Invesco Bond Income Plus: Is a seven percent yield enough to go back to bonds?

Conventional bonds have been virtually untouchable for years − at one stage there were literally trillions of dollars of government debt with a negative yield − but that has all changed now with the sell-off due to rising interest rates making them worth a closer look.

One option at the riskier end of the spectrum is Invesco Bond Income Plus (LON: BIPS), which aims to achieve capital growth and high income from investing predominantly in European high yield debt. With the global economy on the verge of a potentially serious recession this would be a brave investment were it not for the fact that so much bad news has already been priced in.

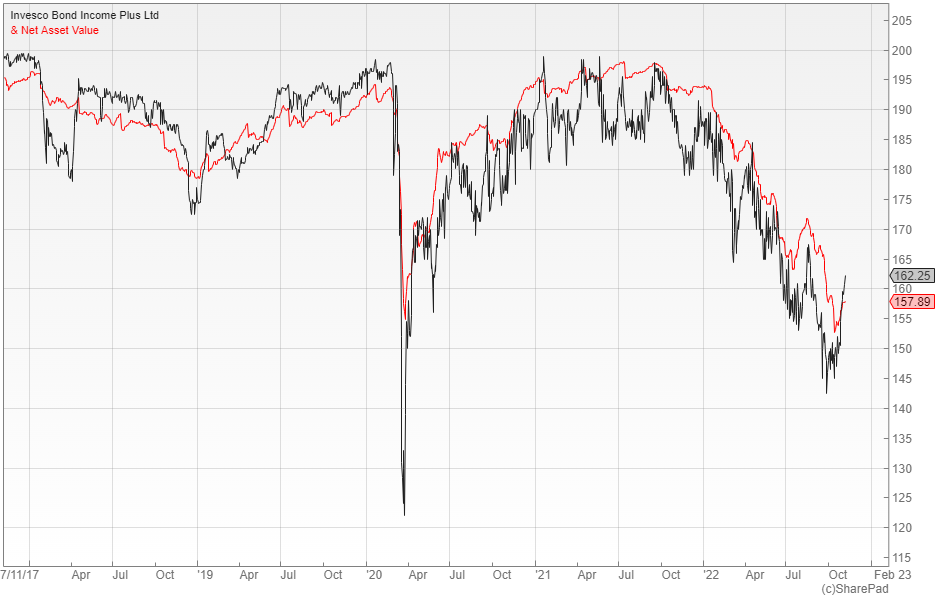

Average yields on the ICE BofA European High Yield index exceed eight percent with many of the securities trading on significant discounts to face value. The underlying BIPS portfolio currently offers an attractive 11% yield to maturity with the shares down around 14% in the last 12 months, so it’s perfectly possible that the trust is close to bottoming out.

Margin of safety

The £320m Invesco Bond Income Plus is the result of the May 2021 merger between City Merchants High Yield and Invesco Enhanced Income, which makes it the largest fund in the peer group with cost and liquidity advantages. Managers Rhys Davies and Edward Craven take a relatively risk averse approach compared to the rest of the sector.

BIPS has no exposure to structured products or leveraged loans, no significant unrated allocation and a 19% weighting to investment grade bonds, although the 18% gearing does add to the risk. In September the quarterly dividend was increased to 2.875 pence, which gives the fund a prospective yield of just over seven percent compared to a loans and bonds peer group average of 5.8%.

The broker Winterflood describe the yield as attractive and point out that the shares are currently trading close to NAV, a rating that they think can be maintained. They say that 2022 has been a challenging year to navigate, but they expect the trust to offer somewhat more stable and predictable returns going forward, relative to its peer group.

Portfolio approach

The managers use a bottom-up credit analysis approach with investments typically considered on a two or three year view, in terms of the issuer’s ability to afford structurally higher borrowing costs and withstand a tougher economic environment. Given the attractive yields across the board there is no need for them to focus on distressed credits and special situations, which would be highly risky in the light of the poor outlook.

At the start of 2022 the average yield on the ICE BofA European Currency High Yield index was 3.4%, but that has since risen to 8.8% as prices have collapsed, a level that has not been seen in the last decade. The managers are understandably cautious and expect the elevated yields to persist over the medium term, potentially impacting credit fundamentals.

They think that interest rates will continue to rise in the short-term, but believe that we are closer to the end of the hiking cycle than the beginning. Once inflation peaks, central banks may pivot to rate cuts to limit the economic damage, which could spark a major recovery in duration and risk markets with the fund being a major beneficiary.

Comments (0)