Global gold stocks set to ride the higher gold price

John Cornford reviews nine of the more established gold-mining companies that investors might view as less risky in the current environment.

To date, I’ve been covering junior miners because, in normal conditions, following their development into producers along with the right timing and luck, can deliver the best returns for investors. But the times might be changing.

Some investors might now be looking at the established majors, who they might view as less risky, with a rising gold price that should be benefiting them all. So, I’ve reviewed nine that could be of interest.

I’m not an expert on these companies, so have merely described them, so that readers can then look to broker recommendations or the websites that purport to choose the best.

But be aware that by ‘less risky’, I mean that the big ‘goldies’ should be less erratic than junior miners. In practice, they have not proved particularly brilliant investments over the decade since the last mining boom in 2011, as shown by the VanEck ETF of the largest global gold miners. Its price now, even after the recent strong run, at $34, is still well below the $50 above which it traded throughout most of that year − a year ago it was still below $20.

So, even though the majors might be considered more stable than juniors on a medium-term timescale, in the long run they go through their own cycle. They try to keep shareholders happy by juggling the phasing in and phasing out of their portfolios of mines. This is difficult, though, when each mine has its own timescale for finding, developing and building − often up to 15 years long. Over that time, those companies have also been contending with diminishing gold grades among a narrowing choice of ore deposits, as well as a gold price that has sparked into life only recently.

However, the best companies have recognised that investors want profits and not necessarily growth, and have been reorganising themselves to achieve that. A rising gold price therefore comes as a bonus on top of their efforts to improve efficiency.

In this review I can’t warrant that any stats I provide are totally up to date, if only because, under those pressures to maintain good-quality production pipelines, there have been some very large mergers and acquisitions quite recently. This makes tracking underlying performances and prospects difficult.

The very largest merger took place early last year. Barrick closed a $7.8bn deal with Randgold to create its now $48.7bn-sized company, while Newmont paid $10bn for Goldcorp, to take first place with a $51bn current market value.

Other mergers were being mooted, with Barrick proposing to buy a 56% stake in Newmont itself, while Canada’s Kirkland Lake agreed to buy Detour Lake Gold for C$4.3bn and China’s Zijin Mining paid C$1.3bn for Canada’s Continental Gold.

So, with miners’ shares (although not all) now riding higher and with global gold output continuing to slowly decline, expect those rumours and deals, to continue.

Declining gold output amounted to some 109 moz (three million tons) in 2018, but the top 10 listed gold miners only accounted for some 26% of it. The industry is very fragmented, with neither China nor Russia (which collectively account for around 20% of global production) fairly represented. Many small miners aren’t listed at all.

As for companies’ exposure to gold, it should be realised that it frequently occurs in conjunction with copper, so that many miners produce both together, and whether they call themselves gold or copper producers depends on the relative importance of each. Solgold’s Alpala project in Ecuador, for example, will be a copper mine, but is capable of producing almost 1 moz of gold annually in its first 10 years.

And remember, also, that the very largest miners of all, such as Rio Tinto, BHP and Anglo American, don’t ‘do’ gold at all, preferring commodities they believe will command more stable and longer-lived industrial demand.

Don’t forget, either, the gold-streaming companies like Wheaton Precious Metals and Franco-Nevada, which are particularly geared to a rising gold price. And lastly don’t overlook the various gold-oriented exchange traded funds (ETFs).

The largest of these is the GDX VanEck Vectors Gold Miners ETF, which replicates the share performances of some 50 stocks. Its largest components are Newmont (15.7%), Barrick (14.4%), Franco-Nevada (8.3%) and Wheaton Precious Metals (5.9%). Its top 34 companies saw their revenues increase by 31% year-on-year in the last quarter, while their operating cash flows were 68.7% higher.

It’s for the investor to decide whether to chase that recent performance. The short-term outlook for gold isn’t necessarily that it will continue steadily upwards. Some observers are recommending caution, even though Newmont and Bank of America see even higher prices ahead. So, the nine stocks that follow (the most I can fit into this review and not necessarily the best) are for those who believe a strong outlook for gold will trump all other considerations.

