Hedge Funds Are Harmful for Long Term Investors

Over the long term it is possible for an investor to build a portfolio with a very low risk profile while still being able to enjoy the upside potential that derives from the effects of compounding. For that goal, the Modern Portfolio Theory is of good help, stating that all an investor must do is to allocate funds between the market portfolio and a safe asset (cash or bonds), depending on the degree of leverage that maximises his own utility function. Some investors are more risk-averse than others, depending on age, financial situation, and other conditions. The more risk-averse an investor is, the less the proportion of the market portfolio he will be willing to add to his portfolio. The less risk-averse, the greater that proportion, to the point of borrowing funds if necessary. Thus, the choice of an equities portfolio doesn’t depend on individual preferences but follows a technique aimed at reducing risk for a certain level of expected return. The idea is to diversify such that non-systematic risk is completely eliminated. At that point an investor’s compensation is a linear function of the systematic risk he incurs, which is summarised by beta. By doubling its stake in the market portfolio, an investor would then get double the return at the lowest possible risk. That’s modern portfolio management, in Markowitz’s way.

But, of course, Markowitz theory is boring, in particular for those who make money from investing money from others’. If the best an investor can do is to allocate money between the market portfolio and a risk free asset, then all the industry can offer is just advice on the optimal allocation of funds between the market and the risk free asset.

Then come the hedge funds, offering the so-called alpha, which they sell as an extra compensation above beta. For the same risk, they claim being able of getting an extra return. If that’s the case, that extra should be attributed to the manager’s skills and then very well justifying the 2-20 fee structure they usually charge.

Fat Tails Come as Fat Losses

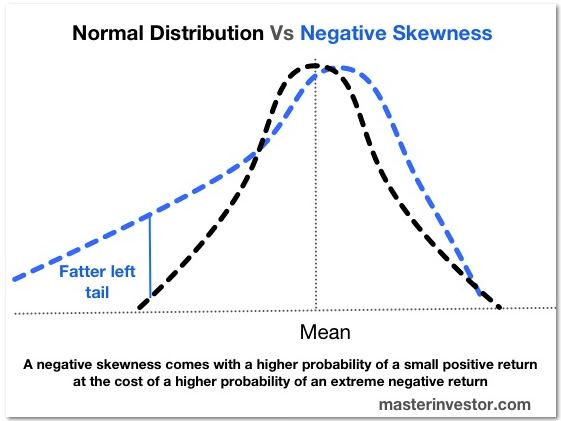

But in order to get a clear picture about the outperformance of hedge funds, we first need to correctly measure their risk-adjusted performance. With that goal in mind, investors usually use the Sharpe ratio, which measures reward per unit of risk. In theory the reward per unit of risk is a good metric to translate returns coming from a diversity of investments to the same unit, but in practice it fails on that goal, because it measures risk with standard deviation, a measure that assumes a normal distribution of returns. The normal distribution of returns requires an equal likelihood for positive and negative returns and no fat tails. But returns do have fat tails and are skewed, meaning there is kurtosis and skewness present. Under that scenario, the Sharpe ratio is clearly not enough to rank portfolios.

In the case of hedge funds, the problem is even worse because they are intentionally skewed. Hedge funds usually show a negative skewness, which means they have an increased likelihood of experiencing small positive returns, which comes at the cost of infrequent but large negative returns. At the same time their performance usually shows extreme kurtosis, meaning that the probability of extreme returns is much higher than predicted by a normal distribution. Under such conditions, the standard deviation underestimates risk. While an extreme negative return doesn’t occur often, it will tend to be more extreme than first predicted. This is exactly what a long-term investor wants to avoid.

A simple football betting example helps understand what happens within a hedge fund. Let’s say you follow a betting strategy of backing the favourite teams, which the bookmakers price between 1/15 and 1/10 for each £1 stake. These favourite teams will win their respective games most of the time, and you will accumulate small but frequent positive returns. But, at the reverse lies the infrequent outcome that sometimes happens, even though infrequently. When the favourites lose, you will experience a large drawdown in your returns. Unlike what happens in a coin tossing game, where the distribution of outcomes is normal, this favourite-backing strategy is negatively skewed. The standard deviation overestimates the risk of a positive return and underestimates the risk of a negative result.

Valeant Pharmaceuticals

Because no one would pay a hedge fund for achieving the same kind of returns that could be obtained by passively investing in the market; hedge funds engage in riskier strategies that deliver an extra return. Most of the time, the extra return is achieved by increasing leverage and exposure to non-systematic risk. But, when they experience large declines, we end realising that many of these bets on non-systematic risk not only are unable to deliver alpha but they even deliver less than beta.

Since the first quarter of this year, Bill Ackman from Pershing Square has been accumulating a position in the biotech firm Valeant Pharmaceuticals. At the end of quarter two, when the hedge fund had to report its holdings, it had accumulated almost 20 million shares in the company, which corresponded to 29.9% of the hedge fund portfolio. Ackman usually establishes a large position in a company in order to then force management to act in his best interests, but the specific risk that comes from such a position is often too large. Such risk will remain unnoticeable most of the time, contributing to enhance what seems to be a real alpha compensation for the portfolio manager’s skills. But later we just perceive it isn’t.

Valeant is a company that lives from its ability to acquire other companies and make deals for specific drugs rather than from its ability from growing internally. In summary, the company acquires undervalued medicines and then violently pushes up its prices overnight. When Hilary Clinton tweeted her plans to put an end on excessively high pricing in the specialty drug industry, the price of Valeant shares declined. Soon after, Democratic members of the House of Representatives Committee of Oversight and Government Reforms forced Valeant to explain its policy to increase the prices of two drugs by 212% and 525%. Shares crashed.

The biotech sector is heavily sensitive to investor sentiment. When central banks flood the market with liquidity, money tends to flow heavily in the direction of these stocks. One reason for that to happen is because these companies are difficult to value and then when sentiment is high, investors tend to foresee very shiny prospects for them, allowing for high P/E ratios and other high valuation metrics. But then, when the central bank contracts its policy (or just plans to contract it), sentiment declines and the price of biotech comes down to Earth. This later movement started in August. Valeant peaked at $262.52 on August 5 just to race downhill towards the $163.46, a 37.7% decline. Bill Ackman’s Pershing Square is heavily exposed to the stock and has lost $1.1 billion since June 30. Jeff Abbey’s ValueAct Capital is another victim of itself having lost more than $800 million in the same period, due to a 17.5% allocation to the shares. Other hedge funds like John Paulson’s Paulson & Co and Steve Mandel’s Lone Pine Capital also suffered heavy losses.

Hedge funds seem to drive alpha to investors much because of the idiosyncratic risk they incur and of the negative skewness and positive kurtosis their portfolios follow. Their stakes seem to carry much less risk than they really carry, until the point where the whole market declines and investors perceive the dimension of risk incurred. While the short term appeal these funds may offer is huge, long term investors are better by avoiding them because for these investors what matters the most is the power of compounding and not an exposure to diversifiable risk and leverage.

Comments (0)