares are still hesitating, despite talk on social media that the project’s updated NPV of $1,400m (£1,050m) at a 8% annual discount rate must be a steal against EML’s current £57m market cap. It seems even more so given a current potash price nearly double the $360/t assumed in the feasibility study, although because that is partly due to bottlenecks at existing producers, bankers and institutions will probably stick with the study assumptions.

Even so, the deal looks much better for the shares than a year ago, despite some time to go before Khemisset can come together. But with readers knowing my views on the irrelevance (except in a very round-about way) of an NPV to a share price, and of all the other adjustments needed to project a realistic share price, it might be time for me to perform my usual Devil’s advocacy and go through the factors that get between an NPV for a company’s project, and the company’s share price. They might explain why the shares are still hesitating, but also perhaps when they might merit buying.

Amongst the largest, never appreciated at all by private investors, is the length of a project in relation to its NPV. Khemisset’s $1.4bn takes in earnings up to 19 years ahead, and even for a reliable mining project (and for any other share sector if forward earnings are projected to mimic a NPV) investors rarely accord a share a value reflecting more than ten years of its projected earnings (ie akin to its PER).

It was because Sirius Mining (which I don’t apologise for mentioning again) tried to pretend its shares were ‘worth’ the total (even if discounted) of its projected earnings up to 55 years ahead, that its fund raisings failed.

I’m not saying EML will go the way of SXX. But I point out that it is using the same broker (Shore Capital) and the same analysts, as over-egged the Sirius story. So I don’t think the institutional investors who will set the share price when EML raises the Khemisset funds next year will give credit for more than half whatever NPV (at a 8% discount rate) per share will be projected at that point.

And that is not the full story, because neither will they pay ‘up-front’ for that NPV. Many investors don’t realise that when they pay the NPV for a limited life project, assuming the earnings or dividends they get turn out as projected, they will merely get back their initial investment, plus the annual discount rate used to calculate the NPV. (the same as if buying an annuity over that life) No sensible investor would assume the risks of a mining project for only the 8% return used for Khemisset. Institutional investors expect a lot more.

So that’s another ‘discount’ institutional investors will apply to any NPV. Its why during the last mining boom in 2011, I couldn’t find any mining share price higher than 1/3rd its theoretical ‘NPV’ per share. Yet the latter is always what companies and brokers use to suggest what their share price should be.

In the face of that however, EML is saying “The recent strength in potash clearly improves Khemisset’s already outstanding economics and, using current spot price, would push our post-tax NPV8 from US$1.4 billion to US$3.9 billion4 and IRR of over 85.4%, while average life of mine post tax cashflow would increase to US$558 million per annum for an initial 19-year life of mine.

That looks impressive, but to put some numbers on it all and consider whether and when the shares might be worth buying, here they are, with my comments.

The cornerstone investors, Global Sustainable Minerals Pte (GSM) based in Singapore, and their banking advisor and others, initially have bought 81.8m new EML shares at 6p, adding to 833.2m already in issue. In addition they have committed to subscribe for $40m in loan notes, convertible at 8.2p for two years (at $1.33/£ – into another 367m shares),on top of which, following shareholders’ agreement at an EGM on Dec 6th, , they will be issued with 82.4m warrants exercisable at 8.2p for one year.

That gives GCM potentially 531.2m shares which, following the further share issues necessary for full Khemisset funding in which they might also participate, they have warranted will not exceed 29.9% of the company.

That initial ‘cornerstone’ package will give EML up to $47m (£35m) to meet the costs of preliminary engineering works, investigations, and negotiations with contractors and bankers to define a more detailed cost and funding plan (so far only to 30% accuracy)

That leaves the full (perhaps $400m) project funding package, including what EML will have to raise through issuing shares to meet the equity element of the Khemisset project funding that lenders will demand that it contributes. Because the study forecasts a high rate of return and rapid cash payback, EML expects this won’t be more than 30% against the 70% that banks and potash off-takers might contribute. So current shareholders will have to stump up some $120m – or (say) £100m to be on the safe side.

While bank loans are typically repaid over 6- 8 years at perhaps 8% interest, off-take or streaming funds aren’t, but are struck as discounts on sales revenues which are usually quite substantial and equivalent to higher interest rates than banks impose.

Putting this together, the cost for that $280m, assuming half from banks and half from streamers or off-takers, will start out at $21m pa interest and capital repayments to the banks for 8 years, and the equivalent of another $21m pa to the off-takers over the life of the project.

This cost will come out of whatever cash flows have been used to calculate the NPV, but on the other hand, because it replaces the $400m capex used in the NPV calculation, $400m can be added back to the PV that will flow to the project shareholders after construction has been paid for.

I estimate the NPV of these funding costs to be deducted from the project NPV will amount to $200m. So the true NPV that shareholders will see from the project will be $1,400m + $400m – $200m = $1,600m, and this will be shared among project shareholders including GSM and EML. (I have assumed that GSM won’t participate in next year’s equity funding. If they do, they will take a bigger share)

That leaves the $120m equity contribution from EML shareholders. The company has speculated that the share price at which it will be raised should be at least 16p ($21). Let’s see!

If at 16p, 570m EML shares need to be issued, meaning the total then, after the CLN note conversion and including GSM’s warrants will be 1,935m.

Dividing the then NPV into those gives a NPV of 82.7c or 62p per share. So that is pretty impressive even after the adjustments I would make, (nearly halving the NPV to take in 10 project years instead of 19) meaning 16p and even higher looks easily achievable.

I’ve left out a few other factors like the 9% loan note interest which could give GSM another 65m or so shares. And I’ve also left out the calculations institutions will make to get from the NPV, to the actual cash flows year by year which are what will determine the share price more accurately than the NPV. (Because an NPV gives no clue as to the variability of project cash flows over the mine life. Sometimes it can be substantial, but investors relying on an NPV won’t know about it.)

That also needs the full project study which companies rarely release except to banks and institutions. And that is without considering whether the 8% discount rate used to calculate the NPV is the ‘right’ one that institutions will use. (using 10% instead of 8% will reduce the NPV by 17%. Conversely, using 5% will increase it by 35%)

But assuming all goes to plan over the next six – eight months until (hopefully) financial close (including that the more detailed feasibility study the banks are demanding won’t upset the NPV calculations, and that potash prices remain strong, and provided global interest rates don’t take a sudden hike) there seems enough margin between even a significantly ‘adjusted’ $1,400m NPV to think EML shares should at least double meanwhile. So its over to the chartists…

Thanks John- very well considered comments re EML there. Any chance you can update your thoughts on the HZM funding that has just been announced please? It looks very well structured to me but it is drawing heat from some private investors who seem to expect the funding to come from thin air and at nil cost.