Fund Manager in Focus – Hugh Hendry

Featured in this month’s Master Investor Magazine.

“The contrary investor is every human when he resigns momentarily from the herd and thinks for himself.”

– Archibald MacLeish

The Last Bear Standing

“Remember the film The Matrix? Morpheus offered Neo the choice of two pills – blue, to forget about the Matrix and continue to live in the world of illusion, or red, to live in the painful world of reality… They, as the “enlightened”, chose red, and so are convinced that they understand everything, which has become illusory about today’s markets. Their truth is Austrian economics. They know that today’s central bankers are spinning a falsehood of recovery; they steadfastly refuse to be suckered in by the euphoria of a monetary boom; and they are convinced that they will therefore be spared the consequences of the inevitable crash. Everyone else, currently drugged by the virtual simulation of prosperity and its acolyte QE, will be destroyed, leaving them alone, to re-invest when markets finally get cheap. They will once again be masters of the universe.”

– Hugh Hendry

As a strongly committed ruthless value seeker and a self-labelled “troublemaker”, Hugh Hendry could not take a pill other than red, just like the enlightened from The Matrix. As a fund manager, he is one of the last standing, still willing to take the painful direction of being right alone instead of going wrong with the herd. Hendry believes that the market often deviates from rationality, as investors are too enthusiastic about their options, and are then heavily influenced by a market wide mood – sentiment – that guides them into detaching asset prices from intrinsic values. He doesn’t hesitate to oppose this mood and sell what others are purchasing. Such contrarian strategies earned him a fortune during the financial crisis when he bet on the collapse of Greece and the banking system. But going the contrarian route of betting against the current order has also earned him fierce critics, as policy makers always believe the main reason behind a financial collapse mostly resides in the actions taken by the devil – i.e. contrarian hedge funds like Hendry’s – and, of course, not in the unsustainable business they usually like to keep.

Buying just for the sake of it while disregarding any fundamental value, in the hope someone will come along later and buy the same at a greater price was never in Hendry’s veins. On the contrary, Hendry seeks out opportunities arising from the sentiment-driven disconnects between fundamental value and nominal price to make his bets. In his view, that is the only way to drive value in an investment over the longer-term and to minimise the risk taken. In 2008, Hendry achieved a 31% return, while most of the fund management industry just struggled to survive, such was the blood bath taken.

Always being critical of the fictional optimism created by central bank intervention and by too much credit creation, Hendry has more often been on the bearish side than on the bullish side. At a time central bank intervention is uncapped, everyone in the market seems like a “fool” waiting for a “greater fool” to buy assets from them at even more “foolish” prices. Everyone, that is, but Hugh Hendry, “the last bear standing”. But, can someone resist the temptation of selling to a greater fool when central banks are protecting against the downside? For how long can someone oppose the irrational upside? Wouldn’t it be better to just join the herd and follow the trend?

From Chronic Troublemaker to Sagacious Fund Manager

Hugh Hendry was born in Glasgow, Scotland, in 1969 and graduated from Strathclyde University in 1990 with a BA in economics and finance. Curiously, he was the first in his family to attend university (and also one of only a few from his school). After graduating, Hendry found a job in Edinburgh at the prestigious investment firm Baillie Gifford. At that time, he was the first non-Oxbridge graduate to enter the firm. Soon, he started causing trouble and ended up moving to the City where he joined Credit Suisse Asset Management. Eventually frustrated by the fact he was just one of 400 other traders planted in the company’s floor, he tried to make his voice heard. But that was unwelcome and he was fired within a month. Nothing better could have happened to him, as the reputation as a troublemaker quickly seduced Crispin Odey from Odey Asset Management, who was seeking a talented someone able to think by himself. In 1999, Hendry was hired by Odey Asset Management and started a successful career that culminated with the creation of Eclectica Asset Management.

Opposing the existing state of affairs is never easy. A person who resigns from the herd and thinks for himself is many times labelled as a troublemaker and is most likely taking the thorny route enlightened by the red pill. But that was exactly the route that led Hendry to brilliance and which led his fund to $1.5 billion in assets under management. With Hendry on board, Odey created the Eclectica fund in 2002. The idea was one of maximising the long-term wealth of investors by opposing irrational pricing. The fund was very successful and in 2005, Hendry and Simon Batten, a colleague at Odey, purchased the management contract of the fund and founded Eclectica Asset Management, which is now independent from Odey.

