John’s Mining Journal: Pan African Resources – to sell or not to sell?

With gold on, possibly, a bit of a plateau, or even at what some investors might think is a peak, they might be thinking of re-deploying their profits from my gold coverage. But from which stock?

Pan African Resources (LON:PAF) (market cap £463m @24p) is definitely not one to sell, even though the price is down 15% since the end of July – when at 27.5p they had surged 150% above my buy recommendation a year ago.

Full results for the year to June will have just been published when you read this but were flagged by the company on 1st September. On about the same volume as last year, PAF’s gold sales were 26% higher, producing underlying earnings per share 87% ahead, with company debt halved throughout the year’s second half.

Pan African Resources – last year

These results were better than expected only a few months ago, and better than forecast by Edison, which follows the company in more detail than I can (they get paid to do it by PAF after all, and are more reliable than some other ‘paid-for’ researchers I could name).

No doubt a few traders took their profit at that point, but the shares now look as though ready to resume their up-trend, if only because, on Edison’s forecast of earnings per share of 16 cents, the forward PER at 24p is less than two. Not only that, but Edison is also forecasting a 1.5 cent dividend (1.15p) to deliver a 4.8% yield.

Admittedly that is less than the 11% that was behind my strong recommendation a year ago, but it is highly likely to continue to increase when the company’s planned re-opening of the refurbished Egoli project (which it acquired along with Evander Mines – which initially proved disappointing – in 2013) starts producing in three years’ time. It will add 38% to PAF’s current gold output at an above average profit margin, while PAF’s solidly existing high-grade Barberton Mines continues to extend its already long life to at least another 15-20 years.

So, Pan African Resources is not dependent on gold continuing strong. It shouldn’t be sold.

But what about some others? From whose profits it might be a good idea to re-deploy into some of my previously up-coming miners, like Horizonte Minerals (LON:HZM), or Chaarat Gold (LON:CGH), which is looking forward to bringing its Central Asia projects into production. It has just published interim results, when it warned that it will be coming to the market for more funds before the end of the year. But that has not dented over-much what looks like a steady long-term up-trend on the charts. It will be making an investor presentation later this week.

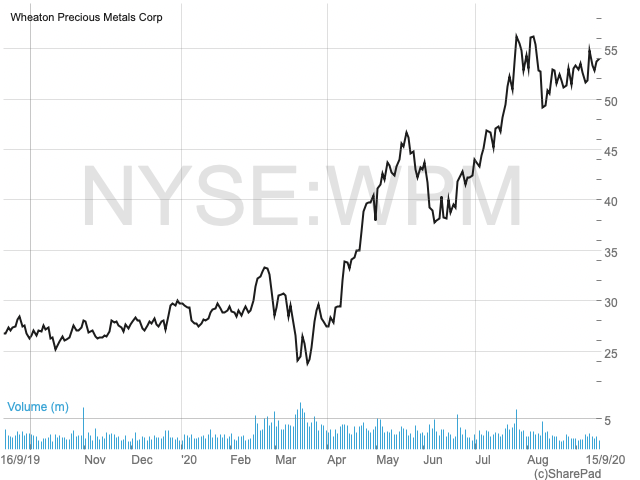

Among my candidates for at least partial profit-taking whether or not one thinks gold might have peaked, would be one of the streamers (which otherwise should be kept for other reasons). Wheaton Precious Metals (NYSE:WPM)(market cap $24.1bn @$54) was previously Silver Wheaton, which gives the clue why I think so. It is ahead by 260% in the last two years and has doubled in the last three months, to where it is on a rather low prospective 0.65% yield.

Although production from the six major silver producers who are its partners (‘clients’ in reality) has been badly dented due to Covid-19 restrictions, that has not affected the shares too much and gives an opportunity to take some of those profits. My thinking is that 95% of its physical output is in silver (with gold accounting for 5%). So, although in revenue terms gold accounts for 50%, that is only at the current gold/silver ratio of around 100.

Wheaton Precious Metals – last year

In other words, even if gold continues on up, WPM’s fortunes depend more on silver, which I don’t think can be relied on to continue upwards along with gold, even though many commentators appear to think that the link is unbreakable. In fact, the link has been stretching now for some time. The fact is that demand for silver is industrial, and not as an investment like gold, so there is a limit to the price it will eventually command.

Mines and oil wells

Both of the above are holes in the ground (and as Mark Twain would have said 150 years ago, each have liars at the top).

How much of a liar was whoever promoted Hurricane Energy (LSE:HUR)? And how many such might there be in the mining world?

HUR has seen its shares decimated (from the Latin for merely ‘one tenth’ – so when the shares are actually down 90%, “annihilated” would be more appropriate) following its announcement that its Lancaster oil field, in the Atlantic 60 miles off the Shetlands, can be expected to deliver only about 12% of what was predicted. And its eye-watering up-front cost has already been spent!

Before I took up mining shares 15 years ago, I was tempted by a few brokers to write about their oil exploration prospects. I was bemused, however, by the method by which the amount of oil to be extracted from the ground is presented to investors. From the results of drilling, the boffins (aka ‘competent persons’) come up with all sorts of concepts to explain how the mass of uncertain factors relating to oil actually there (and where) and how quickly it might flow under the pressure of the varying geology above and below, could be translated into some solid number that investors might understand. So, we have terms like ‘contingent’ resources and ‘probabilities’ of extraction. No wonder investors just take one of those terms as read and blindly stump up the funds.

Not so in the case of minerals in the ground. There, it is easier and cheaper to drill enough holes, and to understand how the ‘reliability’ of estimates of the amount of mineral depends on their spacing, together with the results of assays and long-learned knowledge of how the geology controls it. In turn, well established engineering expertise allows good estimates of the cost of extracting it. So it is that banks are willing to accept estimates of profits for mining projects that are ‘only’ accurate to within 10%. And it is why I have turned down invitations to write about oil for a long time now.

Comments (0)