Taper tantrum two and the funds that can protect you

The US Federal Reserve and the Bank of England have both started openly talking about how they might scale back their bond buying programmes and raise interest rates to control inflation. They have done their best to signal that a change is coming, but when it happens there is still a real possibility of another taper tantrum.

The original taper tantrum occurred in 2013 when the Fed started winding down their purchases of bonds as they reduced the Quantitative Easing (QE) that had been introduced in response to the global financial crisis. It was triggered by the chair of the Fed at the time, Ben Bernanke, who inadvertently tipped off the markets about what they were planning to do during an appearance before congress.

Speaking to the Joint Economic Committee in May of that year he said: “If we see continued improvement and we have confidence that that’s going to be sustained then we could in the next few meetings … take a step down in our pace of purchases.”

The reaction was instantaneous with treasury yields rising, emerging market stocks falling because of the stronger dollar, junk bonds weakening and share prices becoming more volatile. It was this response that eventually became known as the taper tantrum and the consequences were so severe that it forced the Fed to delay their plans.

In the intervening eight years the tightening has of course been reversed and we have witnessed monetary and fiscal easing on a scale never seen before. Central bank balance sheets in the US, UK and elsewhere have ballooned and interest rates have been cut to historic lows, which makes the next shift in policy a potentially momentous event.

All eyes on the Fed

In the US, Fed officials are actively considering how to taper their monthly bond purchases as the economy recovers and inflation risks shift to the upside. There have been no firm announcements as to when that process will begin and what the pace will be, although there have been a few hints to get the market used to the idea.

The Fed has a dual mandate to achieve price stability and maximum sustainable employment. Recent strong jobs growth has prompted more hawkish comments from some of its members, but the key update came at the Jackson Hole summit at the end of August.

Speaking at the virtual event, Fed chair Jerome Powell said that the outlook for the labour market has brightened considerably over recent months and the rapid re-opening of the economy has brought a sharp increase in inflation. He is expecting continued progress towards maximum employment with inflation returning to levels consistent with their goal of an average of two percent.

Powell went on to say that if the economy evolves broadly as anticipated it could be appropriate to start reducing the pace of asset purchases later this year. Interest rates however will not be increased until the economy reaches conditions consistent with maximum employment and inflation has reached two percent and is on track to moderately exceed two percent for some time.

Darius McDermott, MD of Chelsea Financial Services, thinks there will be lots of hints from the Fed about what it is going to do so as to prepare the market before we actually get a formal announcement.

“It will probably announce tapering before the end of the year, with the process starting in 2022. There are some who argue that the Fed is already scaling back QE as is it starting to sell some of the bonds it owns and the ‘dot plots’ have moved markedly in recent months.”

Several central banks have already raised interest rates in response to rising inflation, notably Brazil, Russia and Mexico, while Australia, New Zealand and Canada have either stopped adding to QE or reduced the amount of stimulus they are applying.

Russ Mould, investment director at AJ Bell, says that if the Fed does finally pluck up the courage to tighten policy, markets seem to think that QE will be scaled down first with minor interest rate rises following in 2022 and 2023.

“It is hard to take seriously commentary that the prospect of two, one-quarter point interest rate rises by the end of 2023 represents hawkish policy as a base rate of 0.75% with the biggest balance sheet it has ever had would still represent an ultra-loose monetary stance, one that you could argue is not well-suited to a rip-roaring, post-pandemic recovery, if indeed that is what we get.”

The Bank of England drops some hints

The Bank of England has recently forecast that inflation will hit four percent at the end of this year, it will then fall to 3.3% in one year’s time and 2.1% the year after. These are all well above its two percent target, but it is sticking to its view that the increase will be transitory and that it will not need to raise interest rates any time soon.

When the time comes to reduce the stimulus it has said that it will start bynot reinvesting the proceeds of maturing bonds in the QE programme, but it won’t do this until the Bank Rate has risen to 0.5% from its current 0.1%. It won’t actually consider selling any bonds until the Bank Rate hits at least one percent.

McDermott says that the Bank of England has followed the Fed closely for years and he doesn’t expect it to be any different this time around with both starting to taper in 2022, possibly with the UK going first.

“I think the UK is less likely to raise interest rates before the US as inflation is not as high as in the States and the bank has already said it thinks it will be transitory. We will probably see a more gradual tapering in the coming months as growth comes through strongly, but rate rises will be later.”

Obviously it is important to unwind QE in a predictable and gradual manner to avoid undermining the economy and triggering a sell-off, but whenever it comes it could have a damaging impact on the bond market and the public finances. The reason that central banks are moving slowly is because they don’t know the outcome of the pandemic and how it will affect corporate and consumer behaviour over the long-term.