Today, Hendry manages Eclectica in the Whiteleys Shopping Centre in Bayswater and without maintaining any correspondence with investment bankers or other industry professionals. Unlike many others in the industry, he starts working only at 10 am after a school run and a visit to the local coffee shop. He lives nearby in Notting Hill, but he travels to the countryside at weekends with his wife and three kids in a second-hand Land Rover Discovery.

Stars Don’t Shine Indefinitely

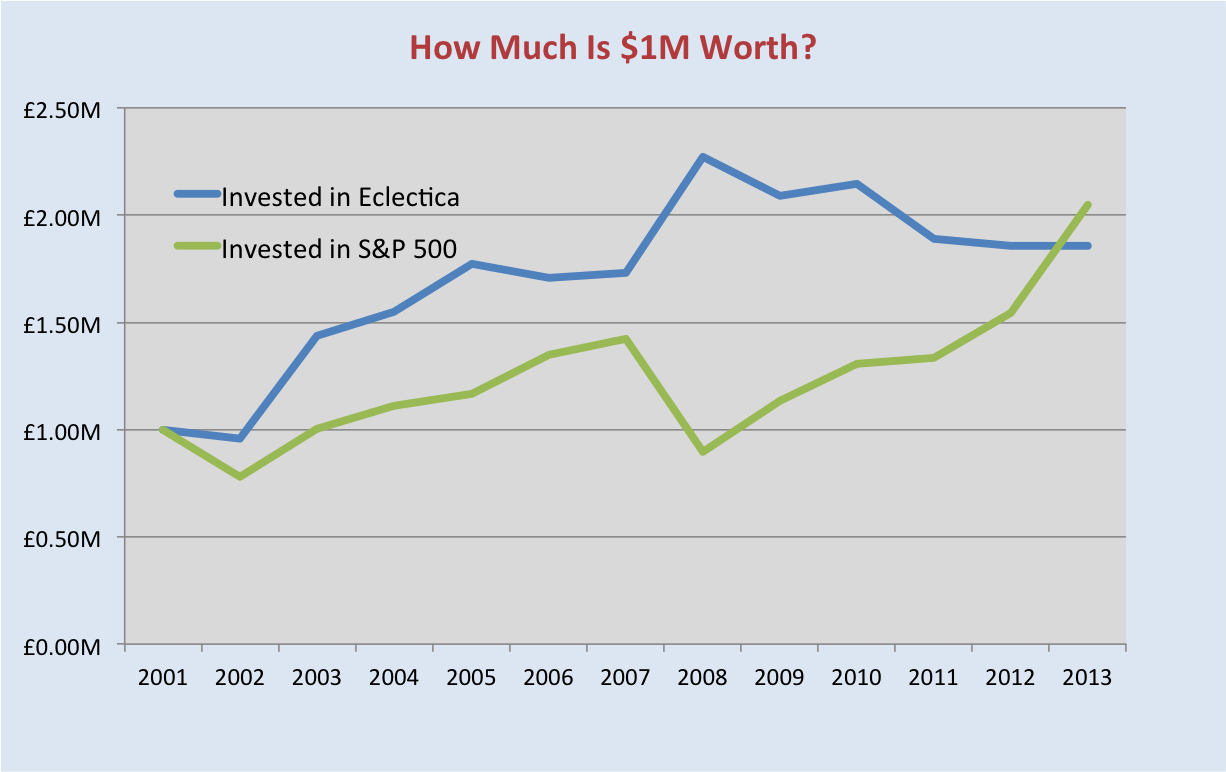

Eclectica was always very effective at managing the risk-return relationship but faced some muddy waters when central banks engaged in massive bold policy action to recover from the financial crisis. With interest rates being kept near zero for too long and massive asset purchase programmes being unfolded by central banks, the game changed dramatically. Such policies are detrimental for the contrarian strategies adopted by Eclectica and prevent professional traders from driving markets towards fundamental value again. The fund performed very well during market downturns, outpacing almost every other hedge fund, but completely struggled in 2012 and 2013, when everyone else, spurred by central bank action, was doing great.

Of course, the large profits everyone achieved in those years were generated by central bank intervention rather than skill. The massive leverage taken on by many would just expose them to bankruptcy had the central bank cut back its support and allowed for fundamentals to prevail. So, to a large extent there was no magic there. But even though fund management is about delivering long-term profits while minimising unnecessary risks, there is always pressure for short-term performance, as investors have limited patience, particularly when they see almost any other naive strategy ending the year with two-digit returns. After getting weary of fighting the irrational market, Hendry decided to let the “last bear standing” rest in peace. In a newsletter to investors, Hendry explained:

“There are times when an investor has no choice but to behave as though he believes in things that don’t necessarily exist. For us, that means being willing to be long risk assets in the full knowledge of two things: that those assets may have no qualitative support; and second, that this is all going to end painfully. The good news is that mankind clearly has the ability to suspend rational judgment long and often.”

