Why the FED may struggle to implement its policy rate

With the FED hiking its key benchmark rate one should expect interest rates to start rising across the yield curve. Liquidity conditions will tighten and the FED’s balance sheet is going to shrink as well. Hmmm, not so fast! The FED has two trillion problems still to solve, as its monetary policy framework is years behind other central banks’ settings, in particular the ECB. Hiking rates is not a mental exercise, it will involve some headaches for the New York FED.

The FED doesn’t really hike rates, it does announce a target for the FED funds rate, which is the rate high street banks charge each other for unsecured overnight loans. The central bank first injects liquidity into this market but then allows the game to be played between banks. The outcome of the game – the interest rate – is just the result of the interaction between those banks. It is not set by the central bank. This means that the FED announces a target rate, known as the FED funds rate, and then uses its magic to make sure the effective funds rate is near the announced rate. But, of course, the effective funds rate is not 0.25pc or 0.50pc just because the FED said it wants it to be at that level. The FED must do something more than just announcing a wish list.

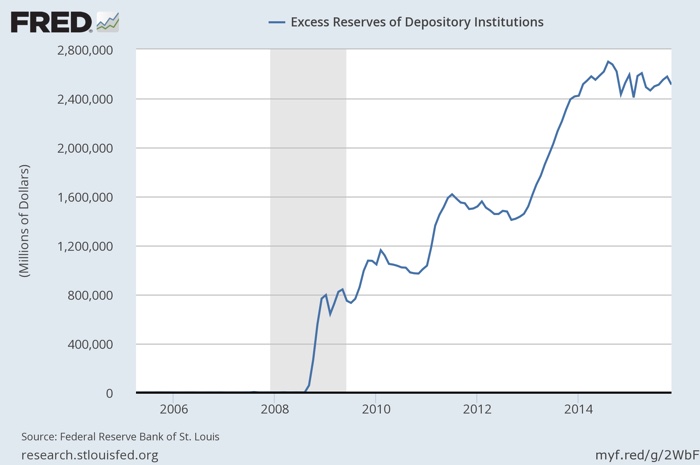

Investors very well know that what gives pricing power to the supply side of a market is scarcity. Commodities markets usually operate under very limited supply conditions, which give pricing power to producers. But if scarcity ceases to exist, producers just lose control of the market. OPEC is a great example depicting this dynamic. The game played by central banks isn’t much different. For the FED to be in control of what happens in the overnight lending market, it must create scarcity. On one hand, the FED must create a need for reserves to force banks to demand liquidity. On the other hand, it must offer a limited quantity of that liquidity such that there is scarcity. As reserves are a monopoly product, the supply of reserves is under the control of the central bank. To be in control of demand, the central bank creates reserve requirements, which imposes banks to carry reserves at the end of the day. Having control of both the supply and demand, the central bank has a great deal of control over the overnight rate. If the FED wants to spur a rise in the effective funds rate, it just needs to reduce the supply of reserves in the market. Because banks still need to fill their reserve requirements at the end of the day, the resulting price of reserves should increase. In theory, if the FED were able to drive the effective funds rate lower across the years, through injection of reserves, it should also bee able to prompt a rise in the same rate by absorbing the excess liquidity. But in practice it is not that simple, because of a reality very well depicted in the following chart:

Since 2008 the Federal Reserve Banks have been accumulating excess reserves from depository institutions while the central bank has been purchasing assets through QE. Faced with a lack of lending interest and a lack of solvent borrowers, banks were unable to lend the reserves created through QE, which quickly piled up at their vaults. One way or another, the reserves the central bank created to purchase Treasuries from the banks ended up deposited back at the FED. In total there are around $2.5 trillion in excess reserves. The injection of reserves through QE was so large that had the FED not adopted some tools to control the effective funds rate, that rate would by now be negative.

Under these circumstances one wonders how easy it will be to drive rates higher again. For the rate to start rising, the FED needs to create scarcity again, which means to first drain the $2.5 trillion in excess reserves to then regain control over the market to drive the interest rate higher. That would mean selling $2.5 trillion in Treasuries and agency debt, an action that would most likely lead to the worst crash ever felt in financial markets. Therefore, selling Treasuries to prompt an increase in interest rates is not an option and the FED needs to look elsewhere for tools to accomplish that goal.

