How to generate a sustainable long-term income – SPONSORED CONTENT

It’s not enough to have the capital to provide an income – how effectively you preserve that capital has a direct result on how long you can generate a sustainable income, explains Charlotte Ransom, CEO of Netwealth Investments.

For many investors, their main priority is to generate and sustain a consistent income. This is usually in retirement, but it can be valuable at any stage in life. Of course, having a regular income is one thing, but how do you ensure that you can make it last?

It’s not enough to have the capital to provide an income – how effectively you preserve that capital has a direct result on how long you can generate a sustainable income.

The persistent effect of inflation

Spending beyond your means will obviously reduce your income pot quickly, but that is something you can control. What you can’t control is the effect of inflation, which can cause serious harm to your total funds over time. So those seeking income must first ensure that their capital is aiming to outpace the rate of inflation.

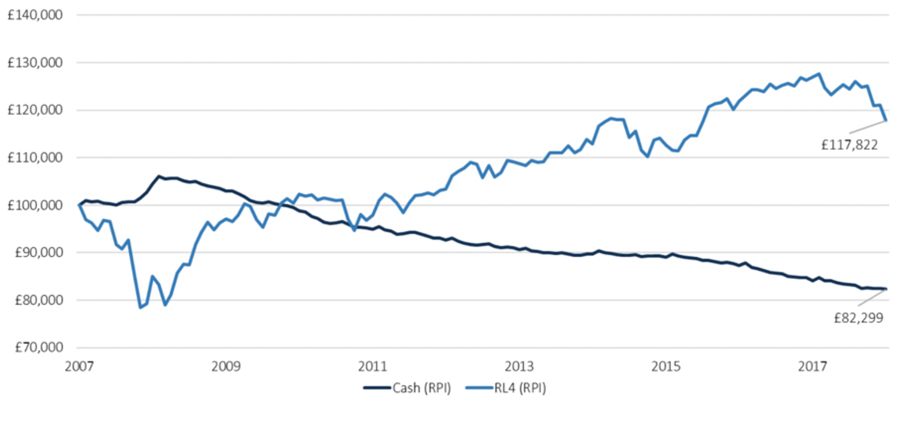

For example, let’s take the period from the end of 2007 to the end of 2018 which accounts for a time of both strong overall stock market growth and includes a considerable decline. If you had left your nominal £100,000 ’safely’ in a bank account, its actual purchasing power – after retail price inflation – would have slumped to £82,299. By investing in a balanced portfolio on the other hand, such as Netwealth’s medium risk portfolio (Risk Level 4), the invested capital would have risen to £117,822 over the same period.

Chart: How inflation can deplete your income pot over time

Source: Bloomberg, Netwealth Investments’ Calculations. Past performance is no guarantee of future performance.

Providing an income in all environments

Stock markets go up and down, as does the level of growth in economies. Income seekers value consistency since they are targeting regular cashflows, but what happens if there is a bear market and the stock market falls for an extended period? If you rely on dividends from single stocks or an equity fund to provide your income, your income level may be maintained for a while, but your capital is likely to be dented, reducing the length of time an income can be drawn from it. This is why a diversified portfolio, that blends returns from both global stock markets and fixed income bonds, is often valuable as a way to smooth returns over time while cashflows are being drawn from the investment pot

How a total return approach, rather than a pure income approach, can provide a sustainable income

We often read about income-based funds; however, portfolios designed purely for income necessarily focus on a narrower set of opportunities – there are only so many stocks and bonds whose dividends and coupons are attractive and predictable enough for an income manager. The risk is that income funds become too concentrated in similar assets and may miss out on important returns elsewhere.

A better alternative is for wealth managers to take a more rounded approach to building portfolios. An emphasis on the total return from a portfolio means it isn’t restricted to chasing potentially expensive income assets; the manager can be agnostic as to whether returns come from dividends, interest or capital appreciation, allowing for more drivers of portfolio performance.

Importantly, smarter technology, such as at wealth manager Netwealth, enables clients to design a personally tailored cashflow strategy with ease, funded from different portfolio components. This provides the opportunity to match payment requirements precisely, driven from a portfolio’s total return rather than relying on a narrow set of income-based assets. We believe that combining a more balanced portfolio targeting total returns, with tailored cashflows, is a better approach for those who are seeking income.

Watch out for high fees

We’ve stated that inflation will deplete returns, but excessive fees can do just as much damage to a pot of money over time. When you invest, even paying 1% more than necessary in fees each year makes a big difference to how much you may earn from your capital. For example, the cost of an extra 1% per year in fees can amount to as much as 15% of capital being eroded over a 10-year period, or £15,000 per £100,000 invested.

If you know how much you are paying in fees each year – or even if you don’t – you should find out how much better off you could be when you pay less. You can make a meaningful difference to your income plans.

Speak to one of our advisers on 020 3795 4747 to learn more, or visit netwealth.com

Please remember that when investing your capital is at risk.

Comments (0)