Why cash flow keeps you on the straight and narrow

Job Curtis, Fund Manager of the City of London Investment Trust, explains why cash flow is so important when investing in equities for the purpose of income, using two stock case studies.

Estimating a company’s future cash flows is a common method of share-price valuation. For investors seeking dividend income from shares, cash flow is crucial. In our view, successful income investing involves identifying companies with enough cash flow not only to pay their dividend, but also to invest enough to generate future profit growth. While it is possible to grow a dividend with debt, this is unlikely to lead to sustainable dividend growth and will leave a company poorly placed for a cyclical downturn. A company with a heavy burden of debt facing falling demand for its goods and services, leading to reduced profits, will inevitably prioritise interest payments to service its debt. Such an indebted company is more likely to cut its dividend compared with a company that has no debt or a low level of borrowings.

To illustrate some of the complexities in understanding cash flows and dividend sustainability, the oil sector offers a useful example. Royal Dutch Shell (RDS) is the largest company by market capitalisation listed on the London Stock Exchange and BP is the fourth largest. RDS has one of the best dividend records of any company, having not cut its dividend since World War II. BP’s record is more volatile over the long term and it had to suspend its dividend for six months in 2010 after the Macondo oil-spill tragedy in the Gulf of Mexico.

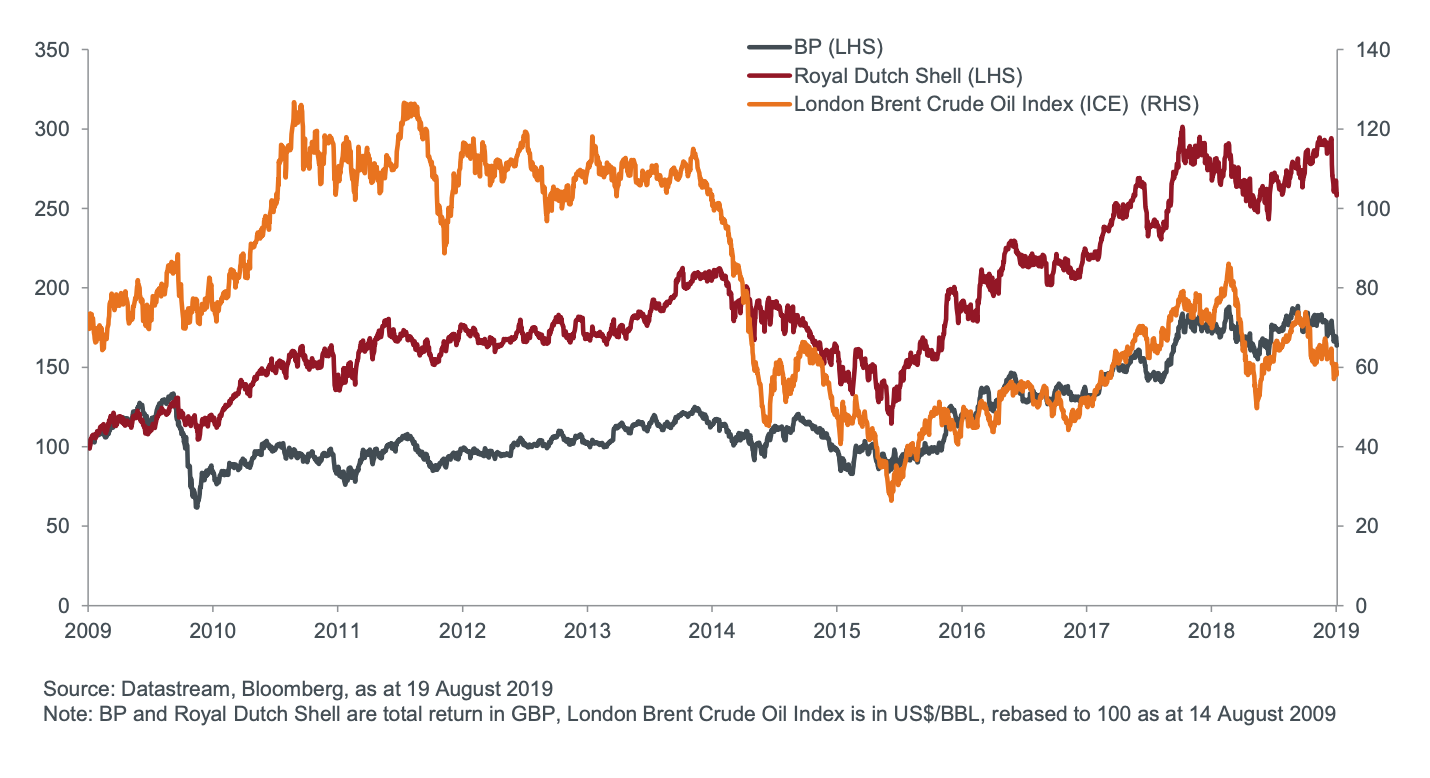

The key determinant of cash flow for RDS and BP in the short term is the oil price, which will affect the profitability of their oil fields that are in production. It also has a significant bearing on their large natural-gas businesses, where long-term contracts continue to have high linkage to the oil price. The chart below compares the oil price over the last 10 years, with the total return from the shares of RDS and BP. Overall, it indicates a fairly close correlation, as well as showing the companies have responded well to the lower oil-price environment since 2015.

Figure 1

Both companies also have large ’downstream’ operations, which encompass chemicals, refining and marketing (such as petrol stations). In general, these downstream operations are countercyclical and RDS and BP are able to earn a better profit margin on them during oil-price downturns.

A further feature to consider when predicting cash flow for both companies is their level of investment. Oil fields deplete and therefore it is necessary to replace production by investing in new fields. During the oil-price boom of 2005-2011, the industry invested heavily, pushing costs higher, leading to disappointing profitability despite the supportive oil-price environment. Since 2014, both companies have been much more disciplined on capital expenditure, although this leads to some questioning on whether they are investing enough for the future.