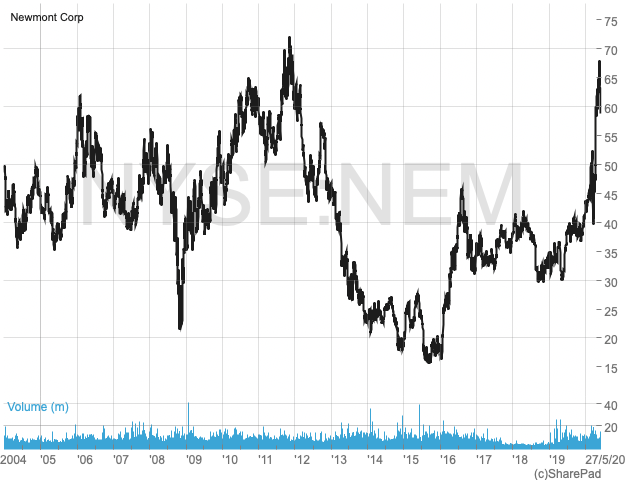

Newmont Corp (NYSE:NEM) market cap: $51bn @ $63.5 per share

Newmont is now the largest global gold miner after its merger in January last year with Canada’s Goldcorp. Current year revenues are around $11bn and it has reserves (ie mineable gold) of over 95m ‘gold equivalent’ ounces (ie including some 15% of revenue which is copper, zinc, silver and lead), which almost guarantees output of 6-7 moz annually for at least the next 10 years. The output includes Newmont’s 38.5% share of the world’s largest gold producer, Nevada Gold Mines.

Of Newmont’s gold, 69% occurs in North, Central and South America; 19% in Australia; and 13% in South Africa, across 14 mines, of which it considers eight are ‘world-class’. In addition, 14 others are still in development.

Goldcorp was struggling, but has high-quality gold reserves, from which Newmont hopes to deliver better results, so that analysts expect it to continue to grow even without an improving gold price.

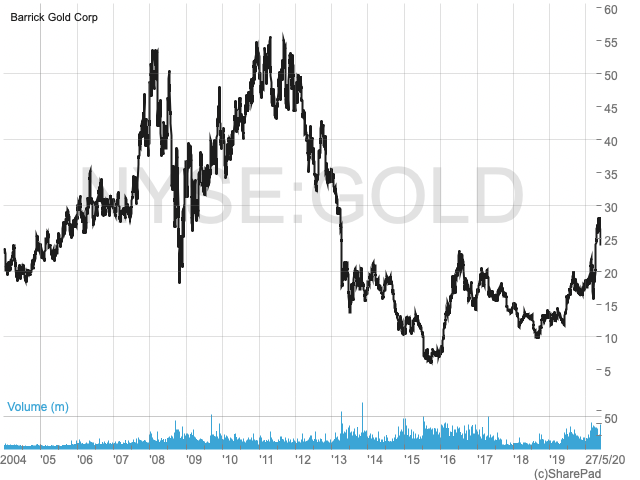

Barrick Gold Corp (TSX:GOLD TSX:ABX) market cap: $46.8bn @ $26.30

Barrick had revenues of $9.2bn in 2019 after its $7.8bn merger with Randgold, producing 5.5m gold ounces, and earning 51 cents per share − 46% higher over the year.

Its largest operation is shared 61.5/38.5 with Newmont, comprising eight mines in Nevada forecast to produce 2.1m gold ounces this year at an overall cost of around $900/oz. Many of its other operations are also joint ventures, which makes describing their contributions more complicated than there is room here to describe. Mostly, Barrick operates in the US and Canada; Peru and Chile; Mali and the DRC; and Tanzania and Botswana, claiming that among them are five of the world’s top-10 gold assets, including Pueblo Viejo in the Dominican Republic.

Financially, Barrick had struggled somewhat, but a recent change of emphasis towards profitability rather than gold volumes, and the Randgold merger, has changed all that as shown by the strong share price. Even though its share of gold reserves stands at a healthy 71 moz, production is forecast to only remain flat over the next 10 years, at around 5 moz annually. What investors are looking forward to is an increase in the dividend and Barrick’s ability to deploy a $3bn acquisition war chest.

Among its use will be an increasing exposure to copper where Barrick has been eyeing Freeport-McMoRan’s Grasberg mine in Indonesia.

