What Are The Prospects For UK Equity Income Funds?

It has been a volatile few months to be invested in the UK equity income sector, with the latest setback being the risk of a banking crisis following the collapse of Silicon Valley Bank. On a longer term perspective the picture looks more encouraging, as over five years these dividend paying companies have clearly outperformed the broader FTSE 100 index of blue chip stocks.

There are lots of different types of open-ended funds operating in the sector and this is reflected in the wide dispersion of the performance and yields. Over the last 12 months the 81 constituents have generated returns of anything from -14.9% to 5.5% with the yields ranging from seven percent down to a little under two percent.

The performance from the 21 equivalent investment trusts has also varied considerably with the 12-month share price returns ranging from 10% down to -11%. The average yield is a decent 4.6% and the average discount for the sector as a whole is currently 3.5%.

Ryan Hughes, head of active portfolios at AJ Bell, says that the UK market has a strong culture of dividends and this is reflected by it being one of the highest yielding developed economies in the world.

“The index yields around 3.5% with UK companies paying out about £78bn in dividends to investors during 2022, but what’s encouraging is the level of dividend cover that’s now in place, as this should provide a cushion to pay-outs should the economy weaken and go into a recession.”

Dividend cover has reached its highest level for a decade as companies have looked to improve their balance sheets, particularly during Covid when many of them cut their pay-outs significantly. This more prudent approach should reassure investors that dividends can be maintained during tougher times, which is important for anyone relying on the income.

Retail investors have been ditching UK equity funds in their droves because of the pessimistic forecasts for the domestic economy, but many professional investors have become more upbeat on the prospects due to a combination of low valuations and attractive yields.

Jason Hollands, MD of Bestinvest, says that the valuations reflect a lot of doom and gloom, which makes UK equities compellingly cheap both compared to their longer-term trend and the rest of the world, where the discount UK shares are trading at is at its widest level in decades.

“Blue chip UK shares are trading at prices of 10.6 times their forecast earnings for the next 12-months. This compares to global equities, which are trading on a price/earnings ratio of 15.9 times. While UK shares trade at a hefty 33% discount compared to global equities, the market offers investors a circa four percent yield, which is attractive compared to global equities (2.3% yield) and also higher than that on UK government bonds (3.4% on 10-year gilts).”

Prospects for UK equity income

Rob Morgan, spokesperson and chief analyst at Charles Stanley, says that the prospects for UK equity income are bright given the undemanding valuations and resilient balance sheets, especially among larger businesses.

“Many of the UK’s heavyweight companies are largely unrelated to the domestic economy. Instead, energy and commodity powerhouses, global banks and pharmaceutical giants ply their trade on the international stage. Overall, around three quarters of FTSE 100 earnings are from overseas.”

These old economy sectors are now back in vogue having had a sustained period in the investment wilderness when growth dominated. The transition to an environment of significantly higher inflation has shifted investor focus to industries and companies that can withstand an era of rising prices and resource constraints.

Morgan says that the precise make-up of a fund is very important, as those that are more oriented towards small and mid-cap will generally have their fortunes dictated by the health of the UK economy, whereas the ones concentrating on the largest firms will be driven by more global trends.

“Going forward, we think UK equity income remains a solid allocation,” explains Darius McDermott, MD of Chelsea Financial Services. “Dividend yields are good and starting valuations in the UK remain low.”

One of the main risks would be a full blown global recession. This would have a potentially significant impact as energy, mining and financial stocks, which all feature heavily in many large cap UK income funds, would suffer.

“It would be an issue for UK equity income as they are usually cyclically focused, which doesn’t do well in a recession,” explains Ben Yearsley, a director at Shore Financial Planning. “However, with a decent starting yield of three or four percent and dividends well covered at the underlying company level, as long as you can hold through any short recession then you should be fine.”

What to look for when choosing a fund

There are many different types of UK equity income fund with some focusing on large companies and others on the small cap end of the spectrum, while some target high yields and others growing yields. All of these approaches have their merits, but it’s vital to understand what you are investing in as the return profile of each will be different.

One of the key things is not to blindly go for the highest yield, as a few of them juice this up by using derivatives strategies, such as the Schroder Income Maximiser,which could hamper the capital growth potential. Other funds using a more traditional approach could potentially ‘overreach’ for yield, investing in companies with high dividends whose prospects are impaired by structural decline.

“You want to make sure you have a mix of styles as you can get small cap, large cap, more growth oriented and more traditional value,” says Yearsley. “Also watch out for the fees as they can vary greatly; there is a passive option in the form of the Vanguard FTSE UK Equity Income fund, so it is worth checking how the ones you choose stack up against that.”

One way to get a decent blend is to have a fund focused on larger businesses such as a cheap index tracker and combine it with a strategy that contains a broader mix. You could potentially factor in when the different funds pay their dividends so as to smooth out your income over the year.

“Some funds take a more quality based approach and accept a lower income from their holdings in the expectation it grows faster and leads to a superior total return, whereas others put themselves in the value camp or are more income targeted. These different strategies will deviate, possibly quite sharply, in terms of relative performance over given periods, especially short ones, so it is important to bear that in mind,” explains Morgan.

Historically, it has been a good idea to go down the market cap spectrum, where you can often find good yields alongside better dividend growth prospects. These types of funds have suffered recently, although if you can accept the greater risk they offer the better long-term potential.

Hughes says that another point to check is how diversified the portfolios are to ensure that they are not overly reliant on certain stocks to provide the income.

