The Fed’s View On Price Stability

Economic analysis by Filipe R. Costa

Long gone are the days when central banks used to target monetary aggregates in order to attain price stability. Until the early 1990s, central banks thought the correlation between the money supply and inflation was strong enough for them to be able to define as their intermediate objectives some growth rate for M1, M2, or whatever M number they were using to target the money supply; and then, at the end of the chain reaction, they would find price stability. But, as they failed miserably (with the exception of the Bundesbank), they changed their view and started targeting the inflation rate directly while using the interest rate and the yield curve as the instrument and intermediate objective, respectively. Since that major change, central banks have been so effective in lowering the inflation rate that they are now struggling to find anything tangible to do.

But despite having already accomplished their mission of stabilising price growth at low levels, central banks are still very active. To speak the truth, they have never been as busy as today. How could that be?

With the advent of fast-growing inflation rates due to the abandonment of the Gold Standard in 1971, the US Congress amended the then outdated Federal Reserve Act in 1977 to encompass a more serious goal of price stability. The monetary policy objectives of the Federal Reserve were then defined as:

“The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates.”

Unlike other central banks, which are solely mandated towards price stability, the Fed was attributed a so-called dual mandate to pursue price stability and a high level of employment at the same time. While appearing different, single and dual mandates are exactly the same in the long run, as there is no known trade-off between inflation and employment in that time horizon, and pursuing price stability is compatible with full employment. But in the shorter-term it allows the Fed to pursue a more accommodative policy to achieve higher levels of employment even when the price stability objective has already been met.

While price stability is supposed to mean that prices are not expected to change much, there is significant scope for misinterpretation of what it really means. When quizzed as to its nature, former Fed chairman Alan Greenspan stated “price stability is that state in which expected changes in the general price level do not effectively alter business and household decisions”. Even though the definition gives some extra clues as to the effects of price instability, it adds little in terms of defining a quantitative level. When forced to provide a number, Greenspan then replied,

“I would say that number is zero, if inflation is properly measured.”

Now that many years have passed since the Greenspan era, we can say that either he wasn’t right about the zero as being the target number or inflation isn’t properly measured by the Fed, because the central bank explicitly pursues an inflation rate of 2% as being the magic number compatible with price.

As reported by Robert Heller, a former member of the Federal Reserve Board of Governors, the Fed had already adopted an inflation target around 2% during the Greenspan mandate but it was never explicitly assumed. In no statement was such a figure ever reported while Greenspan was chairman of the Fed, as he was concerned with the consequences of setting a specific number and showing it to the public. At the same time, while the committee agreed that they shouldn’t tighten monetary policy if inflation was below 2%, they also agreed that they shouldn’t accommodate the policy if the number was lying between 0% and 2%. Instead of being a target, the 2% was seen as a margin on a target of 0%, with this latter figure being the main goal of price stability.

But then in 2012, in the aftermath of the financial crisis, and given the difficulties central banks were facing in making the transmission of lower interest rates to the overall economy work effectively, they decided to strengthen the communications channels with the public. As part of the new policy channel, the Fed explicitly adopted a 2% target for monetary policy, assuming that price stability means pursuing an inflation rate of exactly 2%, and acting whenever the rate is above or below that level. However there is nothing in the Federal Reserve Act guiding in that direction. At that time the Fed also assumed a central tendency for the unemployment rate to lie between 5.2% and 6%, even though allowing this value to change over time (in contrast to what is allowed to happen to the inflation target).

