Time to Rethink Macro Policy

“So just as I want pilots on the planes that I fly, when it comes to monetary policy, I want to think that there is someone with sound judgement at the controls.”

– Martin Feldstein

The time when physical money will be made illegal is not that far away, as central banks have now exhausted all conventional and unconventional monetary policy tools. Global growth is still sluggish, deflation seems imminent, and some emerging economies are cracking at full speed. Over the last year, oil is down 50%, copper is down 21%, and not even gold or silver could escape the trend. China no longer wants to fuel its economy through government spending and the developed world, in particular Europe, is so frenetically worried with government debt, that it forgot the basic relationships between austerity and growth.

Policy-makers seem insane and will incarcerate us inside the deepest economic shadows. Central banks are pushing for creative measures for governments to rely on them while punishing the population for the excess spending of the past. But, while there is no doubt about the necessity of government spending contention, there is doubt about its timing and strength. It is tough to save when you just don’t have enough to live. So eventually the best for you is to go make a living before. At the same time, the current mix of fiscal tightening with monetary easing goes against the theory while pushing for a massive experiment with unknown consequences at a global scale. The outcome may be disastrous and push the global economy towards the worst recession ever.

Policy-makers keep scratching their heads without understanding why there is no inflation. I just have the answer: austerity.

The mix of tight fiscal policy (which reduces disposable income through tax increases and benefits decreases) with expansionary monetary policy (which increases wealth of those who own assets), leads to a major redistribution of wealth from the poor to the rich, creating financial bubbles and goods and services deflation. The story is really simple. The central bank bids on government debt, which contributes to increase the price of this asset class and to then push the price of other riskier assets. Undoubtedly the wealth of those who own these assets increases. While purchasing assets, the central bank also keeps interest rates at a minimum, expecting those who saw their wealth increase to invest in the real economy or to eventually increase their spending. But these people have a very low propensity to consume, so they save instead. They are not willing to invest because there is no demand. And, there is no demand because the austerity measures ruined disposable income, in particular of those with higher propensity to consume. The asset owners then accumulate the extra money in alternative assets, bidding on pre-existing assets, and then creating bubbles. In summary, tight fiscal policy negatively impacts consumption, which prevents investments from occurring. It should not come as a surprise that the price of the assets purchased by the rich is higher while the price of the goods purchased by the poor is not. In other terms, we have asset bubbles and no inflation. That is a consequence of policy. Increasing the scale of the current policy mix will just increase the scale of the problem.

As a consequence of the status quo in macro policy, “relative to its 2012 forecasts, the IMF has revised its estimate for the level of US GDP for 2020 downwards by 6%, Europe by 3%, China by 14%, Emerging Markets by 10%, and 6% for the world as a whole”, as reported by the FT. While the current crisis is effectively not the worst in memory (except for Greece), it has been a long-lasting crisis without the fast recovery phase that usually follows a deep crisis. The mix of fiscal tightening with monetary easing creates a vicious cycle. While the situation in the US and the UK is not dramatic, Europe has been experimenting his own poison.

