Inflation, interest rates and the investment trusts set to benefit

The key issue that is likely to dominate the markets this year is inflation and the degree to which policy makers are able to respond to it. Central banks in the US, UK and elsewhere have already taken their first tentative steps towards monetary tightening, but how far can they afford to go without derailing the economy and crashing the markets?

CPI inflation in the UK recently hit 5.4%, the highest this annual reading has been since the measure was introduced in 1997, with a further increase to six percent expected by the spring. This is way above the Bank of England’s two percent target and prompted the Monetary Policy Committee to increase interest rates from 0.1% to 0.25% in December.

The first hike only had a marginal impact on borrowing costs and the economy, but a second increase to 0.5% would be a lot more significant as that is the hurdle rate the bank has set for naturally reducing its £900bn holdings of government bonds as they mature. If they stop re-investing the proceeds in further purchases it would effectively reduce the stimulus still further.

As you would expect, the benchmark ten year UK gilt yield has risen sharply as a result of the change in policy and is up from 0.7% in early December to 1.25%. The FTSE 100 index is higher over the same period due to the preponderance of value stocks that tend to benefit when yields rise and the exposure to mining and energy companies that profit from increased commodity prices.

In the US the Fed is actively winding down its bond buying program and has suggested that they expect three separate interest rate rises of 25 basis points each this year. They have also said that they could reduce the size of their balance sheet, which would tighten conditions even more.

This is a much more aggressive stance than they had taken in the past, a move that was really forced on them when November’s US CPI data came in at a 39-year high of 6.8%. The benchmark US ten year government bond yield has shot up from less than 1.5% to 1.80% in response and the growth heavy NASDAQ has weakened.

December’s US CPI came in at an even higher seven percent and Fed chair Jerome Powell has said that the bank is likely to raise rates in March. It also plans to end its bond buying programme that same month.

Where are interest rates and inflation headed?

Mick Gilligan, portfolio manager at Killik & Co, says that market interest rate futures are pricing in 3.6% US inflation by the end of this year and UK inflation of around three percent, down from the current five percent. They are also pricing in a rise in US rates from 0.25% to one percent and in UK rates from 0.25% to 1.25%.

“My central view would be that this tightening and the year-on-year comparative effect will help to bring down inflation. Whether this will be smooth or not is difficult to say. The first week’s market action is often a guide to what lies ahead for the next 12 months, which suggests that it could be a choppy year.”

The independent commentator Adrian Lowcock says that it is clear that higher inflation is here and it is likely to remain for much of 2022.

“Some of the drivers of inflation last year were due to temporary base effects, but other inflationary pressures have been caused by supply chain disruption resulting in price rises. The pandemic is also a key factor, as the removal of restrictions and growing level of confidence could lead to stronger consumer spending.”

With central banks finally acknowledging that inflation looks like it will be hanging around longer than they initially thought, it seems inevitable that interest rates will increase this year.

“The Bank of England started the ball rolling at the end of 2021, arguably at least a month too late and seems certain to follow up with a number of increases as we move through the year,” explains Ryan Hughes, head of active portfolios at AJ Bell. “The Federal Reserve is also now making much more noise about rate rises in the US and the stopping of the additional monetary stimulus.”

Central banks have a difficult balancing act. They have used extraordinary monetary policy to get us through the pandemic, but they now have to try and reverse it without upsetting the economies and financial markets they are trying to sustain.

The warning signs

Rob Morgan, pensions & investments analyst at Charles Stanley, says that they will be watching out for any policy error such as hiking interest rates too far too soon, as if the Fed are going to be aggressive they will probably be aggressive early.

“We will also be studying inflation in case it embeds with a wage price spiral, upsetting the central bank forecasts. The danger of this happening is a bit higher than the risk of a policy error as it would be a surprise if the Fed or any of the other major central banks actually overdid the monetary tightening in panic.”

The main thing to watch is the labour market, which has struggled to get people back to work. On both sides of the Atlantic there are political pressures to raise pay for lower paid workers, while at the same time employers are finding it difficult to fill all the vacancies.

It is possible that the sharp rise in general inflation could lead to more successful pay claims thereby initiating a wage price spiral, although the more likely scenario is that workers will experience a cut in their real earnings as a temporary inflation surge hits spending power as people have to lay out more for the basics.

“Taking all of this into account, our central scenario is that equities will still be a reasonable place to be overall as many companies will have sufficient pricing power to offset inflationary effects on their costs,” says Morgan. “However, it will be a much tougher environment than what we have seen in the past year or so as liquidity is coming off the table and there is the possibility of slowing growth.”

The problem is that if inflation remains persistently high, central banks would struggle to raise interest rates enough to bring it back under control.

“The UK and America have got used to low interest rates; raising them to two or three percent would be a lot and would have a huge impact on consumer confidence and the ability of borrowers to finance their mortgages,” warns Lowcock. “Of course the flip side is that inflation also erodes consumer confidence and impacts household incomes, so the most likely outcome is that central backs will have to contain inflation even if it means damaging the economy.”