“I’m Taking the Blue Pill Now”

Getting a share of the easy profits that were lying around was too large a temptation to be missed. Not even the most rampant and fierce opponent of the bull market could survive the long bullish run to tell the story. Hendry was no exception and replaced the red pill with the blue. It is certainly with a bitter taste that he now advises investors to “just be long, pretty much anything” as “only a foolish investor would stand in the way of this bull market”. Perhaps he is right. But it is exactly because not even hedge funds oppose such irrational behaviour that it persists for longer than before, which results in a growing systemic risk that can only end in disaster. On one hand, it is foolish to oppose the market, but on the other, why would anyone pay a 2-20 fee for professional services when one can just purchase a passively managed ETF on the S&P 500 for a fraction of the cost?

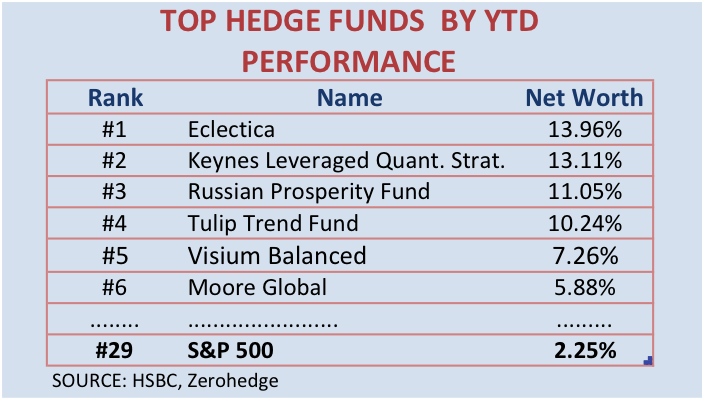

Since changing strategies from contrarian to momentum (trend following), Hendry has boosted Eclectica’s performance. While it struggled to outperform the market in 2013 and most of 2014, the fund then experienced a quick reversion and ended 2014 with a return of 8%. So far in 2015, the fund is up almost 14%, as the conversion of Eclectica from a bearish to a bullish outlook is starting to pay off.

Hendry is an admirer of Kindleberger’s book “Manias, Panics and Crashes”, which depicts how the global economy has been heading from crisis to crisis, fuelled by too much credit expansion and irrational behaviour. But Hendry also admits that the book has been detrimental to his investment performance. Realising a price is wrongly formed is no longer reason to sell or even avoid purchasing an asset, as there may exist a “greater fool” who is willing to purchase it at an even higher price. To justify his options, Hendry additionally claims that Eclectica’s performance has improved substantially since changing strategies. With Eclectica already up 14% this year, such a comment is hard to challenge. But he is now incurring the risk of a systemic crisis and is not particularly offering much more to an investor than one could get from a leveraged passive ETF.

Rather than theorising on markets, Kindleberger adopts a very practical approach. He shows the history of the real world as it happened. He clearly shows how central banks and credit expansion have been contributing to the boom and bust economy and how a period of irrationality is always reversed by a violent return to fundamentals. Only those who take the red pill can survive in the long-term. It is exactly because everyone is betting on the “greater fool” theory that a crisis is going to occur, as such a system is no less than a Ponzi scheme, which is condemned to fail from the beginning. Some are seduced by the uptrend; others, while recognising its irrationality, still believe they can get out before everybody else does. But history tells us that when you realise a crash is about to occur it is probably already too late, because at that point, markets have already returned to rationality.

Sadly, Hendry has just adopted a long-term losing strategy, even if that can bring some positive performance from time to time in the short-term. Eclectica’s assets under management have fallen from more than $1.5 billion to the current $300 million today, as its core investors don’t see the long-term alpha anymore.

Some Final Words

The man who once disturbed Nobel-Prize winner Joseph Stiglitz with a challenging “Um hello? Can I tell you about the real world?” continues to believe the world is going to crash despite having taken the blue pill for now. He believes that financial markets are single-digit years away from a crash that will present investors with opportunities of a lifetime. “Bad things are going to happen and I still think the closest analogy is the 1930s”, he says. So, it seems, the blue pill Hendry has taken was just a small dose after all.

Comments (0)