“In the UK, just ten companies pay over 50% of the total income generated by the market with the likes of Shell, Glencore, Rio Tinto, BAT and HSBC accounting for a significant amount of the dividends. Unfortunately the industries they operate in are cyclical so the pay-outs can fluctuate with the fortunes of the business.”

The best funds

When it comes to the individual selections Morgan recommends TB Evenlode Income, which aims to provide investors with a decent, growing income as well as some capital growth on top.

“They focus on what they call ‘cash compounders’, companies that are able to generate high returns on their investments without the need for debt. The right businesses of this type can consistently recycle profits into future growth and roll up exceptional returns over time, leading to decent results for shareholders.”

This type of good-quality, global leading company can be expensive to buy, but the managers believe it is often worth paying a higher price for stable businesses whose increasing profits can be forecasted relatively easily. As a result, the fund has a fairly low starting yield of 2.7%, but could increase pay-outs more quickly than others over time.

Morgan and Yearsley both like JOHCM UK Equity Income that aims to generate a dividend yield above the FTSE All-Share index through a strict yield discipline.

“Clive Beagles has co-managed the fund alongside James Lowen since inception in 2004, which is the sort of longevity rarely seen in modern day fund management. The two of them seek to invest in fundamentally strong companies at an attractive price and relatively high starting yields,” explains Morgan.

Their approach naturally promotes a contrarian style that backs out-of-favour, less expensive stocks. The fund will typically blend exposure to large multinationals with small and medium-sized companies, often giving it a different profile compared to many other income funds and the broader index.

Another option suggested by Yearsley is Ninety one UK Equity Income, which he says is a newer offering but is proving its mettle already with its quality value strategy. It is up 30% over the last five years and is yielding just over two percent.

Other fund options

If you would prefer a passively managed alternative there is the iShares UK Dividend UCITS ETF that is recommended by Morgan. It tracks an index of up to 50 constituents from within the FTSE 350, which are weighted by their one-year forecast dividend yields.

The main risk to be aware of is that it can be concentrated in terms of sectors and individual company exposure. Also, with the focus purely on yield, the potential capital growth is likely to be constrained, although it has a high 12-month trailing yield of six percent.

Hollands highlights the BlackRock UK Income fund, which is primarily invested in large, dividend generating UK companies, such as AstraZeneca, Shell and RELX. It has an historic yield of just over four percent with quarterly distributions.

McDermott prefers IFSL Marlborough Multi-Cap Income, which he describes as a well-resourced fund that offers something radically different from the majority of large-cap FTSE 100 income funds.

“This well-structured and highly experienced team will likely continue to take advantage of small-cap opportunities, which other managers and brokers often ignore.”

Alternatively he suggests LF Montanaro UK Income that is run by small cap specialists. It has an excellent research process and although it has struggled in the last year as small caps have gone out of favour, it has a good long-term track record.

Hughes also likes it and says that founder Charles Montanaro has built one of the largest independent small cap teams in the market with Guido Dacie-Lombardo now taking the lead manager role.

“Smaller companies were very much out of favour during 2022 and therefore the fund underperformed the market significantly, but used alongside a more traditional equity income fund, it has the potential to offer both income and capital growth. The portfolio currently yields close to four percent per annum.”

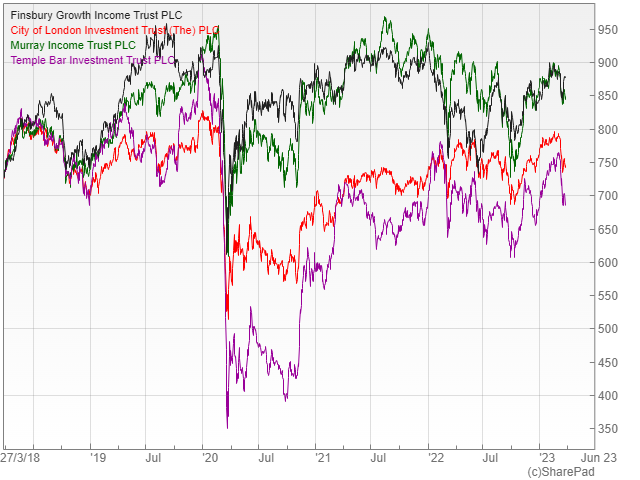

Investment trusts

There are some good investment trusts operating in this area, with Yearsley recommending Finsbury Growth & Income (LON: FGT). Manager Nick Train follows more of a growth focused strategy and as a result it offers a much lower yield of just two percent.

McDermott likes the City of London Investment Trust (LON: CTY), which invests predominantly in larger UK companies with international exposure. It has increased its dividend payment every year for the past 56 years and is very good value with a management fee of just 0.325% per annum of net assets under management.

Hughes is also a fan and says that it has been managed by Job Curtis since 1991 who has built up a strong track record. The trust is very much a core UK equity holding with large positions in the likes of BAT, BAE Systems, HSBC and BP. It currently yields nearly five percent with quarterly distributions.

Hollands suggests the Murray Income Trust (LON: MUT), which is celebrating its 100th birthday this year. It invests mainly in large and medium sized companies with attractive valuations and robust earnings potential, with the shares currently available at a discount to NAV of six percent.

Another of his recommendations is Temple Bar (LON: TMPL) that targets quality companies with strong balance sheets, with the portfolio containing a mixture of large and smaller/medium-sized companies.

“It has the flexibility to invest in selected overseas stocks too, with French oil giant Total Energies being one such example in the current top ten. Temple Bar has a high conviction portfolio of around thirty stocks with the manager adopting a buy-and-hold approach.”

Comments (0)