This is largely a problem of the authorities’ own making as investors have been conditioned into believing that every time there is a threat to the economy, the central banks will turn on the printing presses and come to the rescue. Ever since the global financial crisis over a decade ago the politicians have been terrified of any kind of economic hit, which has led to the current bull market in both equities and bonds.

Multi-asset trusts

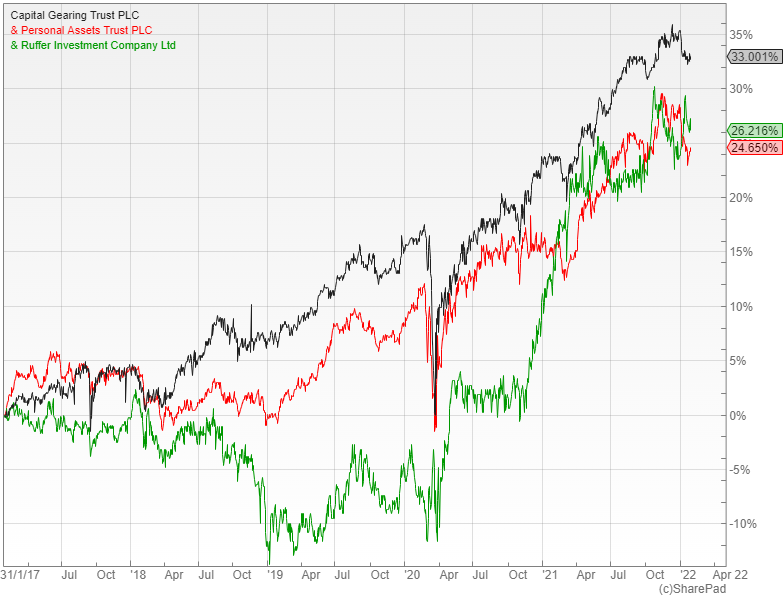

Gilligan says that in an environment of uncertainty, diversification is key, so he suggests two multi-asset absolute return trusts: Capital Gearing (LON: CGT) and Personal Assets (LON: PNL).

“Capital Gearing is diversified across short dated bonds, inflation linked bonds, infrastructure, equities and property. This defensive diversified positioning puts it in a good position to withstand any market gyrations in the year ahead.”

The broker Winterflood has included it as one of their recommendations for the year. They say that it has considerable merits, not just compared with some of its investment trust peers, but also with a range of vehicles that seek to provide investors with steady absolute returns over the long-term.

PNL is another that is on their list. They point out that under Sebastian Lyon’s management the fund has exhibited considerably lower volatility than the FTSE All Share and that it remains attractively positioned for investors who are looking for a defensive portfolio.

“Personal Assets is diversified across short dated bonds, inflation linked bonds, gold and high quality equities with pricing power. Again, this diversified positioning puts it in a good position to withstand any market gyrations in the year ahead,” explains Gilligan.

Hughes is also a fan and says that the economic scenario that Lyon has been worrying about seems to be coming to fruition.

“With jittery equity markets and fears over inflation remaining elevated for a considerable period, the defensive positioning of this trust and its exposure to inflation protecting assets such as gold and inflation linked bonds should sit well looking ahead.”

Morgan and Lowcock both prefer the Ruffer Investment Company (LON: RICA) that is designed to be an ‘all-weather’ vehicle with the overall aim to protect as well as grow investors’ money.

“The managers believe that we are witnessing the beginning of a new market dynamic where the key question has shifted from whether inflation is transitory to whether central banks have the ‘willingness and the ability to bring this lingering, sticky inflation back down.’ They suggest that the mounting pressure on authorities to dial back stimulus makes equity and credit markets vulnerable, so they have increased their allocation to protection strategies and reduced the equity component to just under 40%,” explains Morgan.

Value trusts

Gilligan says that as higher inflation is likely to have a more negative effect on portfolios than lower than expected inflation, it would make sense to hold a value biased equity fund that should do well in such a scenario.

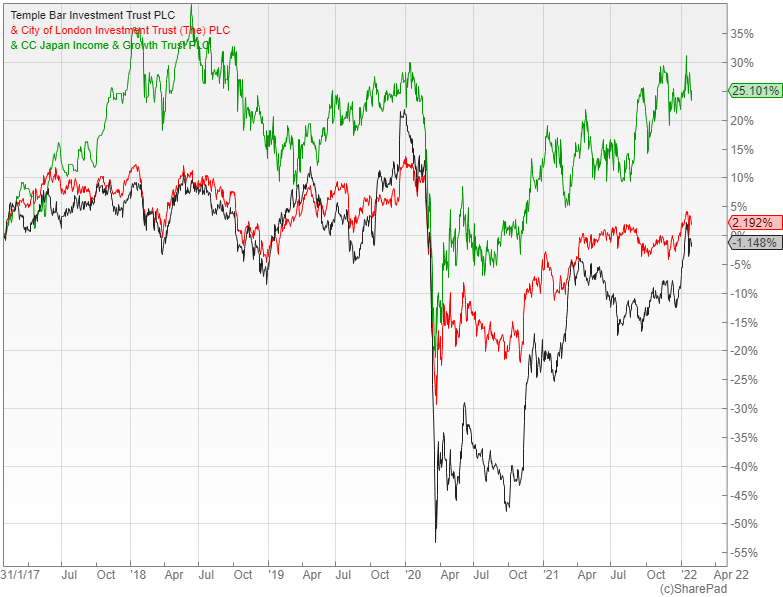

“Temple Bar (LON: TMPL) has a UK equity portfolio with a strong value bias. Value stocks typically outperform growth stocks in a rising rate environment and exposure to commodity stocks and financials should help to hedge any higher than expected inflation.”