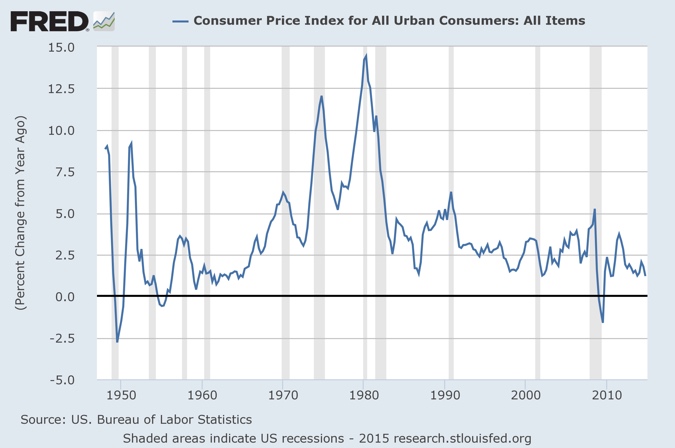

Now let’s look at what is happening in the US economy and put everything together. The unemployment rate lies at 5.5% and is expected to decrease to 5% by the year end, while the inflation rate currently sits at 1.4%, as measured by the PCE core index (the FED’s preferred inflation gauge). Alternatively, we can look at the CPI to measure price change but the number is not much different, currently lying near 1.6%. If measuring inflation with headline figures (without excluding energy and food prices) the numbers are much lower and near 0% for both the PCE deflator and the CPI indexes, but these numbers are heavily skewed by the downtrend in energy prices of late. As these events are seen as temporary, the central bank always bases its policy on the core measures. The rationale behind it is straightforward. Let’s suppose oil prices decline 50% from a price of $100 to $50. The headline inflation figure will suffer a negative impact (decreases) with the oil slump, but that happens within the period in which the price change occurs. If oil prices stay at the $50 level over the next measurement periods, while the price of oil is still 50% below what it was, the inflation rate will no longer be affected by it. Thus, the effect is temporary and should be discarded by using core inflation measures.

With the unemployment rate at very low levels and the inflation rate inside the 0%-2% bracket, and in accordance with the Federal Reserve Act, we can safely say that the Fed has already succeeded in achieving its main objectives. So, congratulations to the Fed. Case closed.

But Janet Yellen is reluctant to stabilise monetary policy towards an interest rate that is compatible with this long-term equilibrium, as she is worried about its effects on the equity market (through decreased valuations) and on corporate profits (through a strong dollar).

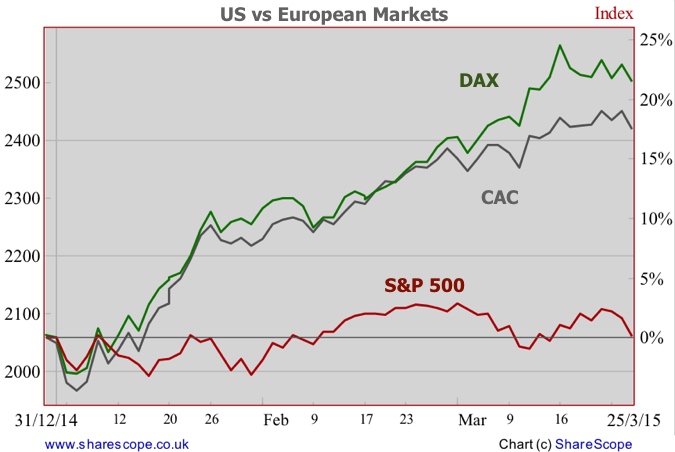

At a time when it is the turn of the ECB to play its QE card, European equities are booming while their US counterparts are stalling. With roughly a quarter of the year already gone, the Dax, the CAC, and the Euronext indexes are already showing a stunning YTD performance of around +20%. The Nasdaq, the S&P 500 and the Dow are near break-even levels. But we shouldn’t forget there was a time in which the opposite happened. US markets have tripled in value, helped by three large-scale asset purchase programmes and now it is the time for catching up with the fundamentals. Besides, there’s nothing in the Federal Reserve Act stating that the Fed should be worried about equity prices.