Newcrest Mining (ASX:NCM) market cap: $US$16.5bn @ 31.5 AUD

Melbourne-based Newcrest claims the lowest operating cost and the longest life reserves of any major at its original mines in Australia, Indonesia, Ivory Coast and Papua New Guinea, where it produced 2.5 moz in 2019. Just over half stemmed from Australia and one third from Indonesia and Papua New Guinea, while a jointly owned mine at Wafi-Golpu in Indonesia is being developed and is claimed to be one of the largest gold/copper prospects in the world.

While initially concentrating on the Australia Pacific region, Newcrest has also ventured into the Americas, adding to a large joint venture in Canada and building stakes in South America (where it has a 15% stake of Solgold), as well as signing joint ventures in four Latin American countries.

Of interest is its recent deal to acquire a streaming contract from Orion Finance for Lundin Gold’s Fruta del Norte mine in Equador (in which Newcrest already held a 32% stake) which together with a current AU$1bn capital raise points to further expansion there. As described elsewhere, streaming deals add even more profit to the upside deriving from a rising gold price, which is shown by the fact that Newcrest paid $450m for the stream, which had provided Lundin with a payment of $300m only three years previously.

So, of the major gold producers described here, NCM appears to be one of the more expansionary minded, with first results from its majority share in the Red Chris mine in British Columbia, for which it paid $2bn, due to boost this year’s results.

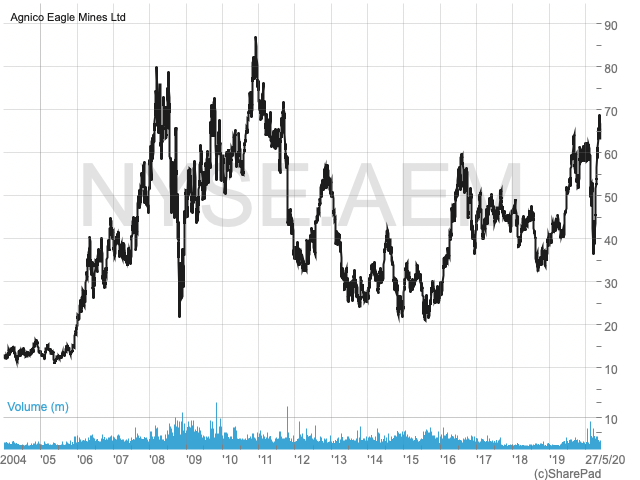

Agnico Eagle Mines Limited (NYSE/TSX:AEM) market cap: $15.8bn @ $65.65

Agnico Eagle is a Canadian-based gold producer with smaller operations in Finland and Mexico, and exploration and development activities extending to the US.

I include it here, even though it is perhaps less well-known in the UK, because it has an exceptionally long record − for a miner − of reliable growth.

Production has doubled since 2012, and although it will be reduced this year due to Covid-19, is expected to be 15% higher next year than in 2018, when output was 1.63 moz. It has a policy of not hedging its forward gold sales, so has full exposure to the gold price, whether higher or lower, and also has a lower-than-average cost of production which, this year before Covid-19, was forecast to be around $900/oz on an all-in basis (ie including ongoing capital costs, as well as day-to-day cash costs).

With gold reserves (proven and probable − ie highly reliable) amounting to 21.6 moz at its four major mining districts, and another 18moz in the less reliable measured and indicated category, the company is confident that its growth will continue into the foreseeable future. This is why most of the 20 North American analysts following it expect it to outperform and to preserve its 37-year history of paying a dividend.