Hughes is also a fan and points out that it is managed by the highly experienced team of Ian Lance and Nick Purves at RWC. The trust invests in classically out of favour UK companies that have a strong chance to recover and are financially sound, with large holdings in the likes of M&S, Royal Mail, Anglo American and Aviva.

Lowcock suggests the City of London Trust (LON: CTY), which mainly invests in UK equities and offers an attractive dividend yield that currently stands at 4.7%.

“It actively uses its revenue reserves to maintain the dividends and has now paid a rising dividend for the last 55 consecutive years. The trust has a defensive and value bias that has impacted the longer term performance, but should help it in a more inflationary environment.”

Hughes likes the Coupland Cardiff Japan Income & Growth investment trust (LON: CCJI) that is yielding three percent and actually managed to increase the dividend during the pandemic as the strength of Japanese companies came through.

“Japan has continued to be a shining example of how to manage company balance sheets in recent years with many corporations sitting on huge amounts of cash without the millstone of enormous debts. This is translating into strong dividend growth for investors in the country at a time when income feels like a scarce commodity. The trust offers a potentially growing income stream and diversification away from the traditional income companies.”

Other options

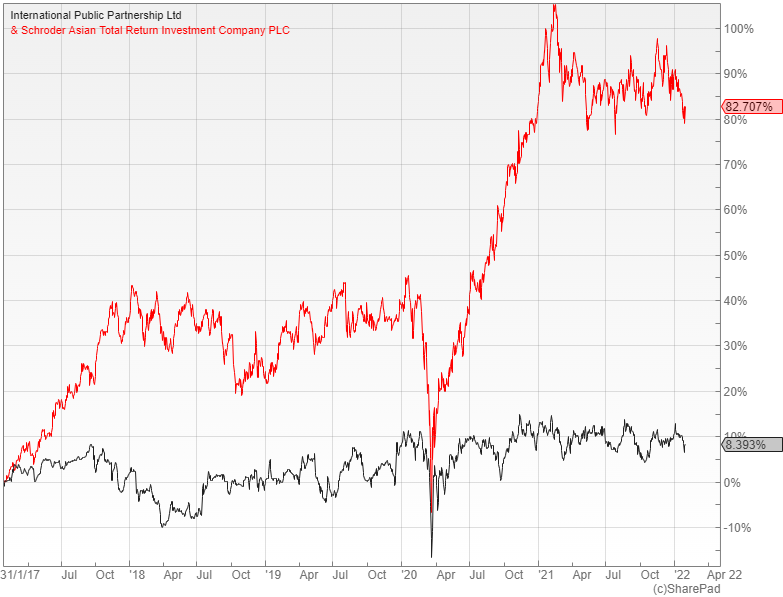

Morgan likes International Public Partnerships (LON: INPP), which invests directly and indirectly in public or social infrastructure located in the UK, Australia, Europe and the US. Its cash flows benefit from a high degree of inflation linkage and are long term in nature with a heavy weighting in regulated assets.

“Infrastructure should be resilient in a variety of scenarios including a more inflationary one. These sorts of assets provide a steady income and often have a certain amount of contractual inflation protection built in.”

Notable holdings include the Thames Tideway Tunnel, London’s ‘super sewer’, as well as the Diabolo Rail Link, which serves Brussels airport and has approximately 75% of revenues related to either the usage of the airport link or the wider rail system in Belgium.

Alternatively he suggests the Schroder Asian Total Return Trust (LON: ATR), which aims to achieve market-beating performance while offering a degree of capital preservation through the tactical use of derivatives. The region suffered from the more interventionist approach taken by the Chinese authorities in 2021, but there are some excellent longer term prospects in the area.

“Managers Robin Parbrook and King Fuei Lee currently have a modest direct allocation to China with higher weightings in Taiwan and Hong Kong. They are on the lookout for oversold stocks in areas less exposed to regulatory risk, warning that Chinese internet companies may become more like quasi-state owned enterprises similar to how certain banks and telecom stocks operate.”

Asia already accounts for half of the world’s economic activity, a proportion that looks likely to grow further over the next few years, aided by a pronounced demographic advantage, rising wealth and hard-working populations. After recent relative weakness versus other global markets, notably the US, it could be a good time for long-term investors to consider upping their exposure.

Comments (0)