One alternative to investment is to make an acquisition. In 2015/2016, during the oil-price bear market, RDS agreed to buy and completed the acquisition of BG Group (BG) for £47 billion, which gave it high-quality oil fields off the coast of Brazil and enhanced its global leadership in natural gas. More recently, in 2018, BP acquired some US shale-oil assets from BHP for $10.5 billion. Disposals also complicate the picture, with RDS selling off assets to help pay for BG and BP doing likewise to pay for claims and fines arising from the Macondo disaster, of some $67 billion.

All in all, the above shows how difficult it is to judge the cash flows and profitability of these giant companies. The consensus of analysts is that RDS and BP have improved a lot from the dark days of 2015/2016, when cash coverage of their dividends was low and the dividends had to be paid partly by issuing new shares. The fact that both stocks yield over 6% indicates a degree of market scepticism about their dividend sustainability, which should be disproved as predicted cash-flow generation comes through.

Glossary

Dividend: a payment made by a company to its shareholders. The amount is variable, and is paid as a portion of the company’s profits.

Cyclical downturn: a period of economic contraction during which certain industries are vulnerable to weaker cash flow, resulting from tight monetary conditions.

Volatility: the rate and extent at which the price of a portfolio, security or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. It is used as a measure of the riskiness of an investment.

Bear market: afinancial market in which the prices of securities are falling. A generally accepted definition is a fall of 20% or more in an index over at least a two-month period. The opposite of a bull market.

For UK investors only. For promotional purposes. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Nothing in this communication is intended to be or should be construed as advice.This article is not a recommendation to sell or purchase any investment. References made to individual securities should not constitute or form part of any offer or solicitation to issue, sell, subscribe or purchase the security.Before investing in any investment referred to in this communication, you should satisfy yourself as to its suitability and the risks involved. Tax assumptions and reliefs depend upon an investor’s particular circumstances and may change if those circumstances or the law change.

Issued in the UK by Janus Henderson Investors. Janus Henderson Investors is the name under which investment products and services are provided by Janus Capital International Limited (reg no. 3594615), Henderson Global Investors Limited (reg. no. 906355), Henderson Investment Funds Limited (reg. no. 2678531), AlphaGen Capital Limited (reg. no. 962757), Henderson Equity Partners Limited (reg. no.2606646), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Henderson Management S.A. (reg no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier). Janus Henderson, Janus, Henderson and Knowledge. Shared are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.

Comments (0)