“There is now so much additional debt in the system compared to 2009 and the end of the financial crisis that even minor increases in borrowing costs could have a large impact on the interest bills and thus ability to spend of governments, corporations and consumers alike,” says Mould.

The government currently pays the Bank Rate of 0.1% on bonds held in the QE programme, so if interest rates rise while QE remains in place, the Treasury’s interest payments would skyrocket. According to the OBR, even a modest one percentage point rise would equate to £20.8 billion more in interest for the Exchequer in 2025/26.

UK households are currently paying £17.2bn annually in (floating rate) interest payments that are likely to be affected immediately by an increase in interest rates, including on variable-rate mortgages, credit card debt and other personal lending. If rates rose by just 0.25%, these annual interest payments would increase to £18.2 billion almost overnight.

Taper tantrum two?

The bond market is the place where it could all unravel. Bond prices have soared during the last 12 years due to the unprecedented level of buying by central banks, but there is a risk that it could all come to a nasty end when QE is unwound and interest rates rise, although nothing is certain.

Ben Yearsley, a director at Shore Financial Planning, does not think that the ending of QE will be taken that badly as with growth so strong and inflation picking up markets are expecting a central bank response.

“However, it will probably hit growth stocks in the short-term as markets panic about what increased rates will mean for the discounted cash flow (DCF) valuations. That could possibly create a buying opportunity in those sorts of companies as over the longer term I think we will return to a low growth environment.”

Any policy tightening will doubtless be well-flagged to markets, even if this shows that central banks have become prisoners of their own policies and attempts to create a wealth-effect through boosting asset prices.

“It is logical to expect some increase in volatility and perhaps a wobble or two, as bountiful liquidity is seen as one reason why so many asset classes have done so well for a decade or more. Yet US equities did well after the Fed put QE3 on hold, so you can never say never, although valuations now are much higher than they were then,” warns Mould.

To some extent we have already had a taper tantrum earlier in the year when US treasury yields rose and growth stocks got hit hard. That has reversed in recent months, which could be the bond market’s way of signalling that the recovery may not be as strong as some people think.

“There is also a widespread belief across markets that the Fed cannot taper for long or normalise rates as this would crash the economy. This is what I think the bond market is saying,” explains McDermott.

“If there is any sort of distress when the Fed tapers it will probably be forced to reverse course as it has done every single time it has attempted to normalise monetary policy since the global financial crisis, so the bond market is calling the Fed’s bluff.”

It could go either way

The problem if we get a taper tantrum is that most assets would fall, as bonds and income producing investments would suffer from the higher government bond yields, as would a large part of the equity market whose valuations would look more stretched on a DCF model.

Gold could also struggle if bond yields rise and the US dollar strengthens.

This makes it hard to hedge against, although a small number of areas could turn out to be safe havens such as inflation-linked bonds, banks and some of the out of favour deep-value stocks.

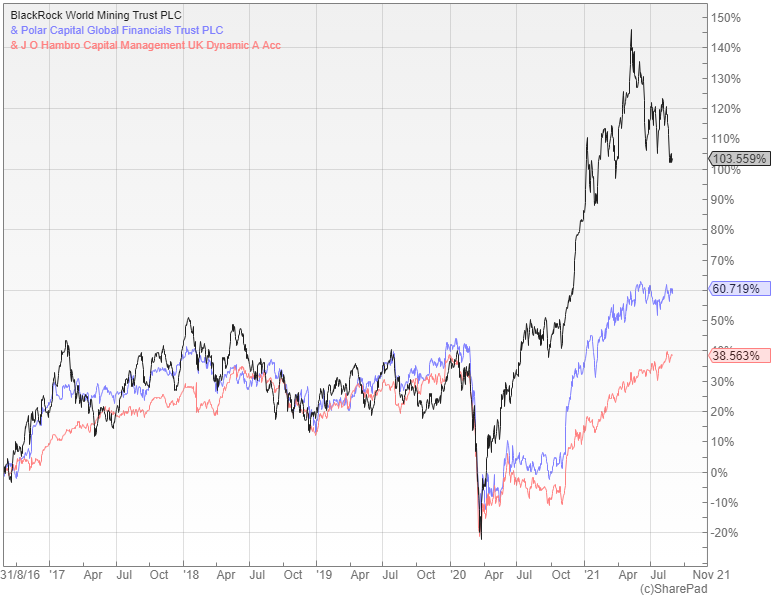

In this sort of scenario Yearsley suggests the Blackrock World Mining investment trust (LON: BRWM) that could do well in an inflationary environment; the Polar Capital Global Financial Trust (LON: PCFT), which holds banks and other financial companies that would benefit from higher interest rates and the value-oriented fund JO Hambro UK Dynamic.