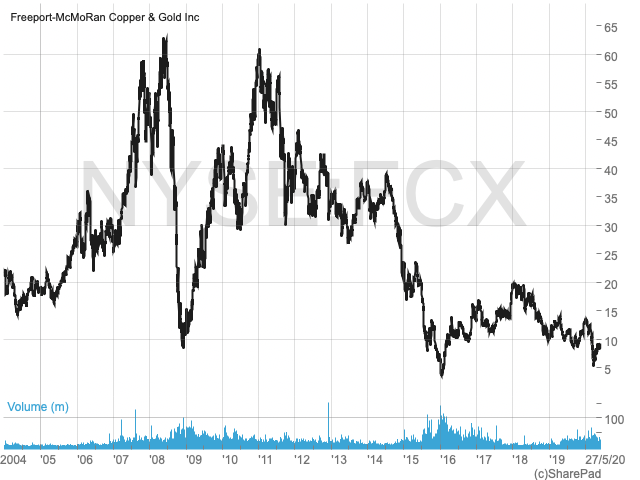

Freeport-McMOran (NYSE:FCX) market cap: $12.7bn @ $8.74

Freeport claims to be one of the world’s-largest, listed producers of copper, but is included here due to its part ownership of the Grasberg mine in Indonesia, which mined 0.9 moz of gold in 2019 and double that in 2018. It also has significant operations in the Americas, including the world-class Morenci mine in North America and Cerro Verde in South America.

Grasberg is one of the world’s-largest copper and gold deposits, but has held back FCX’s results in the last two years while its open pit has been running out of resources, and is being replaced by underground mining. This caused overall revenues to fall drastically from $18.6bn in 2018 to $14.4bn in 2019, explaining the shares’ weakness since 2018.

However, FCX is strong financially and has been aggressively reorganising its whole mining portfolio, which, together with Grasberg’s underground operations due to contribute soon, underlies expectations of a sharp recovery and resumed growth from next year onwards. Analysts particularly like that, with development spending falling, and gold continuing to be strong, and assuming copper remains reasonably healthy, the company should generate significant amounts of cash and further improve its already strong balance sheet.

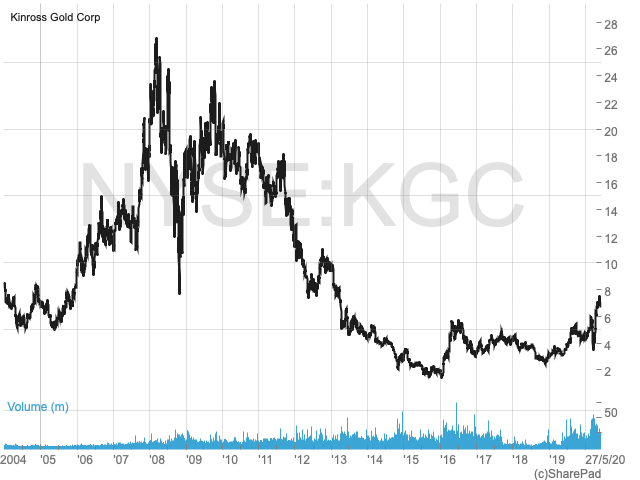

Kinross Gold (NYSE:KGC TSX:KGC) market cap: US$8.9bn @ $7.05

Kinross mined 2.5 moz of gold in 2019: 56% in North and South America; 23% in West Africa; and 21% in Eastern Siberia. Gold reserves total 24.3 moz in addition to another 35 moz in less reliable resources.

While the company doesn’t aim to increase production significantly over the next five years, and it has remained around the same level for the last five, Kinross’s earnings and cash generation have increased over the period, not wholly due to any improving gold price.

However, in January Kinross acquired fellow Canadian miner Detour Gold, and also in 2019 acquired a new prospect in Russia, the former boosting recent first-quarter earnings per share by 30% on revenues 82% higher. With higher gold prices, analysts expect the company to start generating significant cash flow of more than $700m this year, up from $16m in 2019, adding to an already strong balance sheet.

AngloGold Ashanti (NYSE:AU and JSE:AU) market cap: $7.8bn @ $26.00

AngloGold has been based in Johannesburg for over 100 years, producing 3.3 moz of gold in 2019 in all continents except Asia.

More than 20% (22%) stemmed from North and South America; 19% from Australia; 47% from West and Central Africa; and only 13% from South Africa from where rising costs and the depletion of its once highly profitable mines has caused it to withdraw in favour of the rest of Africa and the wider world.

It is building its ore reserves to over 27 moz of gold out of 93 moz in total resources, about half of which are in Ghana and the DRC, with the rest almost equally spread between Guinea, Tanzania, Australia, Argentina, Brazil and Columbia.