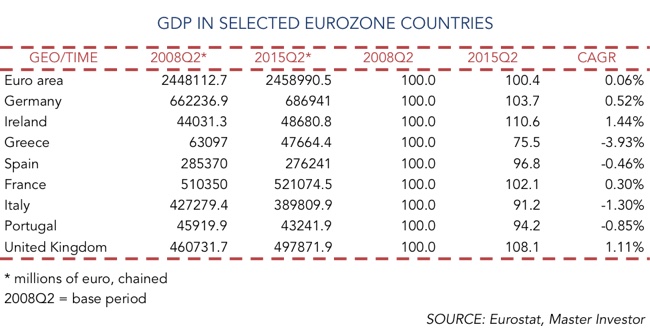

Over the last 7 years Europe has been growing at a 0.06% pace, which is just equal to the ECB main refinancing rate. Germany, which has been traditionally seen as the engine inside the monetary union, is not in much better shape, as growing at a 0.52% annual rate is definitely not enough to even keep the level of employment. In the peripheral countries, where austerity was deeply applied, the situation is much worse (with the exception of Ireland). Greece is decreasing almost 4% per year, Spain 0.5% and Portugal 0.9%. The structural reforms are needed, but they should be only gradually applied and very well timed. At the same time, we should never forget, that most of the problems in peripheral countries come from the banking sector. Years of unregulated credit expansion led banks to an uncomfortable leveraged position, which under our monetary system corresponds to a leveraged household, government, and corporate sectors. That is the result of artificially keeping interest rates below their natural levels in a system where, to expand money, one needs to expand debt. It comes a time where there is more debt than it can ever be repaid and the system collapses. Then the European solution is to apply austerity to reduce debt while allowing the ECB to lead to another increase in debt. An absolute senseless mix.

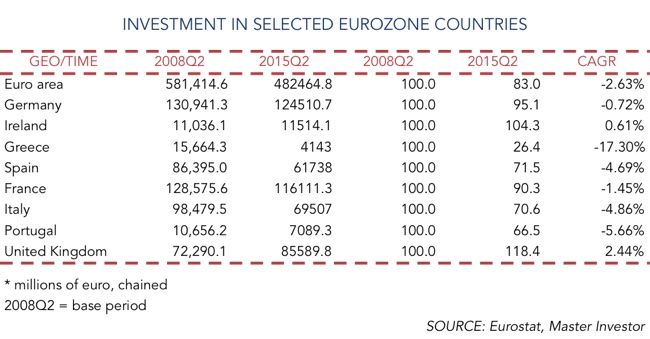

For those who believe low interest rates can really lead to more investment, even in the presence of austerity, the following table helps demystify the issue:

The Eurozone as a whole has seen investment decrease at a pace of 2.6% per year over the last 7 years. In countries where austerity was more painfully applied, the decreases were severe. In the case of Greece, the accumulated loss is now 73.8%. Those who own assets may indeed experience a boost in their wealth due to monetary easing, but they never invest back in real assets while demand is depressed. The current monetary easing is a waste of time and just creates the roots for the next financial crisis.

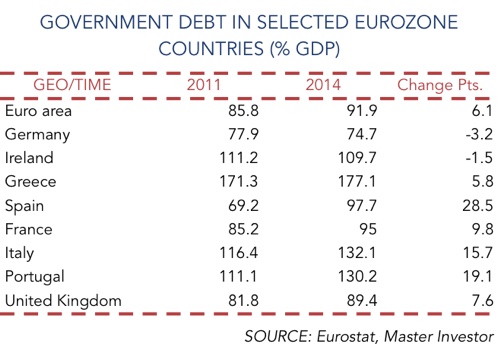

Regarding the positive results on government debt that is expected from austerity, that has been either a myth or an excuse:

The Eurozone, as a whole now has 6.1% more debt. It is exactly in countries with extreme fiscal contention, where the results are the worst. See for example Portugal, Spain and Italy, where debt is up between 15 and 28%. When all try to save at the same time…

It is time to stop and reflect on what we have been doing. The mix of policy is not working. In my view it is because it redistributes wealth from those with higher propensity to consume to those with higher propensity to save. Because investment without demand just leads to inventory accumulation and excess capital, those with the excess capital prefer to build cash piles or invest in financial assets. In the process, financial assets disconnect from fundamentals, while the economy shrinks for lack of real demand.

At this point, many will say: “We just need to do more, we need negative interest rates, to further increase the incentive to consume”. They can go as far as to turn money all-digital, making it illegal to hold physical currency. Their idea is to set a negative interest rate and avoid conversion in physical cash. Their goal is to make it costly to hold cash and convince you to spend more. But all they would achieve is less consumption and uglier asset bubbles.

While I still believe the government should refrain from intervention, if there is a case in favour of it, it certainly isn’t for austerity. We should put an end on monetary easing to avoid bubble creation and eventually allow for some real incentives for consumption. It is time to reduce VAT substantially.

Comments (0)