If the markets and economy react badly it could force policy makers to reverse direction pretty quickly, in which case you would want to be invested in the same things that have worked well for the past decade such as technology and growth stocks.

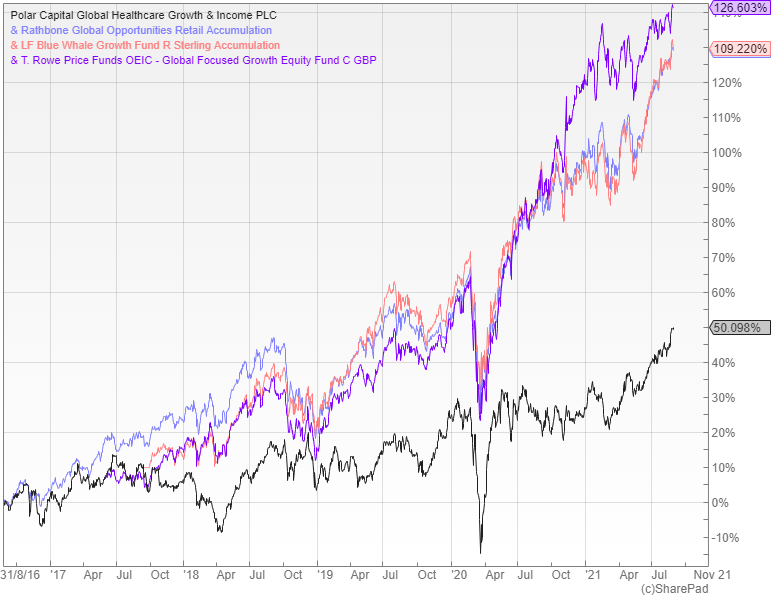

In this situation McDermott recommends funds such as Rathbone Global Opportunities, LF Blue Whale Growth and T. Rowe Price Global Focused Growth Equity,which all invest in growth stocks.

“Alternatively there is the Polar Capital Global Healthcare Trust (LON: PCGH) that is likely to sail through unaffected. Healthcare as a sector sits roughly in the middle ground and will probably not be impacted by Fed policy in the long-term. It is run by excellent stock pickers, meaning the prospects are likely to be driven by their skill, rather than macro forces,” he says.

Absolute return funds

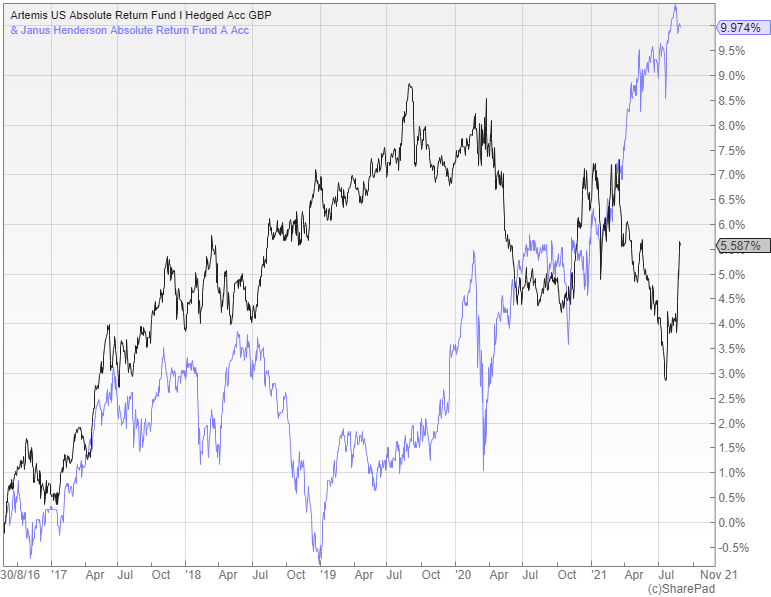

Morgan recommends Artemis US Absolute Return, a US equity long/short fund that aims to deliver a positive return over rolling three year periods.

“In an environment where just about everything is struggling, absolute return funds can come into their own. This particular one derives the majority of its returns from bottom up stock decisions on the long and short books, which means it can provide positive returns in falling markets.”

The majority of the funds in this sector have a poor record, but that is not the case for the Janus Henderson Absolute Return fund, which has been very consistent over a long period.

“This long/short equity fund has proved over numerous bouts of market volatility that it can protect capital and weather the storm, while most other absolute return funds struggle. Managers Ben Wallace and Luke Newman are very experienced and make good decisions in adjusting both the net and gross positions of the fund,” says Ryan Hughes, head of active portfolios at AJ Bell.

