The equity market bubble continues to play out in text book fashion…

By John Hussman

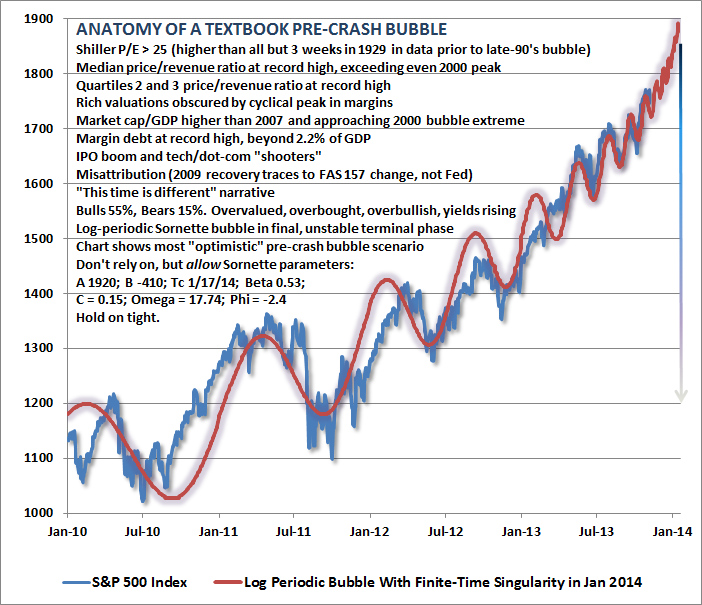

The following chart is reprinted from our November 11, 2013 weekly comment A Textbook Pre-Crash Bubble. What is important, in my view, is not simply the log-periodic structure, but the broad array of additional classic speculative features that emerged as the market approached its recent highs.

A few months ago, Bill Hester examined a century of price data, and observed that the non-overlapping periods most closely correlated with the past 5-year trajectory of the S&P 500 were the advances preceding the 2007, 2000, 1987, 1937 and 1929 market peaks. This shouldn’t be a surprise – the past 5-years have largely resembled a diagonal line, as did the advances to those extraordinary market peaks. Diagonal lines always have a nearly perfect correlation even if there is some amount of variation along the way.

Again, we would dismiss historical analogs like this if the recent market peak did not feature the “full catastrophe” of textbook speculative features – particularly the same syndrome of extreme overvalued, overbought, overbullish, rising-yield conditions observed (prior to the past year) only at major market peaks in 2007, 2000, 1987, 1972, and 1929. The main temptation to ignore this concern is that similarly extreme conditions emerged in both February and May 2013 without consequence. Less extreme variants of this syndrome have also emerged periodically in the past few years (these variants also capture 1937 and a few other bull market peaks, as well as the April 2011 peak after which the market briefly retreated by nearly 20%). Overall, my view continues to be that the consequences of the more recent instances have not been avoided, but merely deferred – and those consequences will be worse for it.

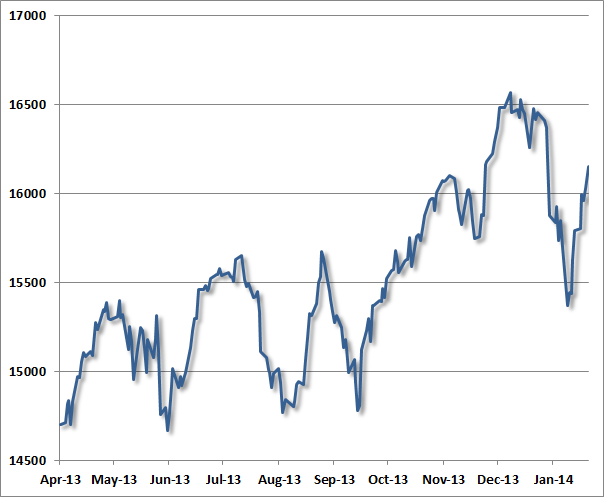

To offer some perspective of how major peaks have typically evolved, the following charts present the Dow Jones Industrial Average in the final advances toward, and the few weeks after, what turned out in hindsight to be major stock market peaks. For reference, let’s examine the recent market peak. Notice several features:

1. A series of moderately spaced peaks forming a broad sideways “consolidation” over several months;

2. A breakout from that consolidation, leading to a steep and only briefly corrected speculative blowoff into the market’s peak;

3. A steep initial selloff from the market peak, and finally;

4. A “reflex” rally (classically on low volume – indicative of a short-squeeze with sellers backing off) that retraces much of the initial selloff.

