Commodities Round-Up

Its time to canter round my list of mining stocks, to see whether in this commodity slump any of them might recover faster than others. I’m assuming they WILL recover, because life has to go on; many of them are about to, or are gearing up to, or are waiting for banks and investors to help them to, produce what everyone thinks the world will need over the next decade.

But ‘stocks’ are not the same as their ‘projects’. It is their projects that need to survive, and at the moment some ‘stock’ investors might be worried because they fear delays which will cut yet again into their share of the company and its ‘projects’.

Nevertheless there are still some miners not as concerned as others about funding delays, and some commodities that ought to receive it faster than others

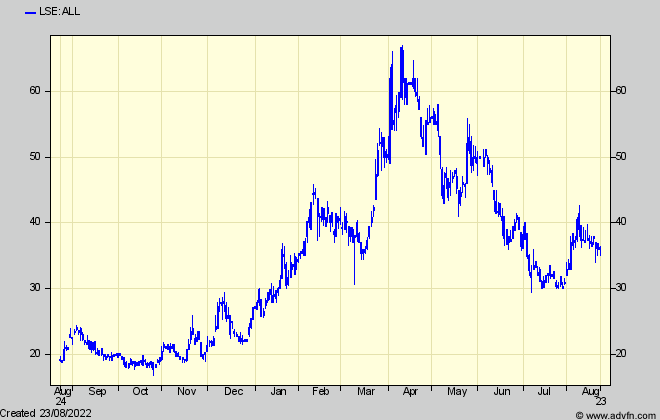

Lithium has held up better than others, which means taking another look at Atlantic Lithium (ALL) which, last December, I said looked interesting for the medium term, with most funding for its Eyoyaa project in Ghana almost guaranteed by NASDAQ’s Piedmont Lithium in return for 50% of revenues. Since then Eyoyaa’s lithium resource has been expanded by 42%, while drilling outside the existing one has shown good grades – increasing the potential for future growth. Meanwhile, the prospectus for a secondary listing on ASX has just been published, which won’t want to raise new cash but enable the estate of an early, now deceased, major investor to sell to new ones, who are reported will take up all the the c23m ASX shares on offer at A$0.58 – which equates to about 34p.

Atlantic Lithium – last year

I was a bit cautious originally about chasing the shares, then below 30p, on my usual grounds that the NPV didn’t justify more than 40p, and even then not yet. However the shares subsequently rocketed above 60p, before the war-induced slump brought them down to 30p, and now 37p. Sorry about that missed – but hairy – opportunity, but perhaps now is a chance to get in at a more sensible price.

Sticking with the battery metals (but the rarer earths variety), another company seeming to deserve funding which, even so, is a long time coming, is Pensana (PRE) who I wrote about only in April. Despite that it is pressing on with its own money, and some limited government grants, preparing to build its rare earths plant at Saltend near Hull, and its mine and processing plant in Angola, there is still no progress on the full funding it will need. Hopes have been that the UK government will help more, especially with the business secretary attending the ground breaking ceremony and announcing a new ‘Government Critical Minerals Strategy’. No doubt he is trying to persuade the private sector to step in first.

One trouble is that PRE doesn’t get very enthusiastic support in the investment press (on the entirely spurious, irrelevant, and illogical ground that its Chairman and founder Paul Atherley ran into un-surmountable environment difficulties in his uranium project in Spain). Another might have been highlighted by the recent news that the vital BritishVolt gigabattery factory in Northumberland, like Pensana, appears to be finding funding difficult. I would have thought that, one way or another, these plants have got to be built.

Yet another would-be whose product should benefit from the predicted long term shortage of its cheap to produce potash fertilser is Emmerson (EML). Its shares held up reasonably well (spiking in May) until recently, when worries resurfaced about the dilution shareholders will suffer when (if) EML makes the share issue it will still need to make, no matter how big any bank project loan to help built its Khemisset mine.

That project has always looked to be very profitable even after repaying any loans but, as ever (like the almost as profitable Horizonte Minerals which I covered for a long time before it eventually secured funding) the terms of loans and share fund raisings in recent years have always proved more onerous than investors had been expecting. (Banks and Institutions are always much more cautious than the latter). So despite that many private investors want to ‘get in’ before funding secures the future of their project, I always advocate waiting to see, and to avoid being sucked into to any spike in the shares that follows. Almost inevitably it takes time for the real numbers shareholders will see to sink in, and to appreciate the time before they see them. Just as for Horizonte Minerals who got its funding two years ago, that will be too long for many investors to have waited. Hence the shares were languishing even before the commodity slump kicked in.

As for EML’s short term, while recent Press reports in Morocco are said to be writing as if Khemisset is a done deal, its environmental impact report which is a necessary precursor to any deal, is still not approved. So potential investors are still jittery.

Elsewhere my cautions against believing a NPV ‘target’ will be met eventually, let alone soon, naturally become less valid as production approaches. Investors start anticipating cash flow which suddenly switches from negative to positive – and a large one at that.

Scotgold (SGZ) – one of three Celtic Goldies I’ve featured from time to time (the fourth, Dalradian’s larger, high grade Curraghinalt mine in Tyrone isn’t a listed company any more) is now just into that phase. I’ve been following Scotgold for over ten years from when its Cononish gold discovery in the Grampians looked potentially highly profitable on the then size of the company (founded by savvy Australians) and on what looked like a relatively cheap path to production. But there have been problems and delays one after another, so that a few months ago I said SGZ’s NPV in relation to the share price had become too low for excitement even though production was in view – especially when the company was still needing short term loans to tide it through and pay for new kit.

But Scotgold is putting that new kit to use and quickly ramping up production and income this year, and paying back those loans, so that for investors steering clear of the shenanigans everywhere else, it could see a useful spurt from its current 70p and £42m market cap.

In July SGZ announced that, after clocking up £3m of losses in the last reported half-year to December (full year results to June are due in December) it had achieved ‘commercial’ operation – meaning three consecutive months of cash income exceeding cash costs of production.

While this doesn’t mean statutory company profits will be positive quite yet, gold production is now

increasing rapidly and is forecast to be between 2,900 and 3,300 ounces in the current quarter (slightly less than the 2nd quarter which benefited from ‘bunching’ and higher than expected grades) but on course to double to an ‘annual rate’ of 23,500 ounces by the middle of next year.

Scotgold – last 3 years

That would mean annualised revenue around £30m and increasing, for at least the planned nine-year life of the mine – which is expected to be considerably extended with more drilling. The exact rise in profit is difficult to predict, but with high gold grades (up to 19oz/tonne – characteristic of all the Celtic gold districts) it should soon meet the levels forecast by the company’s broker Shore Capital who states £13m pa free cash flow, or about 18p per fully diluted share compared with a 70p share price. On those figures a dividend could also be on the cards.

It should be noted (and might confuse a little) that Scotgold is registered in Australia, so results are reported in Aussie dollars which at present are some 58cents per GBP. Expect fairly frequent updates from the company now that it is more confident, so the shares could become more volatile than normal. But even if there is yet another unanticipated upset (why many investors are still wary of the shares) I can’t see much downside risk, and a reasonable upside as the story unfolds.

Comments (0)