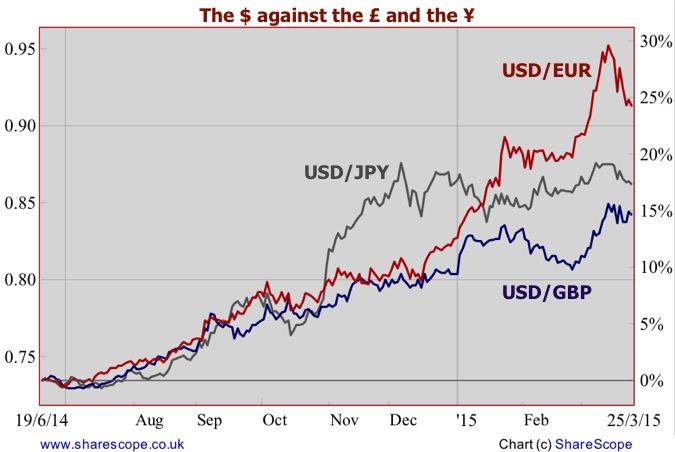

With regard to the strong dollar and its effect on corporate profits, there’s not much Janet Yellen can do about it. Since mid-2014 the market started anticipating an increase in interest rates in the US. With Europe now fully engaged in quantitative easing and the BoJ keeping its near-zero rates for the foreseeable future, the expectation of a rate hike in the US, increases the interest rate differential in favour of the dollar. The appreciation of the dollar was a natural consequence of this speculation. From a rate near 1.40 one year ago, the euro quickly declined to a rate as low as 1.05 on the dollar a few days ago (even though now trading near 1.10).

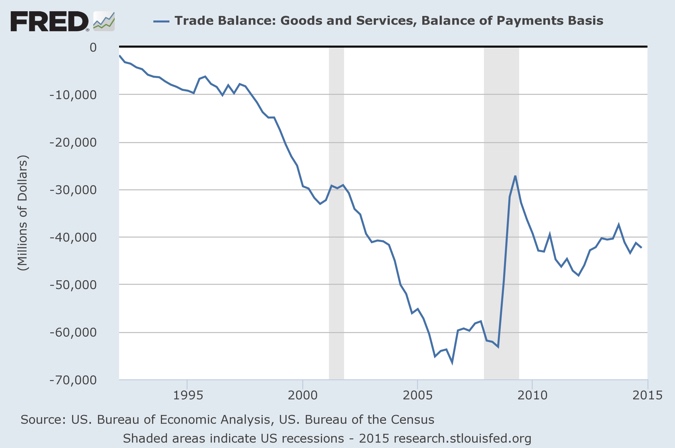

But we shouldn’t forget that the US has a very large trade imbalance, while the Eurozone has a large trade surplus. That means that if the current exchange rate prevails, the trade gap between the two countries will widen and thus wouldn’t be sustainable in the longer-term. This gap will end, pressuring the dollar towards devaluation against the euro. By focusing on short-term speculation, the Fed is ignoring the real fundamentals that should drive policy.

It is time for the Fed to wake up and follow its mandate, in line with what was stipulated by Congress, instead of trying to tweak it towards objectives that were never on the table and that are just generating global distortions. The same reasoning applies to the ECB, which seems to insist in distorting its initial aims.

Inflation is at low levels in the developed world largely because low interest rates don’t lead to a substantial increase in spending anymore but rather to an outflow of hot money in the direction of emerging markets, where it will stay until rates are attractive again in the developed world. The longer the cycle takes, the worse the emerging markets crisis will be. We already have signs across Asia and South America of many countries experiencing inflation and insurmountable increases in debt, as a consequence of too much easing conducted by developed countries. The latest addition to the group seems to be Africa, as Cote d’Ivoire, Nigeria, and Kenya have been seduced by the ECB’s artificially-induced negative yields and are issuing Eurobonds at record high demand. When the likes of the euro and the dollar start rising fast, I wonder how they plan to repay the debt.

The more I dig into the matter, the more I’m convinced that central banks are not part of the solution but rather part of the problem…

Comments (0)