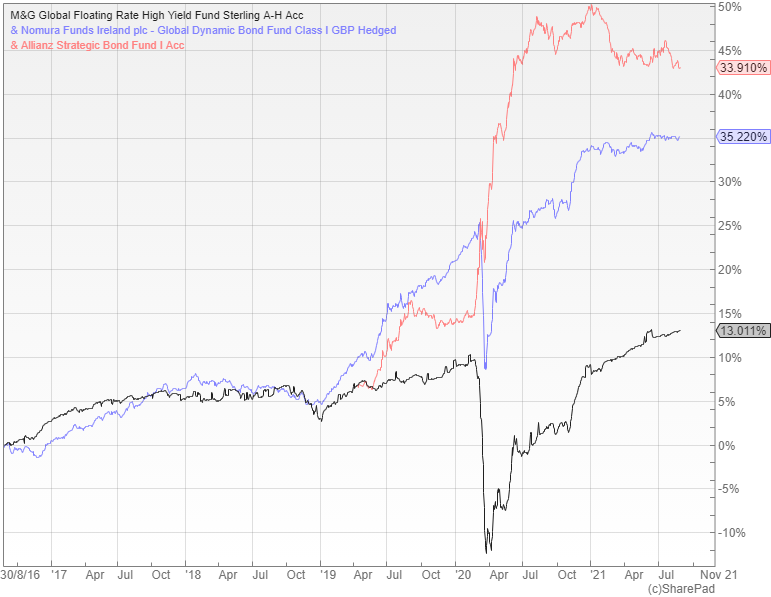

Most bond funds would lose money in this scenario, although those with low interest rate sensitivity or duration would be more resilient, with one possibility being M&G Global Floating Rate High Yield. This expands the floating rate note universe by creating synthetic versions of notes by combining credit default swaps with floating rate treasury bills and pays an attractive income of around four percent.

“Nomura Global Dynamic bond is another option for those looking for an allocation to bonds, but who want considerable flexibility and opportunism. Allianz Strategic Bond is similarly a potential vehicle, as manager Mike Riddell is very macro focused and able to offer plenty of protection, while taking advantage of market upside in extreme scenarios,” explains McDermott.

Defensive Stalwarts

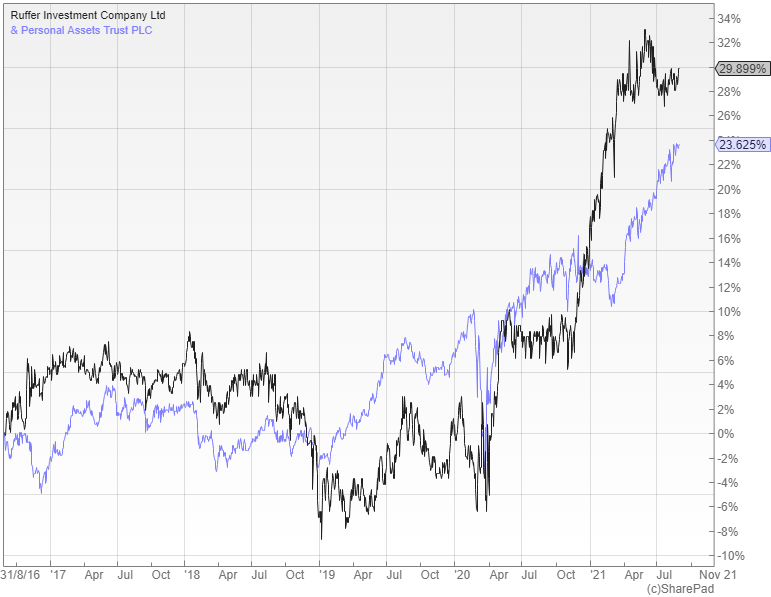

Another option from Morgan is the Ruffer Investment Trust (LON: RICA) that combines conventional asset classes including global equities, bonds, currencies and gold with the use of derivatives strategies that serve as protection in market downturns.

“The overall aim is to protect as well as grow your capital, so the balance of different assets is designed to pay off in a variety of economic scenarios and the managers have a great record of making shrewd macro-economic judgements. They are currently wary of inflation so have this risk firmly in mind,” he says.

Hughes suggests that an alternative could be the Personal Assets investment trust (LON: PNL) managed by Sebastian Lyon at Troy.

“The trust has over 10% exposure to gold with a further third of the portfolio in index linked bonds, giving strong inflation proofing to your investment. This is complemented with around 45% in high quality equities such as Microsoft, Nestle and Diageo, all of which have high barriers to entry and recurring cash flows that underpin decent dividends.”

It looks like the Fed and the Bank of England will both start to taper their bond buying programmes later this year or early next with interest rate rises coming in 2022 or 2023. Even after these changes monetary policy would still be ultra-loose, but if the market believed there was more to come it could easily be enough to trigger another taper tantrum.

Comments (0)