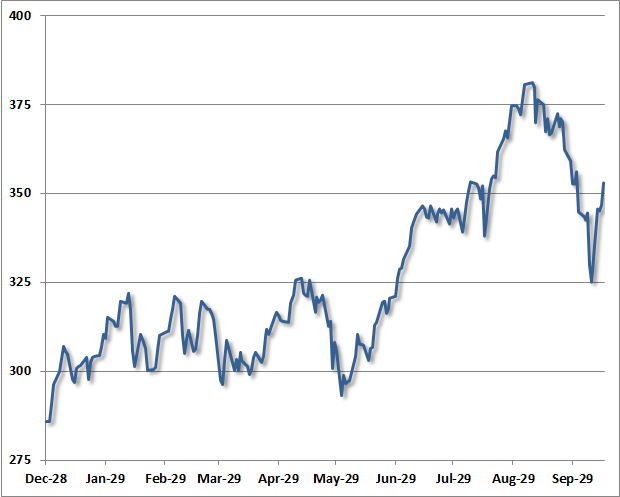

One can observe that same general dynamic in the chart below – a series of moderately-spaced peaks forming a largely sideways consolidation, a breakout to a steep and only briefly corrected speculative “blowoff”, an initial retreat, and finally a reflex rally. This chart depicts the final advance to the 1929 market peak.

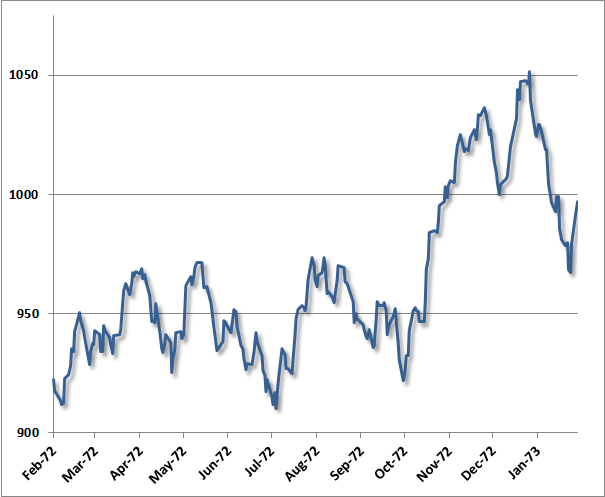

Largely the same dynamic was evident in the advance to the 1973 peak (after which the market lost half its value into late-1974): a series of moderately-spaced peaks comprising a broad consolidation, a breakout to a steep and only briefly corrected speculative blowoff and market peak, a steep initial decline, and a short-lived reflex rally after the peak.

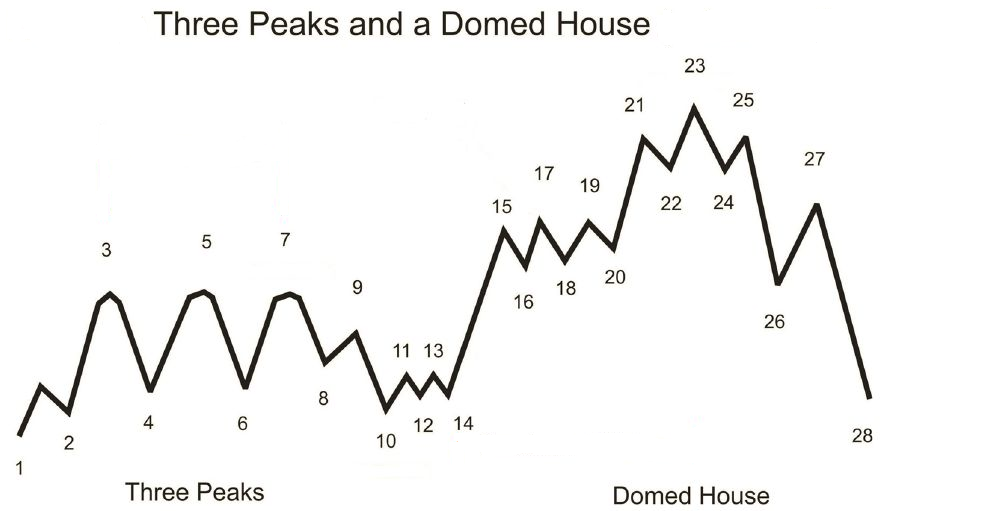

As it happens, the sequence described here is not at all new. Instead, it follows a pattern that technical analyst George Lindsay described in 1970 (and notably before even the 1973 instance above), which he called “Three Peaks and a Domed House.” Lindsay observed this pattern repeatedly across historical market cycles, describing about half of the bull market tops in the DJIA.

My sense is that it is enormously ambitious to label 28 separate points in a technical pattern, but the central observations do appear to nicely characterize many historical instances. Lindsay called points 8-10 a “separating decline” that distinguishes the series of consolidating peaks from first vertical portion of the speculative blowoff (the “wall of the first story”). Following a choppy correction, the pattern completes with the “domed house” – which is roughly the analog of a narrow head-and-shoulders pattern: “after peaking at 25, price tumbles to 26, retraces to 27, before heading lower to 28, completing the pattern.”