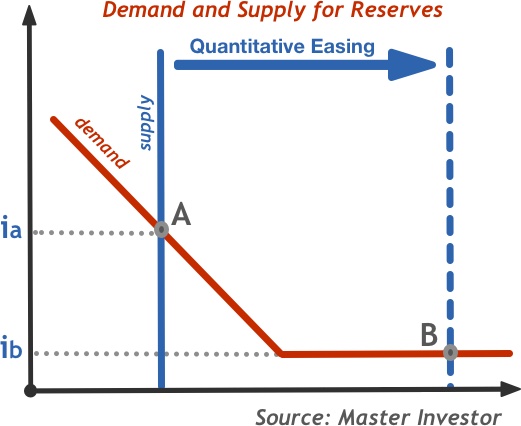

The above chart depicts how the QE programme played out its effects in the overnight lending market. The QE programme acts as an expansion in the supply of reserves, driving the effective funds rate lower (from ia to ib). That rate would by now be negative, if there was no floor. But the FED introduced the floor we see in the figure when it adopted its QE programme, to avoid the negative rate and give more control over monetary policy when it was to be reverted. The rate ia in the chart is the IOER – Interest Rate on Excess Reserves. The FED pays interest on money parked at its vaults in excess of the reserve requirements. This is similar to the ECB’s deposit facility rate, something the FED should have introduced long ago, as this is a powerful tool to keep target rates inside a corridor. But… it is powerful in the hands of the ECB but not as powerful in the hands of the FED. The reason is because the FED limits access to only depository institutions while there are many other institutions playing in the overnight lending market. In a normal situation, arbitrage rules wouldn’t allow for the overnight rate to be below the IOER. Why would a depository institution lend money in the overnight market for cheaper than it can lend to the central bank? But, as there are some additional institutions in the overnight market, the effective funds rate may sometimes decline below the IOER. The IOER is just a soft floor. With this in mind and because there are many frictions in the overnight lending market that don’t allow for depository institutions to unfold arbitrage strategies in full, if and when the FED were to attempt a rate hike, it could very well fail. If the depository institutions can’t borrow freely in the overnight lending market to then deposit the money at the central bank, large differences may persist between the effective funds rate and the IOER, which mean the FED may fail in targeting a level for the funds rate.

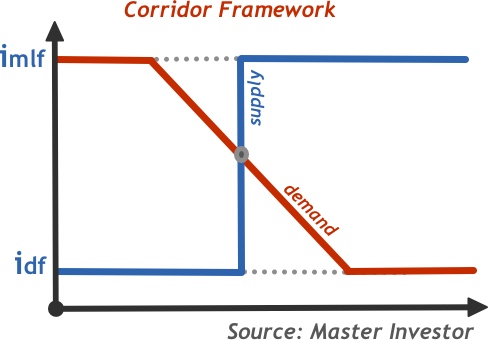

This kind of problem doesn’t exist at other central banks where monetary policy is conducted through a corridor with effective floors and ceilings for the target rate. The ECB has a perfect track record of keeping rates inside the corridor it establishes. The overnight rate cannot go below the deposit facility rate because, at that rate, the ECB demand for reserves is unlimited and there isn’t the same kind of restrictions as with the FED. By a similar token, the overnight rate cannot go above the marginal lending facility rate because the ECB supplies unlimited amounts of reserves at that rate, which means banks won’t bid anything higher than that in the overnight lending market.

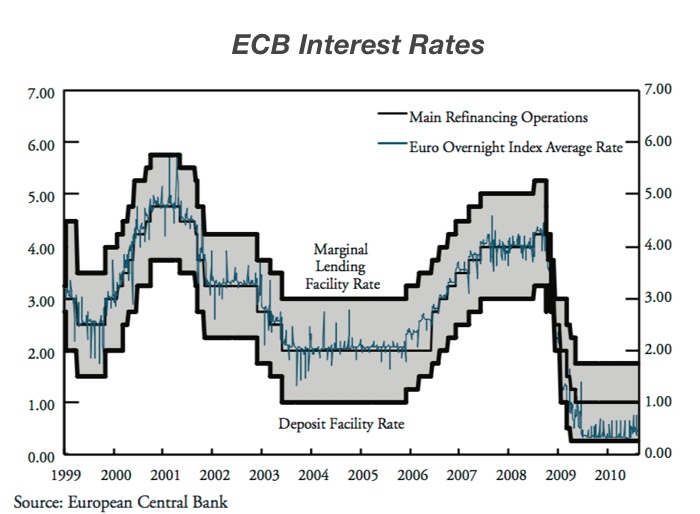

The ECB has been very effective at managing the EONIA within its triple-rate framework.

But will the FED be as successful as the ECB? Many are the doubts as the framework in which the FED operates is much inferior to that of the ECB. To surpass the problem of the IOER working as a soft floor, the FED created another floor which is known as RRP – Overnight Reverse Repurchase Programme. This is a programme similar to the way policy is conducted at the ECB, through repurchase agreements. This tool allows the FED to sell assets to investors with an agreement to purchase them at a later date (usually the following day) at a higher price (to cover interest). This serves as a floor because investors would never lend money in the overnight market at a lower rate than they can lend riskfree (to the central bank). The biggest difference between the two floors, the IOER and the RRP, is that there are much more participating entities in the second. In practical terms the first is set above the second. When the FED announced a new target range for the FED funds rate of 0.25-0.50pc last Wednesday, it also announced a level of 0.25% for the RRP and 0.50% for the IOER. Whether this is going to work remains to be seen because, as I mentioned before, this is an experimental framework, which buys much from banks using a corridor to manage rates but that has not been built from scratch to work that way. It suffers from several flaws, when compared with the ECB system, for example. I feel that if inflation rises faster than expected the FED isn’t in a position to fight it without leading financial markets towards a severe crash, because under its framework the only way to lead interest rates higher at a fast pace is by selling Treasuries on a large scale – an anti-QE programme.

Comments (0)