Inland Homes – an urban regenerator yet to be recognised

Inland Homes is a canny operator with a well-located land bank and some very achievable strategic targets, writes Mark Watson Mitchell.

The confirmation early last week that the company has now received planning consent for its mega-development for its Cheshunt Lakeside, Hertfordshire site has yet to register in the market.

This is the largest consent that Inland Homes (LON:INL) has ever gained and its impact to the developer’s profits over the next few years will be considerable.

Over the last fourteen years this company has quietly become a leading developer of brownfield sites across the South of England. Its housebuilding projects have been both on its own account or in line with partnership housing associations. The development of its various sites over the years has often involved commercial and educational facilities being constructed as a by-product.

| Master Investor Magazine

Never miss an issue of Master Investor Magazine – sign-up now for free! |

Land activity is the foundation of the company – its core focus is in acquiring and developing brownfield sites. However, it is establishing itself as a respected housebuilder, both corporately and on behalf of others as part of partnership housing deals. That allows it to take more control of its sites and ensures a higher build quality while maximising value generated for the group.

The company has a number of joint ventures with institutional landowners, such as the National Health Service, the Ministry of Defence and local authorities, who often are owners of surplus land that could be developed commercially.

With the help of its own in-house construction team it can provide turnkey developments. At the last year-end the order book stood at an impressive £100m for the delivery of over 500 affordable homes over the next four years. These profitable deals are cash flow positive.

The group has a strategic focus on owning 10,000 land plots within the next four years. At the last year end it had 6,870, and of that total 1,708 had planning permission, while 5,162 were without permission. The size of the company’s sites ranges from under 50 to over 1,350 plots. It is a patient developer and enjoys considerable success in gaining the required permissions.

In the 2018 year the company completed 275 open market homes and 79 partnership equivalents. It also sold 837 of its building plots. At the year-end the total number of units, both private and partnership homes, under construction was over 680.

The company has a strategic focus upon building 1,000 homes a year, while it has a target of selling 500 consented private residential units per annum.

Cheshunt Lakeside is going to be a ‘major milestone’ for the company. It centres around the creation of a new ‘urban village’ on the site of the former Tesco headquarters. It takes in a total of 1,725 homes, 19,000 sqm of commercial space and also provides for a new primary school on the development.

Inland Homes is in a joint venture with an equal partner, in owning a total of 1,253 of the Cheshunt residential plots and 4,905 sqm of the commercial and educational space. The estimated gross development value is £620m for this project, the first part of which, 195 units, will be commenced as soon as feasible.

I understand that site clearance will get underway before the end of this year. Inland has an option to buy out its partner, which it will probably enact in due course.

The company changed its year-end from June to September, so until the next trading update is announced I will give no revenue and profit estimates upon the current year and next. However, winning the Cheshunt permissions will certainly boost its balance sheet values past last year’s 102.28p per share in net asset value.

I have known the two main men behind Inland Homes over the last two decades. I have a very strong respect for their professionalism and ability. They built up and sold off their previous AIM company, Country and Metropolitan Homes, to Gladedale in June 2005. Within days they were off and running with Inland.

They have built around them a strong and experienced management team. By using their knowledge, the company adds value throughout the planning process and looks to secure permissions within a two-year period.

The company has a well-located land portfolio in the South and South-East of England, with an attractive unrealised value within their land bank. It captures further value through private and partnership housebuilding activities. It also has some very achievable strategic targets.

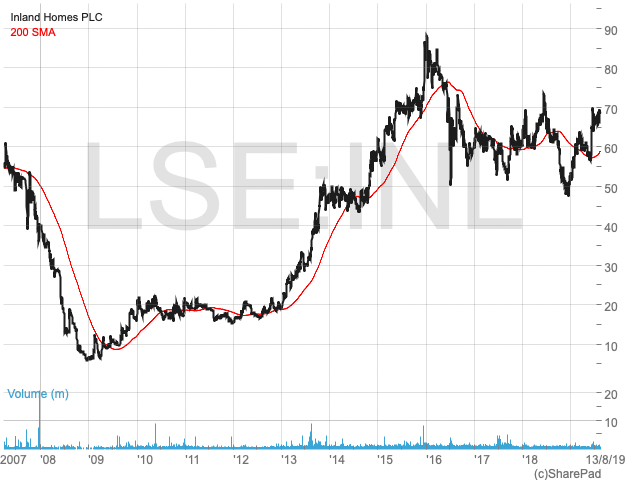

Valued at just £141m, the company’s shares, now trading at 68p, are undervalued. Even the directors have been buying recently. I have set a 110p target price for within the next 18 months.

The only concern I have is that another company might come along and steal Inland for a bargain price. Let’s hope the Inland directors do not give in to silly offers, as have the idiots at Telford homes.

Compounder – I totally agree with you that Telford has sold out too cheaply and even its buyers know that.

However, with Inland Homes I do believe that ,although they too are so undervalued, the Directors have such a determined number of goalposts to achieve within their selected timeframe. As I have said before, I have very high regard for both of its main Directors, and do not believe that they would sell out too soon.

In setting their goalposts they only have to show that they are well on their way to scoring and so making it apparent to others that they are so fixed on track. That is when I feel they would get the best price for their company (and for their shareholders).

The best prices are paid by buyers who can see that there is something left in the pot when they buy – always leave something in it for the next man.

Regards Mark Watson-Mitchell

Inland Homes share price does not appear to be going anywhere, Borrowings are high and if the housing market takes a dip later in the year, will this be an issue? Is it worth being patient ? Will the price reach your target or have the fundamentals changed?