(chart and background h/t Claasen Research, James Goode, Thomas Bulkowski)

Though the “separating decline” after the mid-1999 consolidation was quite deep, as was the initial decline from the January 2000 peak in the Dow Industrials, the same essential features were evident then as well. The correspondence isn’t nearly as pretty as in the present instance, or those of 1973 or 1929. It’s worth keeping in mind that despite a hard initial decline, many (though not all) historical bull market peaks include an “exhaustion rally” anywhere between 2-9 months after the market peak, which can carry prices within a few percent of the high. The problem is that there is too much variability to count on either their timing or extent.

From the standpoint of investor psychology, it seems understandable that the speculative enthusiasm and short-covering that contributes to bull market tops is fueled when the market “breaks out” after a period of consolidation (and what Lindsay called a “separating decline”). The blowoffs that followed – both recently and in the examples above – were accompanied by clear overvaluation on reliable measures, and also featured clearly defined overbought conditions and lopsided bullish sentiment.

I’ll say this yet again, because it’s a crucial point – we would have zero interest in historical analogs like this if the recent market peak was not also accompanied by an extreme overvalued, overbought, overbullish, rising-yield syndrome that – prior to the past year – has emerged only at major market peaks. As with the recent log-periodic bubble, the pattern itself should be simply be treated like an interesting experiment. Lindsay’s and Sornette’s observations are largely consistent in that Lindsay’s pattern is basically a slightly irregular refinement of the very end of a Sornette bubble. The “three peaks” of Lindsay’s pattern correspond to log-periodic oscillations, and the left side of the “domed house” is essentially a final blowoff and short squeeze featuring much shallower fluctuations approaching the high.

Without tracing through over a century of price data for every instance (including “setups” that did not follow through), we can’t say categorically that this pattern is always followed by market losses. What one can say is that when Lindsay’s pattern has beenaccompanied by rich valuations (say, a cyclically adjusted P/E over 18), the market has typically been at the cusp of a significant retreat. Those periods of rich valuations are easily identified, and the corresponding blowoff patterns emerge in 1901-02, 1906, 1929, 1937, 1961, 1966, 1969, 1972-73, 1987, 1998, 2000, and today. The 2007 peak had less fidelity to Lindsay’s pattern because the reflex rally in October slightly exceeded the July peak of that year. Of course, lopsided bullish sentiment – as we observed in December and January – further narrows the set and worsens the average outcome, as do razor-thin risk premiums on corporate debt, soaring margin debt, and severely overbought conditions following a largely-uncorrected multi-year market advance. It’s not any single pattern that concerns us here, but rather the entire syndrome of classic speculative features that accompanied the recent peak – in the words of Zorba the Greek, “the full catastrophe.”

In any event, our present investment outlook certainly doesn’t derive from or rely on such patterns, and are much more related to a broad ensemble of evidence that we can validate over a century of market data. As I’ve noted in numerous prior weekly comments, 1929, 1972-73, 1987, 2000, 2007, and recent market highs belong to a rather exclusive group of instances featuring a similarly extreme syndrome of overvaluation (based on normalized measures that are well-correlated with subsequent 7-10 year market returns, such as 10-year inflation-adjusted earnings, price/revenue, and market capitalization / GDP); overbought conditions (based on the extent and duration of price advances); strikingly overbullish sentiment (based on the proportion of advisory bulls versus bears over a period of weeks); and typically rising interest rates (for example, 10-year Treasury yields above their level of 6 months prior).

Market cycles often display regularities, but investors should never conclude that they follow precise rules… but QE provides a potetial catalyst to prove it’s not different this time…

The primary beneficiary of QE has been equity prices, where valuations are strenuously elevated. QE essentially robs the elderly and risk-averse of income, and encourages a speculative reach for yield. Importantly, one should not equate elevated stock prices with aggregate “wealth” (as higher current prices are associated with lower future returns, but little change in long-term cash flows or final purchasing power). Rather, the effect of QE is to give investors the illusion that they are wealthier than they really are. It is certainly possible for any individual investor to realize wealth from an overvalued security by selling it, but this requires another investor to buy that overvalued security. The wealth of the seller is obtained by redistributing that wealth from the buyer. The constant hope is to encourage a trickle-down effect on spending that, in any event, is unsupported by a century of economic evidence.

The risks of continuing the recent policy course have accelerated far beyond the potential for benefit. The Fed is right to wind it down, and as it does so, the FOMC should focus on addressing the potential fallout from speculative losses that to a large degree are now unavoidable. Ultimately, the U.S. economy will be best served by a return to capital markets that allocate scarce savings toward productive investment rather than speculative activity. The transition to that environment will pose its own cyclical challenges, but is well worth achieving if the U.S. economy is to escape the grip of what is now more than 15 years of Fed-enabled capital misallocation.

CLICK THE IMAGE BELOW TO READ OUR GUIDE ABOUT A POTENTIAL END DATE TO THE CURRENT BULL RUN…

Comments (0)