AU is to sell its only remaining mine in South Africa to Harmony Gold this year for $300m, while it is finalising the development of what will be its largest mine. Obuasi in Ghana has only just poured its first gold and expects to produce up to 0.4 moz per year from 2022 onwards at one of Africa’s lowest costs. Thereafter AU’s plans include a move into Nevada and Canada.

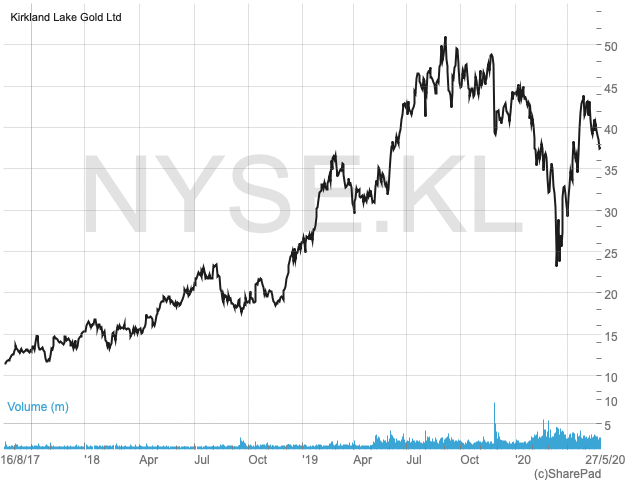

Kirkland Lake Gold (TSE:KL) market cap: C$14.8bn @ C$52.00

Kirkland saw its shares soar twelve-fold in the three years to July last year as its Fosterville mine in Australia contributed to a trebling of gold output, at the same time as costs fell dramatically.

Gold production in 2019 was just short of 1.0 moz, and this year is expected to be well ahead of that, from KL’s two existing mines in Canada, as well as in Australia, and from the newly acquired Detour Lake Gold in Canada.

Helped by a large boost from Detour Lake, KL’s gold reserves have jumped to a total of 20 moz, of which 2.5 moz are in Australia. So, with industry costs at the lower end of the spectrum, analysts are almost all recommending the shares as a buy.

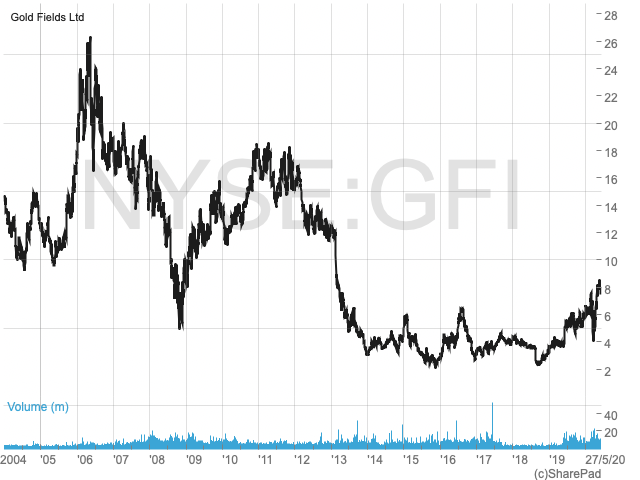

Gold Fields Ltd (JSE:GFI and NYSE:GFI) market cap: $6.8bn @ $8.28

Headquartered in Johannesburg, Gold Fields has eight operating mines in Australia, Chile, Ghana, Peru and South Africa, as well as several development projects.

Production last year was 2 moz, against gold reserves of around 52 moz, of which 63% is in South Africa, 14% in West Africa, 12% in Australia and 10% in South America, where GFI also has 310,000 tonnes of copper.

As in the case of AngloGold, Gold Fields was suffering from its South African operations and their high costs, although recently it has restructured its capital, selling off assets, and paying off loans, as well as by moving production away from South Africa.

New mines in Ghana and Australia helped production in 2019 to be skewed more towards those areas, which accounted for 35% and 41% respectively of the total, while one mine in Peru contributed 13%. The switch will continue, with a new project in Chile expected to produce 0.4 moz annually from 2023 onwards.

These moves helped what had been an uninspiring financial performance improve dramatically in 2019, so that analysts expect the trend to continue and that revenues could double over the next three years with a consequent strong financial performance.

Comments (0)